Bombardier Inc. – Annual report – 31 December 2025

Industry: contracting

NOTES TO THE CONSOLIDATED FINANCIAL STATEMENTS

For the fiscal years ended December 31, 2025 and 2024

(Tabular figures are in millions of U.S. dollars, unless otherwise indicated)

2. SUMMARY OF MATERIAL ACCOUNTING POLICIES (extract)

Revenue recognition

Manufacturing and Other – Revenues from the sale of new aircraft are considered a single performance obligation and are recognized at delivery, which is the point in time when the customer has obtained control of the aircraft and the Corporation has satisfied its performance obligation. All costs incurred or to be incurred in connection with the sale, including warranty costs and sales incentives, are charged to cost of sales or as a deduction from revenues at the time revenue is recognized.

For the bill-and-hold arrangements in respect of new aircraft, if any, revenue is recognized when the customer has obtained control of the aircraft and the customer has requested the arrangement, the aircraft is separately identified as belonging to the customer, the aircraft is ready for physical transfer to the customer and the Corporation does not have the ability to use the product or direct it to another customer.

The Corporation accounts for a significant financing component on orders where timing of cash receipts and revenue recognition differ substantially. There are certain orders related to aircraft where advances were received well before expected delivery and therefore a financing component has been accounted for separately. The result is that interest expense is accrued during the advance period and the transaction price will be increased by a corresponding amount.

Revenues from the sale of pre-owned aircraft are recognized at the point in time when the customer has obtained control of the promised asset and the Corporation has satisfied the performance obligation.

Services – Aftermarket services are generally recorded over time. The measure of progress toward complete satisfaction of the performance obligation is generally determined by comparing the actual costs incurred to the total costs anticipated for the entire contract. The expected benefits to be received are generally limited to the revenues from the associated contract. Spare parts are recognized at the point in time when the customer has obtained control of the promised asset and the Corporation has satisfied the performance obligation.

Other – Revenues earned by the Corporation on the sale of components related to commercial aircraft programs are recognized at delivery.

Contract balances

Contract related balances comprise of contract assets and contract liabilities presented separately in the consolidated statements of financial position.

Contract assets – Are recognized when goods or services are transferred to customers before consideration is received or before the Corporation has an unconditional right to payment for performance completed to date. Contract assets are subsequently transferred to receivables when the right of payment becomes unconditional. Contract assets comprise cost incurred and recorded margins in excess of progress billings on service contracts.

Contract liabilities – Are recognized when amounts are received from customers in advance of transfer of goods or services. Contract liabilities are subsequently recognized in revenue as or when the Corporation performs under contracts. Contract liabilities comprise advances on aerospace programs and other deferred revenues related to operation and maintenance of systems.

A net position of contract asset or contract liability is determined for each contract. The cash flows in respect of advances are classified as cash flows from operating activities.

Government assistance and refundable advances

Government assistance, including wage subsidies and investment tax credits, is recognized when there is a reasonable assurance that the assistance will be received and that the Corporation will comply with all relevant conditions. Government assistance related to the acquisition of inventories, PP&E and intangible assets is recorded as a reduction of the cost of the related asset. Government assistance related to incurred expenses is recorded as a reduction of the related expenses. Wage subsidies are recorded as a reduction of inventories or the related wage expenses.

Government refundable advances are recorded as a financial liability if there is reasonable assurance that the amount will be repaid. Government refundable advances are adjusted if there is a change in the number of aircraft to be delivered and the timing of delivery of aircraft. Government refundable advances provided to the Corporation to finance research and development activities on a risk-sharing basis are considered part of the Corporation’s operating activities and are therefore presented as cash flows from operating activities in the statement of cash flows.

Provisions

Provisions are recognized when the Corporation has a present legal or constructive obligation as a result of a past event, it is probable that an outflow of resources will be required to settle the obligation and the cost can be reliably estimated. These liabilities are presented as provisions when they are of uncertain timing or amount. Provisions are measured at their present value.

Product warranties – A provision for assurance type warranties is recorded in cost of sales when the revenue for the related product is recognized. The interest component associated with product warranties, when applicable, is recorded in financing expense. The cost is estimated based on a number of factors, including the historical warranty claims and cost experience, the type and duration of warranty coverage, the nature of products sold and in service and counter-warranty coverage available from the Corporation’s suppliers. Claims for reimbursement from third parties are recorded if their realization is virtually certain. Product warranties typically range from one to five years.

Restructuring provisions – Restructuring provisions are recognized only when the Corporation has an actual or a constructive obligation. The Corporation has a constructive obligation when a detailed formal plan identifies the business or part of the business concerned, the location and number of employees affected, a detailed estimate of the associated costs and an appropriate timeline. Furthermore, the affected employees or worker councils must have been notified of the plan’s main features.

Onerous contracts – If it is more likely than not that the unavoidable costs of meeting the obligations under a firm contract exceed the economic benefits expected to be received under it, a provision for onerous contracts is usually recorded in cost of sales, except for the interest component, which is recorded in financing expense. Unavoidable costs include the costs that relate directly to the contract such as anticipated cost overruns, expected costs associated with late delivery penalties and technological problems, as well as allocations of costs that relate directly to the contract. Provisions for onerous contracts are measured at the lower of the expected cost of fulfilling the contract and the expected cost of terminating the contract.

Termination benefits – Termination benefits are usually paid when employment is terminated before the normal retirement date or when an employee accepts voluntary redundancy in exchange for these benefits. The Corporation recognizes termination benefits when it is demonstrably committed, through a detailed formal plan without possibility of withdrawal, to terminate the employment of current employees.

Environmental costs – A provision for environmental costs is recorded when environmental claims or remedial efforts are probable and the costs can be reasonably estimated. Legal asset retirement obligations and environmental costs of a capital nature that extend the life, increase the capacity or improve the safety of an asset or that mitigate, or prevent environmental contamination that has yet to occur, are included in PP&E and are generally amortized over the remaining useful life of the underlying asset. Costs that relate to an existing condition caused by past operations and that do not contribute to future revenue generation are expensed and included in cost of sales.

Litigation – A provision for litigation is recorded in case of legal actions, governmental investigations or proceedings when it is probable that an outflow of resources will be required to settle the obligation and the cost can be reliably estimated.

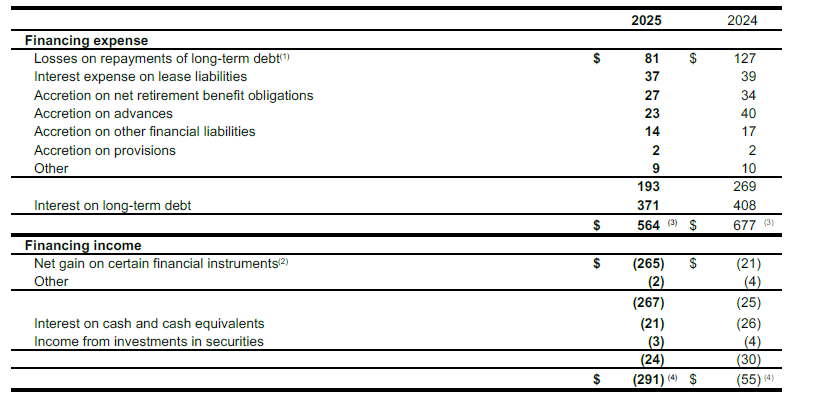

8. FINANCING EXPENSE AND FINANCING INCOME

Financing expense and financing income were as follows, for fiscal years:

(1) Represents the losses related to the full repayment of the Senior Notes due 2026 and 2027 for fiscal year 2025 (the losses related to the partial repayment of the Senior Notes due 2026 and 2027 for fiscal year 2024). Refer to Note 27 – Long-term debt for more information.

(2) Net gain on certain financial instruments classified as FVTP&L, which includes call options on long-term debt.

(3) Of which $385 million represents the interest expense calculated using the effective interest rate method for financial liabilities classified as amortized cost for fiscal year 2025 ($425 million for fiscal year 2024).

(4) Of which $21 million represents the interest income calculated using the effective interest rate method for financial assets classified as amortized cost and FVOCI for fiscal year 2025 ($26 million for fiscal year 2024).

Borrowing costs capitalized to PP&E and intangible assets totaled $13 million for fiscal year 2025, using an average capitalization rate of 7.36% ($13 million and 7.52% for fiscal year 2024). Capitalized borrowing costs are deducted from the related interest on long-term debt or accretion on other financial liabilities, if any.

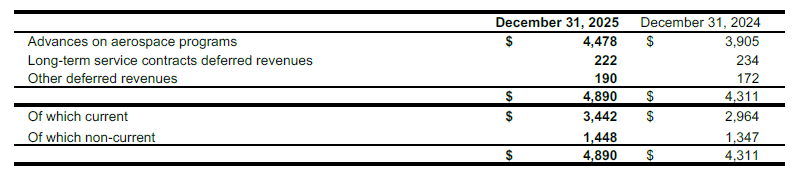

15. CONTRACT BALANCES

Contract assets represent costs incurred and recorded margins on service contracts in the amount of $157 million and $138 million as at December 31, 2025 and December 31, 2024, respectively.

Contract liabilities were as follows, as at:

Revenues recognized were as follows, for fiscal years:

17. BACKLOG

The following table presents the aggregate amount of the revenues expected to be realized in the future from partially or fully unsatisfied performance obligations as we perform under contracts at delivery or recognized over time. The amounts disclosed below represent the value of firm orders only. Such orders may be subject to future modifications that might impact the amount and/or timing of revenue recognition. The amounts disclosed below do not include unexercised options or letters of intent.

Revenues expected to be recognized in:

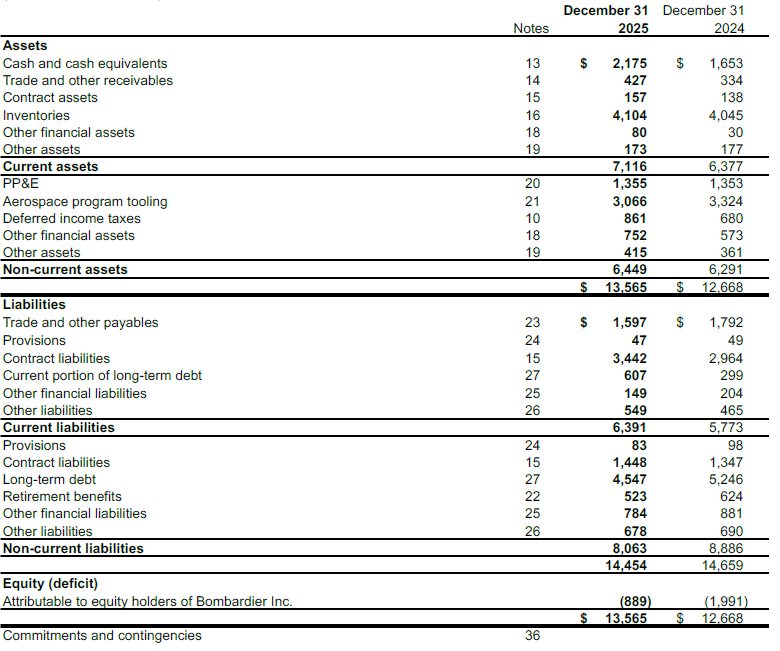

BOMBARDIER INC.

CONSOLIDATED STATEMENTS OF FINANCIAL POSITION

As at

(in millions of U.S. dollars)