Genus plc – Annual report – 30 June 2025

Industry: agriculture

29. RETIREMENT BENEFIT OBLIGATIONS

The Group operates a number of defined contribution and defined benefit pension schemes, covering many of its employees. The principal funds are the Milk Pension Fund (‘MPF’) and the Dalgety Pension Fund (‘DPF’) in the UK, which are defined benefit schemes. The assets of these funds are held separately from the Group’s assets, and are administered by trustees and managed professionally.

Accounting policies

Defined contribution pension schemes

A number of our employees are members of defined contribution pension schemes. We charge contributions to the Income Statement as they become payable under the scheme rules. We show differences between the contributions payable and the amount we have paid as either accruals or prepayments in the Balance Sheet. The schemes’ assets are held separately from the Group’s assets.

Defined benefit pension schemes

The Group operates defined benefit pension schemes for some of its employees. These schemes are closed to new members and to further accrual. We calculate our net obligation separately for each scheme, by estimating the amount of future benefit that employees have earned, in return for their service to date. We discount that benefit to determine its present value and deduct the fair value of the plan’s assets (at bid price). The liability discount rate we use is the market yield at the balance sheet date on high-quality corporate bonds, with terms to maturity approximating our pension liabilities. Qualified actuaries perform the calculations, using the projected unit method.

We recognise actuarial gains and losses in equity in the period in which they occur, through the Group Statement of Comprehensive Income. Actuarial gains and losses include the difference between the expected and actual return on scheme assets and experience gains and losses on scheme liabilities.

Genus and the other participating employers are jointly and severally liable for the MPF’s obligations. We account for our section of the scheme and our share of any orphan assets and liabilities, and provide for any amounts we believe we will have to pay under our joint and several liability. The joint and several liability also means we have a contingent liability for the scheme’s obligations that we have not accounted for.

Under the joint and several liability, we initially recognise any changes in our share of orphan assets and liabilities in the Income Statement. After this initial recognition, any actuarial gains and losses on the orphan assets and liabilities are recognised directly in equity through the Group Statement of Changes in Equity, in the period in which they occur.

During the year, the National Pig Development Company Pension Fund (‘NPD’) purchased annuities in order to hedge longevity risk for pensioners within the scheme. As permitted by IAS 19, the Group has opted to recognise the difference between the fair value of the plan assets and the cost of the policy as an actuarial loss in Other Comprehensive Income.

We measure the fair value of our qualifying insurance policy assets to be the deemed present value of the related obligation.

Retirement benefit obligations

The financial positions of the defined benefit schemes, as recorded in accordance with IAS 19 and IFRIC 14, are aggregated for disclosure purposes. The liability/(asset) split by principal scheme is set out below.

The MPF and DPF pension schemes are in IAS 19 surplus positions but these surpluses are restricted to nil under IFRIC 14.

Overall, we expect to pay £0.4m (2024: £0.4m) in contributions to defined benefit plans in the 2026 financial year.

The defined benefit plans are administered by trustee boards that are legally separated from the Group. The trustee board of each pension fund consists of representatives who are employees, former employees or are independent from the Company. The boards of the pension funds are required by law to act in the best interest of the plan participants and are responsible for setting certain policies, such as investment and contribution policies, and for the governance of the fund.

The defined benefit pension schemes expose the Group to actuarial risks such as greater than expected longevity of members, lower than expected return on investments and higher than expected inflation, which may increase the plans’ liabilities or reduce the value of their assets.

UK pensions are regulated by The Pensions Regulator, a non-departmental public body established under the Pensions Act 2004 and sponsored by the Department for Work and Pensions, operating within a legal regulatory framework set by the UK Parliament. The Pensions Regulator has statutory objectives set out in legislation, which include promoting and improving understanding of the good administration of work-based pensions, protecting member benefits and regulating occupational defined benefit and contribution schemes. The Pensions Regulator’s statutory objectives and regulatory powers are described on its website.

All defined benefit schemes are registered as an occupational pension plan with HMRC and are subject to UK legislation and oversight from The Pensions Regulator. UK legislation requires that pension schemes are funded prudently and valued at least every three years. Separate valuations are required for each scheme. Within 15 months of each valuation date, the plan trustees and the Group must agree any contributions required to ensure that the plan is fully funded over time, on a suitably prudent measure.

Funding plans are individually agreed with the respective trustees for each of the Group’s defined benefit pension schemes, taking into account local regulatory requirements.

In June 2023 the High Court ruled, in the case of Virgin Media vs NTL Pension Trustees II Limited, that certain historical adjustments to defined benefit schemes may be invalid. In respect of this case, for the MPF, a detailed review has been performed and concluded that the risk of any additional liability is low; for the NPD, the scheme closed to future accrual in March 1997, and any changes after this would not materially impact member benefits; and for DPF, as the vast majority of the scheme has been bought out or is in the process of buy-out, there are not expected to be any additional liabilities resulting from the ruling. The risk of additional liabilities is further reduced by the recent announcement by the Department for Work and Pensions that the Government will introduce legislation to deal with issues arising from the Virgin Media judgement. On this basis no additional liabilities have been recorded in the financial statements.

The Milk Pension Fund (‘MPF’)

The MPF was previously operated by the Milk Marketing Board and was also open to staff working for Milk Marque Ltd (the principal employer, now known as Community Foods Group Limited), National Milk Records plc, First Milk Ltd, hauliers associated to First Milk Ltd, Dairy Farmers of Britain Ltd (which went into receivership in June 2009) and Milk Link Ltd. Genus Breeding Limited is currently the principal employer.

We have accounted for our section of the scheme and our share of any orphan assets and liabilities, which together represent approximately 86% of the MPF (2024: 86%). Although the MPF is managed on a sectionalised basis, it is a ‘last man standing’ scheme, which means that all participating employers are jointly and severally liable for all of the fund’s liabilities. With effect from 30 June 2013, Genus’s remaining active members ceased accruing benefits in the fund and became deferred pensioners.

The most recent actuarial triennial valuation of the MPF was at 31 March 2024 and was carried out by qualified actuaries. The valuation has been agreed by the trustees.

The principal actuarial assumptions adopted in the 2024 valuation were that:

- investment returns on existing assets would exceed fixed-interest gilt yields by 1.0% per annum until 31 March 2030, then by 0.5% per annum thereafter;

- Consumer Price Index (‘CPI’) price inflation is expected to be 0.7% per annum lower than Retail Price Index (‘RPI’) price inflation until 31 March 2030, then less 0.1% per annum thereafter; and

- pensions in payment and pensions in deferment would increase in future in line with CPI price inflation, subject to various minimum and maximum increases.

At 31 March 2024, the market value of the fund’s assets was £341m. This represented approximately 104% of the value of the uninsured liabilities, which were £329m at that date.

The surplus in the fund as a whole, by reference to the 31 March 2024 valuation, was £12m (of which Genus’s notional share was £10m). Reflecting the improvement in the funding position, no deficit repair contributions and no contributions in respect of the scheme’s operating expenses are payable until 30 June 2028.

The disclosures required under IAS 19 have been calculated by an independent actuary, based on accurate calculations carried out as at 31 March 2024 and updated to 30 June 2025.

At 30 June 2025, the MPF was in an overall net pension asset position of £16.2m (2024: £31.9m). However, the Company does not have the unilateral right to this surplus and therefore in line with IFRIC 14, the recognition of this asset is restricted.

Dalgety Pension Fund (‘DPF’)

The most recent actuarial valuation of the DPF was at 31 March 2021 and was carried out by qualified actuaries.

The principal actuarial assumptions adopted in the 2021 valuation were that:

- investment returns on existing assets are gilt yields less 0.35% per annum;

- CPI price inflation is expected to be 0.7% per annum lower than RPI price inflation until 2030, then utilising the RPI curve from 2030 onwards; and

- pensions in payment and pensions in deferment would increase in future in line with CPI price inflation, subject to various minimum and maximum increases.

The market value of the available assets at 31 March 2021 was £938m. The value of those assets represented approximately 100% of the value of the uninsured liabilities, which were £937m at 31 March 2021. Under the funding agreement, the Company will not have to make deficit repair contributions.

The disclosures required under IAS 19 have been calculated by an independent actuary, based on accurate calculations carried out as at 31 March 2021 and updated to 30 June 2025.

Formal notice to wind-up the DPF was given by the scheme’s sponsoring employers on 13 February 2025, as all member benefits have now been secured with insurance companies, following the completion of the GMP equalisation exercise. Wind-up is expected to complete in the first quarter of 2026. As a result a significant number of members have now received their individual pension policies resulting in a net settlement of asset and liabilities of £421m, as the trustees are no longer liable. The remaining individual pension policies are expected to be issued to members during the second half of 2025.

At 30 June 2025, the DPF, which includes a £5.5m separate reserve held against future unknown liabilities materialising, was in an overall net pension asset position of £3.8m (2024: £4.5m). However, in the judgement of the Company, there is no unconditional and unilateral right to this surplus. The trustees, in relation to any scheme surplus, still needs to complete certain statutory requirements with the pension regulator and scheme members as part of the wind-up process and therefore in line with IFRIC 14, the recognition of this asset is restricted.

National Pig Development Company Pension Fund (‘NPD’)

The Group operates a closed defined benefit scheme for a small number of former employees of the National Pig Development Company Limited. The total market value of scheme assets and liabilities at 30 June 2025, under the provisions of IAS 19, were £4.7m (2024: £5.4m) and £4.7m (2024: £4.8m), respectively.

The most recent actuarial triennial valuation of the NPD was at 30 June 2023 and was carried out by qualified actuaries. The valuation has been agreed by the trustees.

The principal actuarial assumptions adopted in the 2023 valuation were that:

- investment returns on existing assets are gilt yields less 0.35% per annum;

- CPI price inflation is expected to be 0.6% per annum lower than RPI price inflation; and

- pensions in payment and pensions in deferment would increase in future in line with CPI price inflation, subject to various minimum and maximum increases.

The market value of the available assets at 30 June 2023 was £5.0m. The value of those assets represented approximately 92% of the value of the uninsured liabilities, which were £5.4m at 30 June 2023. In May 2024, it was agreed under the trustee-prepared schedule of contributions that no deficit repair contributions will be payable from 1 June 2024.

On 2 August 2024, the Trustees purchased a bulk annuity (‘Buy-in Policy’) with Just Retirement Limited (‘Just’). In exchange for a combined premium of £5.5m, all future benefit obligations for both deferred and pensioner members of the Scheme were insured with Just from 2 August 2024.

The disclosures required under IAS 19 have been calculated by an independent actuary, based on accurate calculations carried out as at 30 June 2023 and updated to 30 June 2025.

Other unfunded schemes

When the Group acquired Sygen International plc in 2005, it also acquired unfunded defined benefit schemes and an unfunded retirement health benefit plan, which it now operates for the benefit of the previous Group’s senior employees and Executives.

Unfunded defined benefit schemes

The scheme liabilities for two unfunded defined benefit schemes amounted to £4.0m (2024: £4.6m), based on IAS 19’s methods and assumptions. This amount is included within pension liabilities in the Group Balance Sheet. It also includes several other unfunded defined benefits liabilities which amounted to £2.4m (2024: £2.1m). Interest on pension scheme liabilities amounted to £0.3m (2024: £0.3m). The disclosures required under IAS 19 have been calculated by an independent actuary, using the principal assumptions used to calculate the scheme liabilities for the defined benefit schemes.

Post-retirement healthcare

The scheme liabilities for the unfunded retirement health benefit plan amounted to £0.5m (2024: £0.5m), based on IAS 19’s methods and assumptions. This amount is included within retirement benefit obligations in the Group Balance Sheet. Interest on plan liabilities amounted to £nil (2024: £nil).

The principal assumptions used to calculate the plan liabilities were that the discount rate would be 5.50% (2024: 5.15%) and that the long-term rate of medical expense inflation would be 6.90% (2024: 6.90%).

Aggregated position of defined benefit schemes

Each of the defined benefit schemes manages risks through a variety of methods and strategies, including equity protection, to limit the downside risk of falls in equity markets, as well as inflation and interest rate hedging. By funding its defined benefits schemes, the Group is exposed to the risk that the cost of meeting its obligations is higher than anticipated. This could occur for several reasons, for example:

- Investment returns on the schemes’ assets may be lower than anticipated, especially if falls in asset values are not matched by similar falls in the value of the schemes’ liabilities.

- The level of price inflation may be higher than that assumed, resulting in higher payments from the schemes.

- Scheme members may live longer than assumed, for example due to advances in healthcare. Members may also exercise (or not exercise) options in a way that leads to increases in the schemes’ liabilities, for example through early retirement or commutation of pension for cash.

- Legislative changes could also lead to an increase in the schemes’ liabilities.

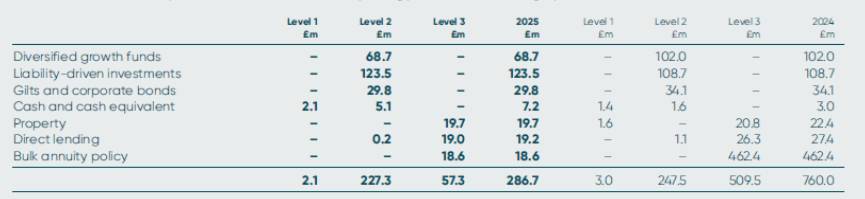

Aggregated position of defined benefit schemes

The fair value of the total plan assets at the end of the reporting period for each category is as follows:

Note:

Level 1: valued using unadjusted quoted prices in active markets for identical financial instruments.

Level 2: valued using techniques based on information that can be obtained from observable market data.

Level 3: valued using techniques incorporating information other than observable market data.

All of the above assets with the exception of cash and the annuity policy are held through pooled investment vehicles which are unquoted.

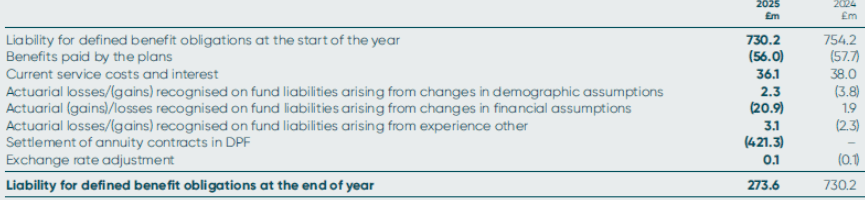

Movement in the liability for defined benefit obligations

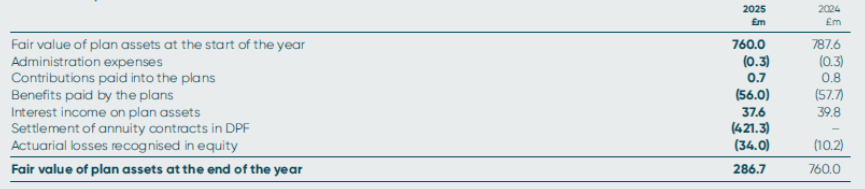

Movement in plan assets

Aggregated position of defined benefit schemes

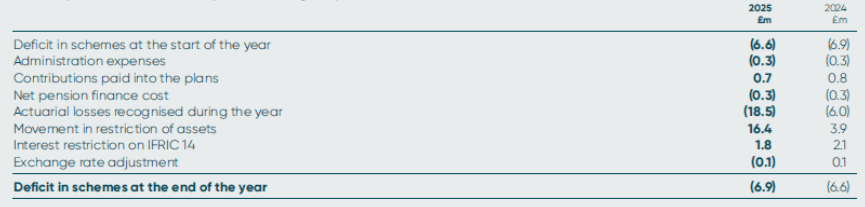

Summary of movements in Group deficit during the year

Amounts recognised in the Group Income Statement

The expense is recognised in the following line items in the Group Income Statement

Actuarial losses/(gains) recognised in the Group Statement of Comprehensive Income

Actuarial assumptions and sensitivity analysis

Principal actuarial assumptions (expressed as weighted averages) are:

The mortality assumptions used are consistent with those recommended by the schemes’ actuaries and reflect the latest available tables, adjusted for the experience of the scheme where appropriate. For 2025 and 2024, the mortality tables used are 100% of the S3PMA (males)/S3PFA_M (females) all lives tables, with birth year and CMI 2023 projections with parameters of Sk=7.0 and A=0.5% and weighting parameters of w2020=0%, w2021=0%, w2022=15% and w2023=15%, subject to a long-term rate of improvement of 1.50% per annum for males and females.

Aggregated position of defined benefit schemes

The following table shows the assumptions used for all schemes and illustrates the life expectancy of an average member retiring at age 65 at the balance sheet date and a member reaching age 65 in 20 years’ time.

Duration of benefit obligations

Sensitivity analysis

Measurement of the Group’s defined benefit obligation is sensitive to changes in certain key assumptions. The sensitivity analysis below shows how a reasonably possible increase or decrease in a particular assumption would, in isolation, result in an increase or decrease in the present value of the defined benefit obligation as at 30 June 2025.

The sensitivity analysis may not be representative of an actual change in the defined benefit obligation, as it is unlikely that changes in assumptions would occur in isolation from one another.

The sensitivities assume the funds’ assets remain unchanged. However, in practice changes in interest rates and inflation will also affect the value of the funds’ assets. The funds’ investment strategy is to hold matching assets with values that move in line with the liabilities of the fund, to protect against changes in interest rates and inflation.

This sensitivity analysis has been prepared using the same method adopted when adjusting results of the latest funding valuation to the balance sheet date. This is the same approach as adopted in previous periods.

The history of experience adjustment is as follows: