Mercedes-Benz Group AG – Annual report – 31 December 2025

Industry: automotive

1. Material accounting policies (extract)

Leasing

Leases include all contracts that transfer the right to use a specified asset for a stated period of time in exchange for consideration, even if the transfer of the right to use such asset is not explicitly described in the contract. The Group is a lessee mainly of real estate properties and a lessor of its products.

The Mercedes-Benz Group as lessee

The Mercedes-Benz Group as a lessee recognizes for generally all lease contracts right-of-use assets as well as leasing liabilities for the outstanding lease payments. Variable lease payments that are not included in the initial recognition of the right-of-use asset are recognized as an expense for the period.

The Mercedes-Benz Group applies both recognition exemptions for leases with a lease term of twelve months or less (short-term leases) and for leases for which the underlying asset is of low value, not to recognize a right-of-use asset and a lease liability. The lease payments associated with those leases are predominantly recognized as an expense on a straight-line basis over the lease term.

Right-of-use assets, which are included under property, plant and equipment, are initially recognized at cost. The cost of a right-of-use asset comprises the amount of the initial measurement of the lease liability, any lease payments made at or before the commencement date, any initial direct costs and an estimate of costs to be incurred in dismantling or removing the underlying asset. All leasing incentives already received from the lessor are deducted.

Lease liabilities, which are assigned to financing liabilities, are measured initially at the present value of the lease payments still to be made. The lease liabilities include the following lease payments:

- fixed payments including de facto fixed payments less lease incentives from the lessor

- variable lease payments linked to an index or interest rate

- amounts expected to be payable under residual-value guarantees

- the exercise price of a purchase option, when exercise is estimated to be reasonably certain, and

- contractual penalties for the termination of a lease if the lease term reflects the exercise of a termination option

In contracts that contain both lease and non-lease components, the option of foregoing a separation of these components is generally used with regard to the relevant lease payments.

Lease payments are discounted at the rate implicit in the lease if that rate can readily be determined. Otherwise, discounting is at the incremental borrowing rate. This incremental borrowing rate as a risk-adjusted interest rate is derived on a maturity and currency specific basis. As the cash flow pattern of the reference interest rates (bullet maturity) does not correspond to the cash flow pattern of a lease contract (annuity), a duration adjustment in order to account for that difference is used.

A right-of-use asset is subsequently measured at cost less any accumulated depreciation and, if necessary, any accumulated impairment. If the lease transfers ownership of the underlying asset to the lessee at the end of the lease term or if the cost of the right-of-use asset reflects that the lessee will exercise a purchase option, the right-of-use asset is depreciated to the end of the useful life of the underlying asset. Otherwise, the right-of-use asset is depreciated to the end of the lease term. The depreciation of right-of-use assets is recognized within functional costs.

In the subsequent measurement of a lease liability, the carrying amount is increased to reflect interest on the lease liability and reduced to reflect the lease payments made. The interest due on the lease liability is a component of interest expense. Extension and termination options are part of a number of leases, particularly of real estate. In determining the lease term, those options are only considered if their exercise is reasonably certain. During the term, these options are regularly checked with regard to their probability of being exercised.

The Mercedes-Benz Group as lessor (equipment on operating leases)

The opportunities and risks associated with a leased asset are used to assess whether economic ownership of the leased asset is attributable to the lessor (operating leases) or the lessee (finance leases) as part of the lease of a Group product.

For operating leases the economic ownership of the vehicle remains at the Mercedes-Benz Group. Additionally, an operating lease may have to be reported with sales of vehicles for which the Group enters into a repurchase obligation.

For operating leases in particular, certain assumptions are regularly made about the residual value of returns from leasing transactions. If changing market developments at the balance sheet date lead to a negative deviation from previously estimated assumptions, the residual value must be adjusted or an impairment carried out. Depending on the region and the current market situation, the risk-mitigation measures taken generally include continuous market monitoring as well as, if required, price-setting strategies or sales-promotion measures designed to regulate vehicle inventories. The residual value estimate is generally verified by regular comparisons of internal and external sources, and, if required, the determination of residual values is adjusted and further developed with regard to methods, processes and systems.

In the case of accounting as an operating lease, these vehicles are capitalized at the (amortized) cost of production under equipment on operating leases and are depreciated over the contract term on a straight-line basis with consideration of the expected residual values. Changes in the expected residual values lead either to prospective adjustments of the scheduled depreciation or, if there are indications, to an impairment loss. The vehicles are allocated to the segment which bears substantially all of the residual-value risk. Excluded from this are the operating lease agreements described in the following paragraph.

Operating leases also relate to vehicles, primarily Group products, that Mercedes-Benz Financial Services acquires from non-Group dealers or other third parties and leases to end customers. These vehicles are presented at (amortized) cost of acquisition under equipment on operating leases in the Mercedes-Benz Financial Services segment. If these vehicles are Group products and are subsidized, the subsidy is passed on to the external customer as part of the leasing contract. This leads to a reduction in acquisition costs and a corresponding reduction of revenue from vehicle sales. After revenue is received from the sale to independent dealers, these Group products generate revenue from lease payments and subsequent resale on the basis of the separate leasing contracts.

In the case of finance leases, the Group presents the receivables under receivables from financial services in an amount corresponding to the net investment of the lease agreements. The net investment in a lease is determined by discounting the gross investment (future lease payments and non-guaranteed residual value) using the interest rate implicit in the lease.

Sustainability related aspects in connection with the recognition and measurement of assets and liabilities

The recoverability of leased vehicles classified as operating leases is reviewed regularly. When determining recoverability, the residual value of the leased

vehicles is particularly relevant. As a result of the transformation towards an electrification of the vehicle fleet, residual values can be influenced by changing

customer behaviour, new regulatory requirements and further technological developments. For example, stricter emissions regulations, increasing demand for

zero-emission vehicles, and technological innovations can significantly influence the residual value of vehicles. No significant impairment losses were required for

vehicles with gasoline or diesel engines in the reporting year. For all-electric vehicles and plug-in hybrid vehicles, impairment losses of the leased items were recorded

due to the factors mentioned above. These are shown in Note 12.

The recoverability of inventories is also regularly reviewed. Information on the impairment of inventories is presented in Note 18.

The expected proceeds from the disposal of vehicles pledged as collateral are taken into account in the determination of expected credit losses for receivables from financial services. The expected proceeds from the disposal are based on an estimate of the market value at the expected time of a possible default. An analysis regarding a possible increase in the default risk and a reduction of the estimated market values

resulting from a shift in customer behaviour due to climate change effects or other sustainability risks was conducted as of the reporting date. An insignificant additional allowance for credit losses was recognized on the affected receivables.

2. Accounting estimates and management judgements (extract)

Recoverable amount of equipment on operating leases

Based on the decision of whether the economic ownership of the leased asset in the context of leasing a Group product is attributable to the lessor (operating leases) or the lessee (finance leases) the Mercedes-Benz Group regularly reviews the factors determining the values of its leased vehicles from operating leases (carrying amount as of 31 December 2025: €39,472 million; 31 December 2024: €45,220 million). In particular, it is necessary to estimate the residual values of vehicles, which constitute a substantial part of the expected future cash inflows from equipment on operating leases. In this context, assumptions are made regarding major influencing factors, such as the expected number of returned leased vehicles and the latest remarketing results. Those assumptions are determined by qualified estimates. The qualified estimates are based on publications by expert third parties and data from external market research institutes as well as internal calculations and additional information available, such as historical experience and current sales data.

In addition, knowledge about new regulatory requirements or changes in customer behaviour is included in the residual value estimates. The residual values thus determined serve as a basis for scheduled depreciation; changes in residual values lead either to a prospective adjustment of the scheduled depreciation or, in the case of a significant decline in expected residual values, to an impairment. If scheduled depreciation is prospectively adjusted, changes in estimates of residual values do not have a direct effect but are equally distributed over the remaining term of the lease contract.

11. Property, plant and equipment including right-of-use assets (extract)

Property, plant and equipment as shown in the Consolidated Statement of Financial Position with a carrying amount of €27,340 million (2024: €26,537 million) also includes right-of-use assets that the Group received as lessee. Property, plant and equipment, including right-of-use assets, developed as shown on the following page.

In 2025, government grants of €26 million (2024: €30 million) were deducted from the carrying amount of property, plant and equipment.

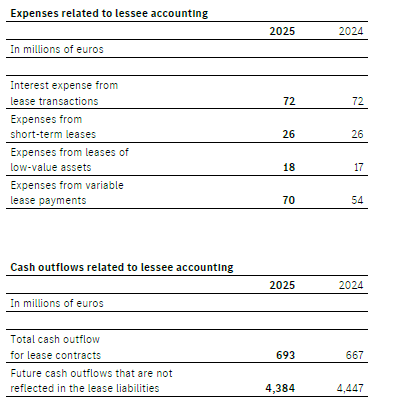

The following tables show additional disclosures related to lessee accounting.

Further information on lessee accounting is provided in Note 24 and Note 32.

Property, plant and equipment including right-of-use assets

12. Equipment on operating leases

The revenue received from the sale of Group products to external dealers – plus in particular any dealer margin – is estimated by the Group as being of the magnitude of the respective addition to leased equipment at Mercedes-Benz Financial Services. These vehicles generate revenue from lease payments and subsequent resale on the basis of the separate leasing contracts. In 2025, additions to leased equipment from these vehicles at Mercedes-Benz Financial Services amounted to €11.9 billion (2024: €11.4 billion).

At 31 December 2025, equipment on operating leases with a carrying amount of €11,306 million was pledged as security for liabilities from ABS transactions (2024: €10,890 million). These liabilities related to a securitization transaction of future lease payments on leased vehicles. Further information is provided in Note 24.

In 2025, impairment losses of €0.1 billion on all-electric vehicles were recorded in the Consolidated Statement of Income. The prior year included €0.4 billion for plugin hybrid vehicles and all-electric vehicles in the Mercedes-Benz Cars segment.

Lease payments

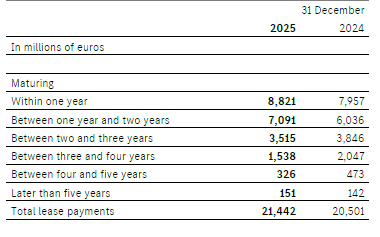

Maturities of lease payments under operating lease agreements to be paid by lessees to the Mercedes-Benz Group in the future are as follows.

Maturity of undiscounted lease payments for equipment on operating leases

14. Receivables from financial services

Types of receivables

Receivables from sales financing with customers include receivables from credit financing for non-Group third parties who purchased their vehicle either from a dealer or directly from the Mercedes-Benz Group.

Receivables from sales financing with dealers represent loans for floor financing programmes for vehicles purchased from the Mercedes-Benz Group. In addition, these receivables also relate to the financing of other assets that the dealers purchased from third parties, in particular used vehicles or property.

Receivables from finance lease contracts consist of receivables from leasing contracts for which all substantial risks and opportunities incidental to the leasing business are transferred to the lessee.

In 2025, the Mercedes-Benz Group realized a profit from finance lease contracts of €136 million (2024: €110 million).

At 31 December 2025, receivables from financial services with a carrying amount of €8,116 million (2024: €10,536 million) were pledged mostly as collateral for liabilities from ABS transactions. Further information is provided in Note 24.

Receivables from financial services1

1 At balance sheet date, €430 million were attributable to the reclassification of the balance sheet item “Assets held for sale” of the Consolidated Statement of Financial Position.

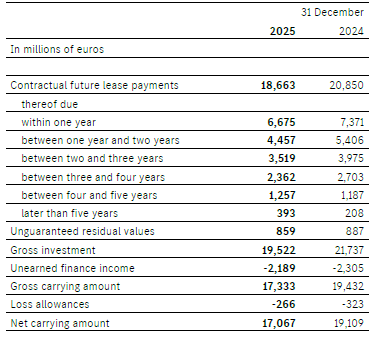

The following table shows the maturities of the future contractual lease payments and the development of lease payments to the carrying amounts of receivables from finance lease contracts.

Development of the receivables from finance lease contracts

As of 31 December 2024, unguaranteed residual values of €4,242 million have been reported. For better comparability, €3,355 million unguaranteed residual values were reclassified into contractual future lease payments to the extent that these relate to exercise prices of purchase options for which the exercise of the option is considered reasonably certain.

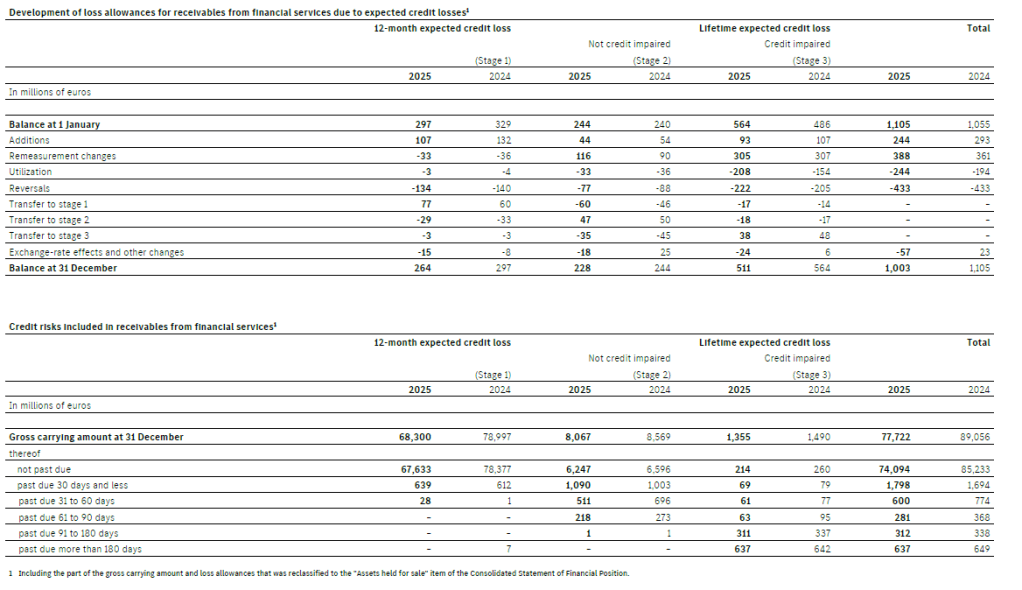

Loss allowances

The loss allowances for receivables from financial services due to expected credit losses are shown in the table “Development of loss allowances for receivables from financial services due to expected credit losses”. The carrying amounts of receivables from financial services based on modified contracts that are shown in stage 2 and 3 amounted to €586 million at 31 December 2025 (2024: €580 million). In addition, carrying amounts of €140 million in connection with contractual modifications were reclassified at 31 December 2025 from stage 2 and 3 into stage 1 (2024: €91 million).

Credit risks

Information on credit risks included in receivables from financial services is shown in the table “Credit risks included in receivables from financial services”.

Longer overdue periods regularly lead to higher loss allowances.

At the beginning of the contracts, collaterals of usually at least 100% of the carrying amounts are agreed; these are backed by the vehicles based on the underlying contracts. Over the term of the contracts, the performance of the collateral is continuously included in the calculation of the risk provision to be recognized, so the net carrying amounts of the credit-impaired contracts are essentially backed by the underlying vehicles.

Further information on loss allowances, financial risks and types of risks is provided in Note 32.

24. Financing liabilities

In the year 2025, bonds totalling €6,414 million (2024: €17,504 million) were issued. Due to redemptions, the bonds were reduced by €11,253 million (2024: €12,415 million).

Furthermore, liabilities to financial institutions decreased by €1,888 million to €24,427 million in 2025.

In addition, asset-backed securities (ABS) transactions with a total financing volume of €10,177 million (2024: €13,957 million) were carried out in 2025. In the reporting period, €10,670 million (2024: €11,933 million) was repaid.

Further information on the maturities of lease liabilities as of 31 December 2025 is provided in Note 32.

Financing liabilities1

1 At balance sheet date, €500 million were attributable to the reclassification of the balance sheet item “Liabilities held for sale” of the Consolidated Statement of Financial Position.

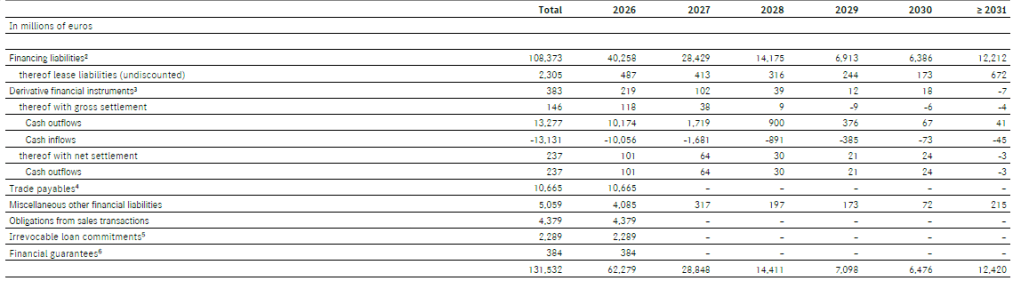

32. Management of financial risks (extract)

The following overview of liquidity runoff shows how the cash flows in connection with liabilities, derivative financial instruments and irrevocable loan commitments and financial guarantees as of 31 December 2025 may affect the Group’s future liquidity situation.

Liquidity runoff at 31 December 2025 for liabilities and financial guarantees1

1 The amounts were calculated as follows:

(a) If the counterparty can request payment at different dates, the liability is included on the basis of the earliest date on which the Mercedes-Benz Group can be required to pay. The customer deposits of Mercedes-Benz Bank are therefore mostly considered in this analysis to mature within the first year.

(b) The interest payments of floating-interest financial instruments are estimated on the basis of forward rates.

2 The stated cash flows of financing liabilities consist of their undiscounted principal and interest payments.

3 The undiscounted sum of the payments of the derivative financial liabilities is shown for the respective year.

4 The cash outflows of trade payables are undiscounted.

5 The maximum available amounts are stated.

6 The maximum potential obligations under the issued financial guarantees are stated. It is assumed that the amounts are due within the first year.