Hunting PLC – Annual report – 31 December 2021

Industry: oil and gas

41. Principal Accounting Policies (extract)

(b) Revenue

(i) Revenue from Contracts with Customers

- Revenue from contracts with customers is measured as the fair value of the consideration received or receivable for the provision of goods and services in the ordinary course of business, net of trade discounts, volume rebates, and sales taxes.

- Revenue is recognised when control of the promised goods or services is transferred to the customer. Consequently revenue for the sale of a product is recognised either: 1.Wholly at a single point in time when the entity has completed its performance obligation, which is most commonly indicated by shipment of the products or the products are made available to the customer for collection; or 2. Piecemeal over time during the period that control incrementally transfers to the customer while the good is being manufactured or the service is being performed.

- Hunting’s activities that require revenue recognition over time comprise: 1. Work undertaken to enhance customer-owned products – most commonly the lathing of a thread onto the ends of customer-owned plain-end pipe; 2.The manufacture of goods that are specifically designed for and restricted to the use of a particular customer, such as the manufacture of bespoke specialised circuitry and housing, and for which Hunting is entitled to a measure of recompense that reflects the fair value of the stage of production prior to their completion; and 3. The provision of services in which the customer obtains the benefit while the service is being performed – most commonly the storage and management services of customer-owned pipe.

- Hunting’s activities that require revenue recognition at a point in time comprise: 1. The sale of goods that are not specifically designed for use by one particular customer. These products include tubulars acquired by Hunting as plain-end pipe on which lathing work has been applied and which are resold as threaded pipe; and 2. The manufacture of goods that are specifically designed for one particular customer but for which Hunting is not entitled to a measure of recompense that reflects the fair value of the stage of production prior to completion.

(ii) Rental Revenue

- Rental revenue is measured as the fair value of the consideration received or receivable for the provision of rental equipment in the ordinary course of business, net of trade discounts and sales taxes.

- Revenue from the rental of plant and equipment is recognised as the income is earned.

(c) Other Income: Government Financial Assistance

- Cash received in respect of the COVID-19 pandemic is recognised in the consolidated income statement when the funded costs are incurred and are included in other operating income.

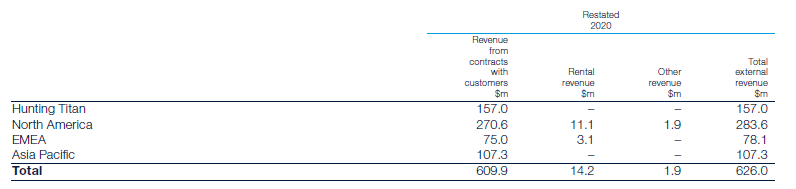

3. Revenue

In the following tables, a breakdown of the Group’s different revenue streams by segment has been given, including the disaggregation of revenue from contracts with customers.

There is no material difference in the timing of revenue recognition between contracts with customers at a point in time and contracts with customers over time, as the majority of Hunting’s performance obligations are relatively short. Revenue is typically recognised for products when the product is shipped or made available to customers for collection and for services either on completion of the service or, at a minimum, monthly for services covering more than one month. The amount of consideration is not adjusted for the effects of a significant financing component as, at contract inception, the period between when the entity transfers a promised good or service to a customer and when the customer pays for that good or service will be one year or less.

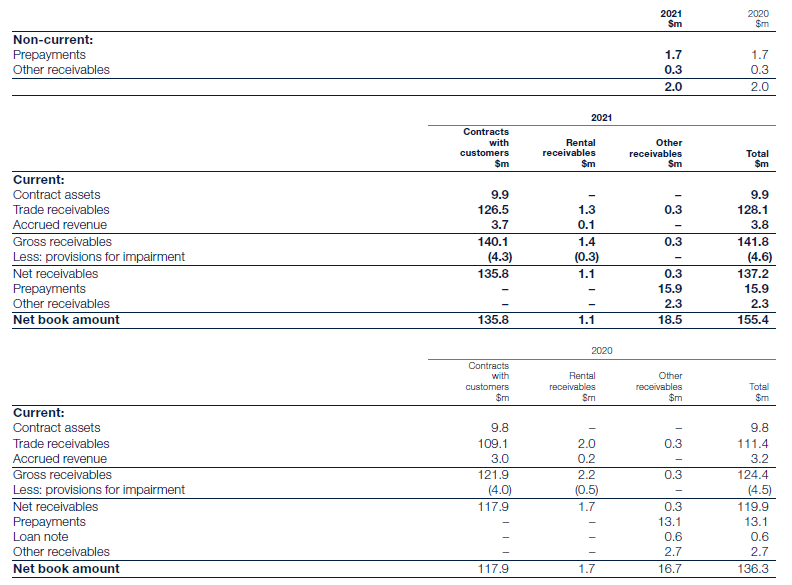

19. Trade and Other Receivables

Current and non-current other receivables generally arise from transactions outside the usual operating activities of the Group and comprise receivables from tax (VAT, GST, franchise taxes, and sales and use taxes) of $1.1m (2020 – $1.6m), derivative financial assets of $0.1m (2020 – $0.1m) and other receivables of $1.4m (2020 – $1.3m), which are financial assets measured at amortised cost.

The Group does not hold any other collateral as security and no assets have been acquired through the exercise of any collateral previously held.

In accordance with the requirements of the Group’s $160m committed Revolving Credit Facility, security has been granted over certain trade receivables and other receivables in the UK, US and Canada, which have a gross value of $102.4m (2020 – $84.3m). For the receivables pledged as security, their carrying value approximates their fair value.

Impairment of Trade and Other Receivables

The Group has chosen to apply lifetime expected credit losses (“ECLs”) to trade receivables, accrued revenue and contract assets upon their initial recognition. Each entity within the Group uses provision matrices for recognising ECLs on its receivables, which are based on actual credit loss experience over the past two years, at a minimum. Receivables are appropriately grouped by geographical region, product type or type of customer, and separate calculations produced, if historical or forecast credit loss experience shows significantly different loss patterns for different customer segments. Actual credit loss experience is then adjusted to reflect differences in economic conditions over the period the historical data was collected, current economic conditions, forward-looking information based on macroeconomic information and the Group’s view of economic conditions over the expected lives of the receivables. The contract assets relate to unbilled work in progress and have substantially the same risk characteristics as the trade receivables for the same types of contracts. It has, therefore, been concluded that the expected loss rates for trade receivables are a reasonable approximation of the loss rates for the contract assets.

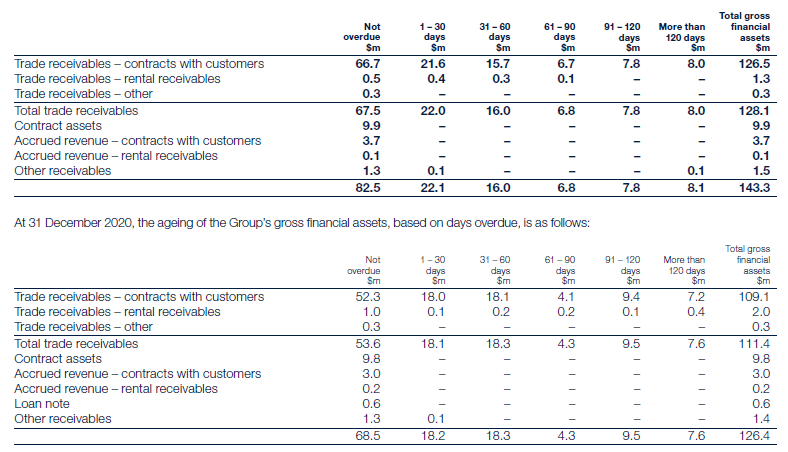

At 31 December 2021, the ageing of the Group’s gross financial assets, based on days overdue, is as follows:

Concentrations of credit risk with respect to trade receivables are limited due to the Group’s wide and unrelated customer base. The maximum exposure to credit risk is the carrying amount of each class of financial assets mentioned above. The carrying value of each class of receivables approximates their fair value as described in note 30.

Since the year-end 31 December 2020, there has been a modest decrease in the ageing of receivables despite the increase in trade receivables from $111.4m to $128.1m at 31 December 2021, with trade receivables not overdue at the year-end comprising 53% of gross trade receivables compared to 48% at 31 December 2020. Overdue debts arise due to a number of different factors, including the time taken in resolving any disputes, a culture of slow/late payment in some jurisdictions, and some debtors experiencing cash flow difficulties.

Default on a financial asset is usually considered to have occurred when any contractual payments under the terms of the debt are more than 90 days overdue. Usually, no further deliveries are made or services provided to customers that are more than 90 days overdue unless there is a valid reason to do so, such as billing issues have prevented the customer from settling the invoice. Permission from the local financial controller can be obtained to continue trading with customers with debts that are more than 90 days overdue, and the outstanding debts may also be rescheduled with the permission of the financial controller.

Whilst a proportion, 12% (2020 – 15%), of the Group’s trade receivables are more than 90 days overdue, the majority of these have not been impaired. Some of these debts have become overdue due to billing issues and others because the customer has just been slow to pay. Where there is no history of bad debts and there are no indicators that the debts will not be settled, these have not been impaired. These customers are monitored very closely for any indicators of impairment.

Receivables are written off when there is no reasonable expectation of recovery. Indicators that receivables are generally not recoverable include the failure of the debtor to engage in a repayment plan, failure to make contractual payments for a period greater than 180 days past due and the debtor being placed in administration. Where receivables have been written off, the entity will continue to try and recover the outstanding receivable. Impairment losses on receivables are presented net of unused provisions released to the consolidated income statement within operating expenses. Subsequent recoveries of amounts previously written off are credited against the same line item.

Credit risk arises on accrued revenue where goods or services have been provided to a customer but the amount is yet to be invoiced. The accrued revenue balance is short-term and relates to customers with a strong credit history. Therefore, the expected credit losses on this balance are immaterial and no provision for impairment has been recognised.

During the year, the movements on the provisions for impairment were as follows:

The provision for the impairment of trade and other receivables has increased modestly by $0.1m to $4.6m at the year-end, as some debtors face cash flow difficulties due to the global economic downturn and the risk of bad debts for the Group in the coming months increases. Financial assets that were written off during the year are no longer subject to enforcement activity.

For 2020, $1.2m of the $1.8m net impairment losses charged to the consolidated income statement was presented as an exceptional item (see note 6).

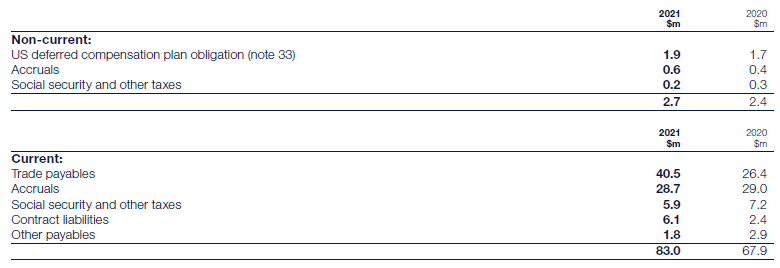

23. Trade and Other Payables

Other payables include derivative financial liabilities of $0.2m (2020 – $0.6m).

24. Contract Assets and Liabilities

The following table provides information about receivables, contract assets and contract liabilities from contracts with customers.

(a) Significant Changes in Contract Assets and Contract Liabilities

Contract assets increased from $9.8m at 31 December 2020 to $9.9m at 31 December 2021 due to increased levels of bespoke customer work-in-progress in the Subsea Spring business, which were offset by a reduction in bespoke customer work-in-progress in Dearborn.

Contract liabilities represent deposits received on contracts relating to the purchase of pipe in the Asia Pacific businesses, prior to Hunting placing an order with the steel mills, and increased from $2.4m at 31 December 2020 to $6.1m at 31 December 2021, reflecting a recent improvement in orders for the region.

(b) Revenue Recognised in Relation to Contract Liabilities

The following table shows how much of the revenue recognised in the current reporting period relates to carried-forward contract liabilities and how much relates to performance obligations that were satisfied in a prior year.

(c) Unsatisfied Performance Obligations

The aggregate amount of the transaction price allocated to partially or fully unsatisfied performance obligations as at the year-end on confirmed purchase orders received prior to the year-end is $211.5m (2020 – $144.4m). It is expected that 85% or $180.6m (2020 – 81% or $117.0m) will be recognised as revenue in the 2022 financial year and the remaining 15% or $30.9m (2020 – 19% or $27.4m) in future years.