Air China Limited – Annual report – 31 December 2022

Industry: airline

4. SIGNIFICANT ACCOUNTING POLICIES (extract)

Financial instruments (extract)

(ii) Debt instruments classified as at FVTOCI

Subsequent changes in the carrying amounts for debt instruments classified as at FVTOCI as a result of interest income calculated using the effective interest method are recognised in profit or loss. All other changes in the carrying amount of these debt instruments are recognised in other comprehensive income and accumulated under the heading of capital reserve. Impairment allowances are recognised in profit or loss with corresponding adjustment to other comprehensive income without reducing the carrying amount of these debt instruments. When these debt instruments are derecognised, the cumulative gains or losses previously recognised in other comprehensive income are reclassified to profit or loss.

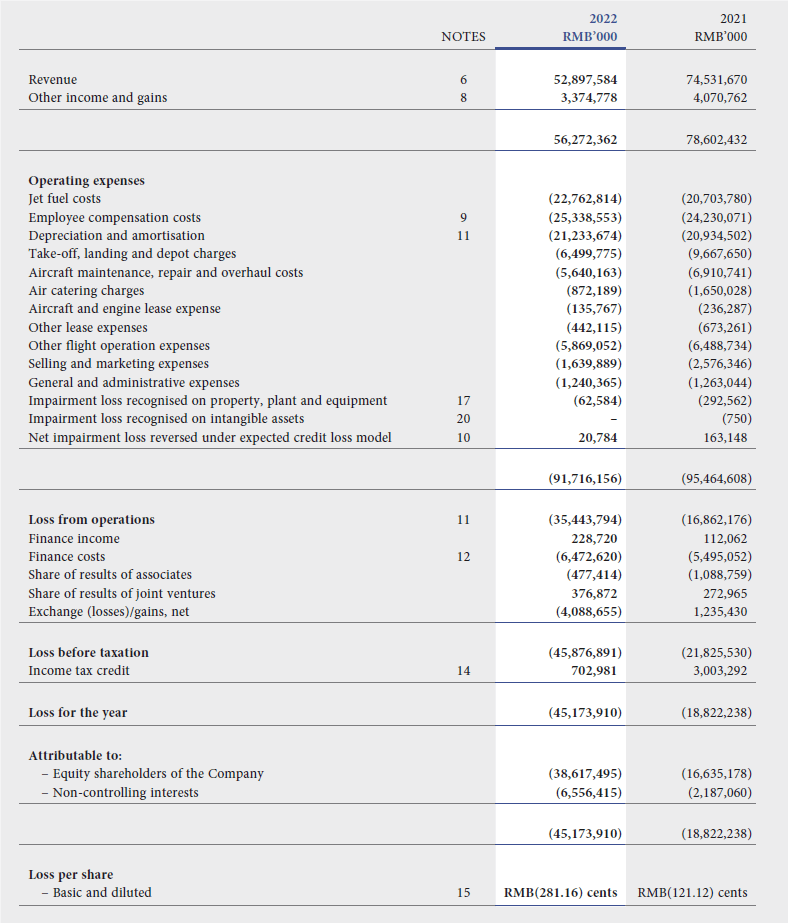

CONSOLIDATED STATEMENT OF PROFIT OR LOSS

For the Year Ended 31 December 2022

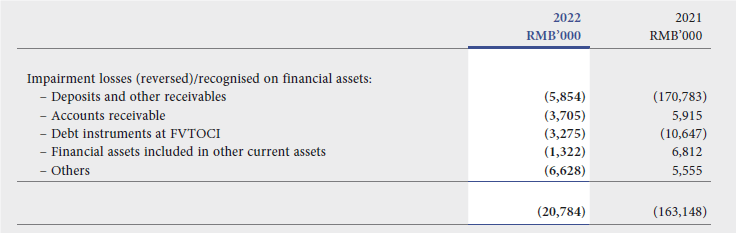

10. NET IMPAIRMENT LOSS REVERSED UNDER EXPECTED CREDIT LOSS MODEL

Details of impairment assessment are set out in Note 44.

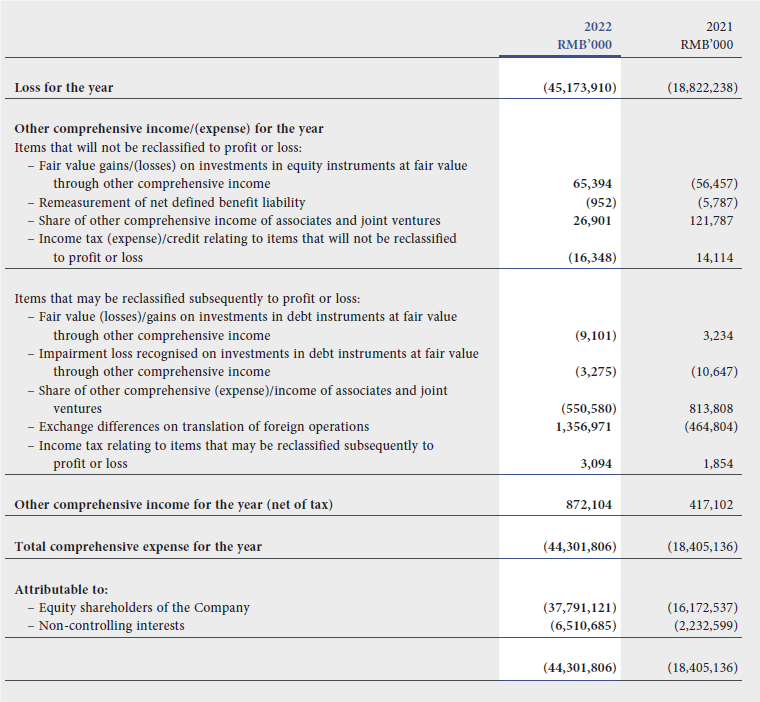

CONSOLIDATED STATEMENT OF PROFIT OR LOSS AND OTHER COMPREHENSIVE INCOME

For the Year Ended 31 December 2022