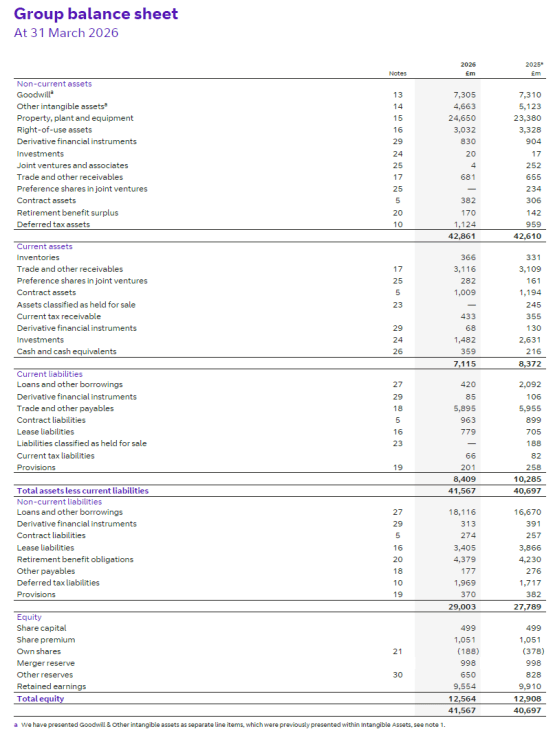

BT Group plc – Annual report – 31 March 2026

Industry: telecoms

5. Revenue

Material accounting policies that apply to revenue

Revenue from contracts with customers in scope of IFRS 15

Most revenue (excluding Openreach revenue) is recognised under IFRS 15 Revenue from Contracts with Customers. At contract inception we identify each distinct performance obligation within the contract. The transaction price is allocated to these performance obligations based on their relative standalone selling prices and revenue is recognised as each performance obligation is satisfied, either over time or at a point in time depending on the nature of the underlying goods or services.

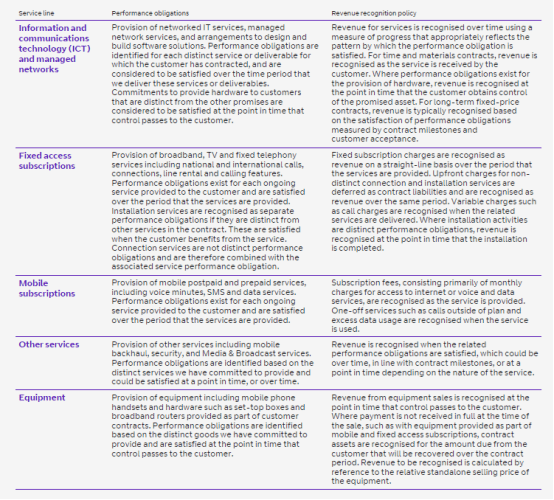

The table below summarises the key performance obligations across our major service lines, including the timing of when they are satisfied and the associated revenue‑recognition policy. This note also provides information on revenue expected to be recognised in future periods in relation to unsatisfied performance obligations for contracts in place at 31 March 2026.

Openreach revenue

Revenue within Openreach is primarily within the scope of IFRS 16 and is recognised over the period of the lease in accordance with the underlying contractual terms.

Application of revenue accounting policies

Below, we include a description of principal activities from which the Group generates its revenue and the recognition policy applied to each.

We recognise revenue based on the relative standalone selling price of each performance obligation. Determining the standalone selling price often requires judgement and may be derived from regulated prices, list prices, a cost-plus derived price or the price of similar products when sold on a standalone basis by BT or a competitor. In some cases it may be appropriate to use the contract price when this represents a bespoke price that would be the same for a similar customer in a similar circumstance.

The fixed access and mobile subscription arrangements sold by our Consumer business are typically payable in advance, with any variable or one-off charges billed in arrears. Contracts are largely inflation-linked with price increases recognised when effective. Payment is received immediately for direct sales of equipment to customers. Where equipment is provided to customers under mobile and fixed access subscription arrangements, payment for the equipment is received over the course of the contract term. Payments received in advance are recognised as contract liabilities; amounts billed in arrears are recognised as contract assets.

We adopt variable consideration to allocate the transaction price to take account of the likelihood of the customer upgrading to a new handset during the contract term. Consideration is constrained to a period shorter than the contract term and is allocated to the handset and airtime based on relative standalone selling price. Certain Business and International long-term contracts offer rebates to our customers. Where this is the case we make an estimate of variable consideration at the outset of the contract based on assumed volumes. These rebates are normally settled monthly against service revenues.

We apply the practical expedient in IFRS 15 that permits revenue to be recognised on an “as‑invoiced” basis where the amount we invoice corresponds directly with the value delivered to the customer for fixed access and mobile subscription services. We also apply the practical expedient not to disclose the transaction price allocated to remaining performance obligations for these contracts. The use of these expedients is consistent with prior periods.

We do not have any material obligations in respect of returns, refunds or warranties.

Where we act as an agent in a transaction, such as certain insurance services offered, we recognise commission net of directly attributable costs.

We exercise judgement in assessing whether the initial set-up, transition and transformation phases of long-term contracts are distinct from the other services to be delivered under the contract and therefore represent separate performance obligations. This determines whether revenue is recognised in the early stages of the contract, or deferred until delivery of the other services promised in the contract begins.

We recognise immediately the entire estimated loss for a contract when we have evidence that the contract is unprofitable. If these estimates indicate that a contract will be less profitable than previously forecast, contract assets may have to be written down to the extent they are no longer considered to be fully recoverable. We perform ongoing profitability reviews of our contracts in order to determine whether the latest estimates are appropriate. Key factors reviewed include:

- Transaction volumes or other inputs affecting future revenues which can vary depending on customer requirements, plans, market conditions and other factors such as general economic conditions.

- Our ability to achieve key contract milestones connected with the transition, development, transformation and deployment phases for customer contracts.

- The status of commercial relations with customers and the implications for future revenue and cost projections.

- Our estimates of future staff and third party costs and the degree to which cost savings and efficiencies are deliverable.

Revenue from lease arrangements in scope of IFRS 16

Presented within revenue is income from arrangements classified as operating leases under IFRS 16 and which represent core business activities for the group. Income predominantly relates to Openreach’s leases of fixed-line telecommunications infrastructure to communication providers, and leases of devices to Consumer customers as part of fixed access subscription offerings.

At inception of a contract, we determine whether the contract is, or contains, a lease following the accounting policy set out in note 16. Arrangements meeting the definition of a lease in which we act as lessor are classified as operating or finance leases at lease inception based on an overall assessment of whether the lease transfers substantially all the risks and rewards incidental to ownership of the underlying asset. If this is the case then the lease is a finance lease; if not, it is an operating lease. For sub-leases, we make this assessment by reference to the characteristics of the right-of-use asset associated with the head lease rather than the underlying leased asset.

Income from arrangements classified as operating leases is presented as revenue where it relates to our core operating activities. Operating lease income from other arrangements is presented within other operating income (note 6).

We recognise operating lease payments as income on a straight-line basis over the lease term. Any upfront payments received, such as connection fees, are deferred over the lease term. Determining the lease term is subject to the significant judgements set out in note 16.

Where the contract contains both lease and non-lease components, the transaction price is allocated between the components on the basis of relative standalone selling price.

Where an arrangement is assessed as a finance lease we derecognise the underlying asset and recognise a receivable equivalent to the net investment in the lease. Finance lease receivables are presented in note 16. The receivable is measured based on future payments to be received discounted using the interest rate implicit in the lease, adjusted for any direct costs. Any difference between the derecognised asset and the finance lease receivable is recognised in the income statement. Where the nature of services delivered relates to our core operating activities it is presented as revenue. Where it relates to non-core activities it is presented within other operating income (note 6).

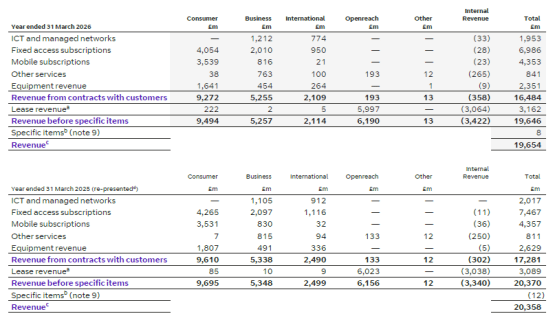

Disaggregation of revenue

The following table disaggregates revenue by our major service lines and by reportable segment.

a Lease revenue includes income from Openreach’s fixed access subscription services.

b Relates to regulatory matters classified as specific. See note 9.

c We have further disaggregated the revenue presented here to derive the UK adjusted service revenue of £15,445m (FY25: £15,568m). Please refer to our adjusted UK service revenue reconciliation in the Additional Information section of this report for details. Adjusted UK service revenue includes some portion of equipment revenue where that equipment is sold as part of a managed services contract, or where that equipment cannot be practicably separated from the underlying service.

d FY25 comparative information re‑presented. Further information on the nature of these re‑presentations is set out below. Note 34 presents a bridge between financial information for the year to 31 March 2025 as published on 22 May 2025 and the comparatives presented above.

Re-presentation of revenue

FY25 comparative revenue information has been re‑presented to reflect a number of changes to the Group’s external reporting. These include (i) the creation of the new International CFU following its separation from the Business CFU, (ii) changes in the Group’s internal management reporting reviewed by the Chief Operating Decision Maker (CODM), and (iii) updates to segmental revenue to better reflect the nature of services provided and the underlying trading relationships between units.

As a result of these changes, disaggregated revenue has been re‑presented to reflect updates to the CODM reporting structure, with ‘Equipment’ and ‘Other Services’ now shown separately and lease revenue disclosed distinctly. Internal CFU revenue is now included, and enhanced system data has enabled more granular categorisation being used to align service line reporting with the Group’s accounting policies. Comparatives have been re‑presented accordingly. Note 34 presents a bridge between financial information for the year to 31 March 2025 as published on 22 May 2025 and the comparatives presented above.

Remaining performance obligations

Revenue expected to be recognised in future periods for performance obligations that are not complete (or are partially complete) as at 31 March 2026 is £11,834m (FY25: £13,249m). Of this, £4,736m (FY25e: £5,260m) relates to ICT and managed services contracts and equipment and other services which will substantially be recognised as revenue within three years. Fixed access and mobile subscription services typically have shorter contract periods and so £7,098m (FY25e: £7,989m) will substantially be recognised as revenue within two years.

Lease income

Presented within revenue is £3,162m (FY25: £3,089m) income from arrangements classified as operating leases under IFRS 16 and which represent core business activities for the group. Income relates predominantly to Openreach’s leases of fixed-line telecommunications infrastructure to external communications providers, classified as fixed access subscription revenue in the table above, and leases of devices to Consumer customers as part of fixed access subscription offerings, classified as equipment and other services.

e FY25 comparative information has been re-presented to better align revenue categories, reflecting the wider revenue re-presentation of revenue referenced above.

During the year we also recognised:

- £19m (FY25: £19m) operating lease income from non-core business activities which is presented in other operating income (note 6). Note 15 presents an analysis of payments to be received across the remaining term of operating lease arrangements.

- £19m (FY25: £12m) revenue in relation to upfront gains from arrangements meeting the definition of a finance lease. These arrangements meet the criteria for revenue recognition as they concern leases and sub-leases of telecommunications infrastructure that represent core business activities of the group.

£24m (FY25: £33m) of our lease income relates to the sub-leasing of right-of-use assets. These are primarily operating sub-leases of unutilised properties, and finance sub-leases of telecommunications infrastructure.

Key accounting estimates made in accounting for revenue

Estimate of customer refunds

There remains an accounting estimate in place to reflect a risk of billing inaccuracy where there is the presence of bespoke pricing. We have recognised a liability of £47m (FY25: £51m) in relation to this billing inaccuracy. This is presented within note 18 and represents our best estimate required to cover ongoing billing adjustments to products relating to both current and prior periods.

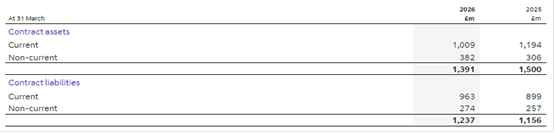

Contract assets and liabilities

Material accounting policies that apply to contract assets and liabilities

We recognise contract assets for goods and services for which control has transferred to the customer before we have the right to bill. These assets mainly relate to mobile handsets provided upfront but paid for over the course of a contract. Contract assets are reclassified as receivables when the right to payment becomes unconditional and we have billed the customer.

Contract liabilities are recognised when we have received advance payment for goods and services that we have not transferred to the customer. These primarily relate to fees received for connection and installation services that are not distinct performance obligations.

Where the initial set-up, transition or transformation phase of a long-term contract is considered to be a distinct performance obligation we recognise a contract asset for any work performed but not billed. Conversely a contract liability is recognised where these activities are not distinct performance obligations and we receive upfront consideration. In this case eligible costs associated with delivering these services are capitalised as fulfilment costs, see note 17.

We provide for expected lifetime losses on contract assets following the policy set out in note 17.

Contract assets and liabilities are as follows:

£764m (FY25: £704m) of the contract liability at 31 March 2026 was recognised as revenue during the year. Impairment losses of £19m (FY25: £47m) were recognised on contract assets during the year.

The expected credit loss provisions recognised against contract assets vary across the group due to the nature of our customers; the expected loss rate at 31 March 2026 was 2% (FY25: 3%).

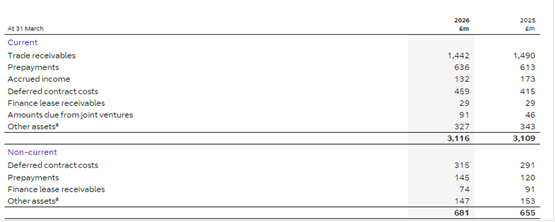

17. Trade and other receivables

Material accounting policies that apply to trade and other receivables

Trade receivables are recognised where the right to receive payment from customers is conditional only on the passage of time. We initially recognise trade and other receivables at fair value, which is usually the original invoiced amount. They are subsequently carried at amortised cost using the effective interest method. The carrying amount of these balances approximates to fair value due to the short maturity of amounts receivable.

We provide services to consumer and business customers, mainly on credit terms. We know that certain debts due to us will not be paid through the default of a small number of our customers. Because of this, we recognise an allowance for doubtful debts on initial recognition of receivables, which is deducted from the gross carrying amount of the receivable. The allowance is calculated by reference to credit losses expected to be incurred over the lifetime of the receivable. In estimating a loss allowance we consider historical experience and informed credit assessment alongside other factors such as the current state of the economy and particular industry issues. We consider reasonable and supportable information that is relevant and available without undue cost or effort.

Once recognised, trade receivables are continuously monitored and updated. Allowances are based on our historical loss experiences for the relevant aged category as well as forward-looking information and general economic conditions. Allowances are calculated by individual CFUs in order to reflect the specific nature of the customers relevant to that CFU.

The group utilises factoring arrangements for selected trade receivables. Trade receivables that are subject to debt factoring arrangements are derecognised if they meet the conditions for derecognition detailed in IFRS 9 ‘Financial instruments’ and the related cash flows received are presented as cash flows from operating activities. Where a portfolio of trade receivables are either sold or held to collect the contractual cash flows, they are recorded at fair value through other comprehensive income.

Contingent assets such as any insurance recoveries are recognised within trade and other receivables only when their receipt is virtually certain.

a Other assets include £275m (FY25: £262m) of Flex Pay receivables and £6m (FY25: £35m) of deferred cash consideration mainly relating to the FY23 disposal of BT Sport.

Amounts due from joint ventures relates to a sterling Revolving Credit Facility (RCF) provided to the Sports JV, see note 31. The expected loss provision is immaterial.

The company has a facility with a third party for the sale of mobile handset receivables. Under this facility, the Group transfers substantially all of the risks and rewards to the third party, and therefore has derecognised the transferred receivables. During FY26, we received net cash flows of £159m (FY25: £420m) through this facility. The cashflows are included within the ‘(Increase) decrease in trade and other receivables’ line in the ‘Statement of Cash Flows’. The net impact of working capital programmes on normalised free cash flow is set out in the Group’s Alternative Performance Measures. We use handset‑related programmes to manage the cash flow impact of extending handset contract lives from 24‑month to 36‑month customer contracts, better aligning cash receipts with the timing of revenue recognition.

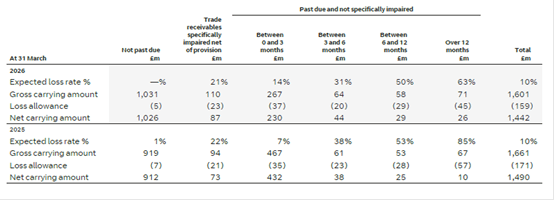

Trade receivables are stated after deducting allowances for doubtful debts, as follows:

The expected credit loss allowance for trade receivables was determined as follows:

Trade receivables not past due and accrued income are analysed below by CFU.

a Comparative information for the year to 31 March 2025 has been re-presented to reflect the formation of the new International CFU. For more information see note 1.

Given the broad and varied nature of our customer base, the analysis of trade receivables not past due and accrued income by CFU is considered the most appropriate disclosure of credit concentrations.

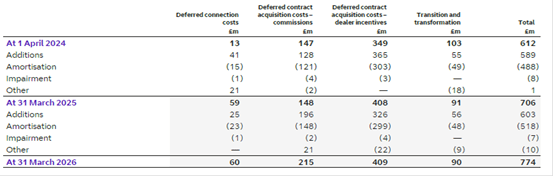

Deferred contract costs

Material accounting policies that apply to deferred contract costs

We capitalise certain costs associated with the acquisition and fulfilment of contracts with customers and amortise them over the period that we transfer the associated services.

Connection costs are deferred as contract fulfilment costs because they allow satisfaction of the associated connection performance obligation and are considered recoverable. Sales commissions and other third party contract acquisition costs are capitalised as costs to acquire a contract unless the associated contract term is less than 12 months, in which case they are expensed as incurred. Capitalised costs are amortised over the minimum contract term. A portfolio approach is used to determine contract term.

Where the initial set-up, transition and transformation phases of long-term contractual arrangements represent distinct performance obligations, costs in delivering these services are expensed as incurred. Where these services are not distinct performance obligations, we capitalise eligible costs as a cost of fulfilling the related service. Capitalised costs are amortised on a straight-line basis over the remaining contract term, unless the pattern of service delivery indicates a more appropriate profile. To be eligible for capitalisation, costs must be directly attributable to specific contracts, relate to future activity, and generate future economic benefits. Capitalised costs are regularly assessed for recoverability.

The following table shows the movement on deferred costs: