EVN AG – Annual report – 30 September 2024

Industry: utilities

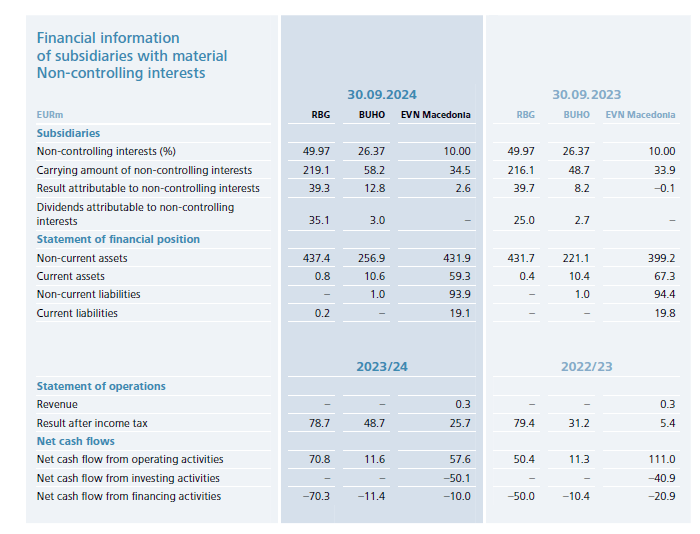

49. Non-controlling interests

The item non-controlling interests comprises the non-controlling interests in the equity of fully consolidated subsidiaries.

The following table provides information on each fully consolidated subsidiary of EVN with material non-controlling interests before intragroup eliminations:

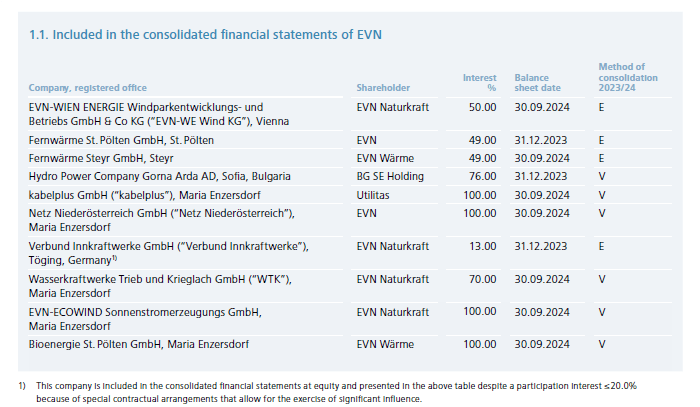

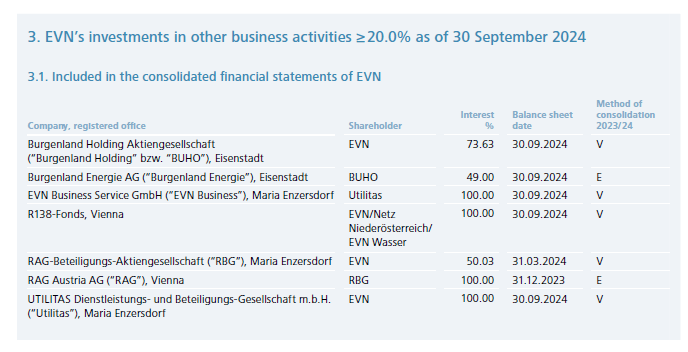

EVN’s investments according to § 245a (1) in connection with § 265 (2) UGB (extracts)