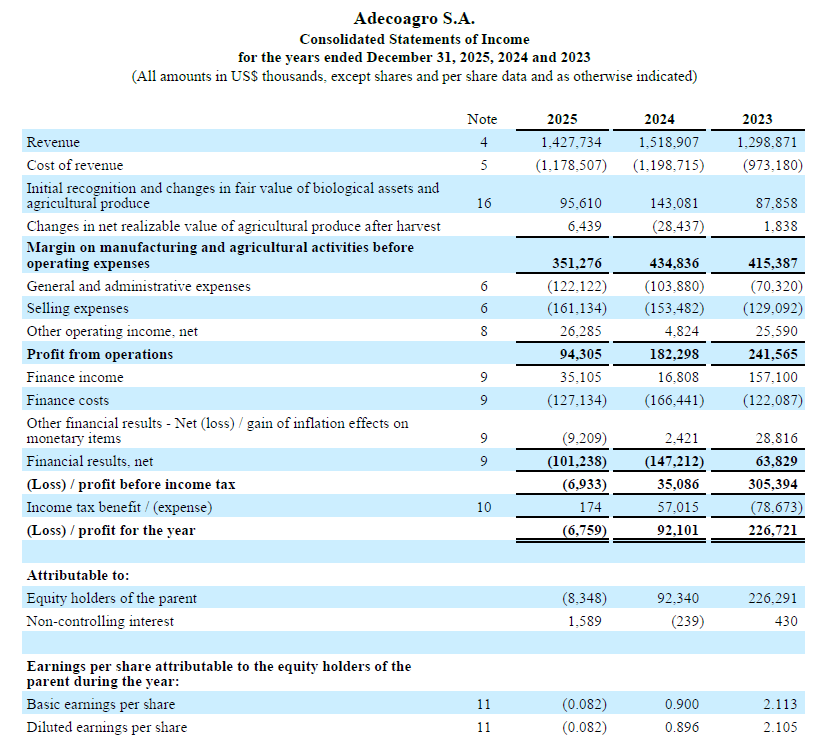

Adecoagro S.A. – Annual report – 31 December 2025

Industry: agriculture

Notes to the Consolidated Financial Statements

(All amounts in US$ thousands, except shares and per share data and as otherwise indicated)

33. Summary of material accounting policies (extract)

33.11 Biological assets

Biological assets comprise growing crops (mainly corn, wheat, soybeans, sunflower peanuts and rice), sugarcane and livestock (growing herd and cattle for dairy production).

The Group distinguishes between consumable and bearer biological assets, and between mature and immature biological assets. “Consumable” biological assets are those assets that may be harvested as agriculture produce or sold as biological assets, for example livestock intended for dairy production. “Bearer” biological assets are those assets capable of producing more than one harvest, for example sugarcane or livestock from which raw milk is produced. “Mature” biological assets are those that have attained harvestable specifications (for consumable biological assets) or are able to sustain regular harvests (for bearer biological assets). “Immature” biological assets are those assets other than mature biological assets.

Costs are capitalized as biological assets if, and only if, (a) it is probable that future economic benefits will flow to the entity, and (b) the cost can be measured reliably. The Group capitalizes costs such as: planting, harvesting, weeding, seedlings, irrigation, agrochemicals, fertilizers and a systematic allocation of fixed and variable production overheads that are directly attributable to the management of biological assets, among others. Costs that are expensed as incurred include administration and other general overhead and unallocated production overhead, among others.

Biological assets, both at initial recognition and at each subsequent reporting date, are measured at fair value less costs to sell, except where fair value cannot be reliably measured. Cost approximates fair value when little biological transformation has taken place since the costs were originally incurred or the impact of biological transformation on price is not expected to be material.

Gains and losses that arise on measuring biological assets at fair value less costs to sell and measuring agricultural produce at the point of harvest at fair value less costs to sell are recognized in the statement of income in the period in which they arise in the line item “Initial recognition and changes in fair value of biological assets and agricultural produce”.

Where there is an active market for a biological asset or agricultural produce, quoted market prices in the most relevant market are used as a basis to determine the fair value. Otherwise, when there is no active market or market-determined prices are not available, fair value of biological assets is determined through the use of valuation techniques.

Therefore, the fair value of biological assets is generally derived from the expected discounted cash flows of the related agricultural produce. The fair value of the agricultural produce at the point of harvest is generally derived from market determined prices.

A general description of the determination of fair values based on the Company’s business segments follow:

- Growing crops including rice:

Growing crops, for which biological growth is not significant, are measured at cost, which approximates fair value. Expenditure on growing crops includes land preparation expenses and other direct expenses incurred during the sowing period including labor, seedlings, agrochemicals and fertilizers among others.

Otherwise, biological assets are measured at fair value less estimated point-of-sale costs at initial recognition and at any subsequent period. Point-of-sale costs include all costs that would be necessary to sell the assets

The fair value of growing crops including rice is measured based on a formula, which takes into consideration the estimate of crop yields, estimated market prices and costs, and discount rates. Estimated yields are determined based on several factors including location of farmland, environmental conditions and other restrictions and growth at the time of measurement. Yields are multiplied by sown hectares to determine the estimated tons of crops including rice to be obtained. The tons are then multiplied by a net cash flow determined at the future crop prices less the direct costs to be incurred. This amount is discounted at a discount rate, which reflects current market assessments of the assets involved and the time value of money.

- Growing herd and cattle:

Livestock are measured at fair value less estimated point-of-sale costs, with any changes therein recognized in the statement of income, on initial recognition as well as subsequently at each reporting period. The fair value of livestock is determined based on the actual selling prices less estimated point-of-sale costs in the markets where the Group operates.

- Sugarcane:

Sugarcane planting costs form part of Property plant and equipment. The agricultural produce growing on sugarcane is classified as biological assets and are measured at fair value less cost to sell. The fair value of agricultural produce growing on sugarcane depends on the variety, location and maturity of the plantation.

Agricultural produce growing in the Sugarcane, for which biological growth is not significant, is valued at cost, which approximates fair value. Expenditure on the agricultural produce growing in the sugarcane consists mainly of labor, agrochemicals and fertilizers among others. When it has attained significant biological growth, it is measured at fair value through a discounted cash flow model. Estimated revenues are based on estimated yearly production volume (which will be destined to sugar, ethanol, energy and raw cane production) and the price is calculated as the average of daily prices for sugar future contracts (Sugar #11 ICE-NY contracts) for a six months period. Projected costs include maintenance and land leasing among others. These estimates are discounted at an appropriate discount rate.

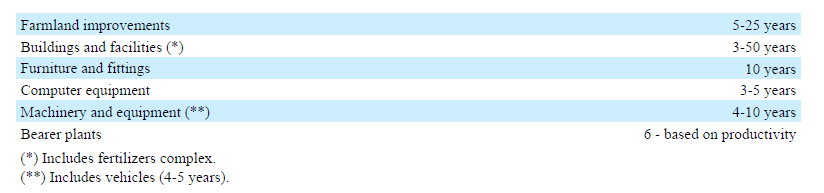

33.5 Property, plant and equipment

Farmlands are initially recorded at fair value and are subsequently measured under the revaluation model based on periodic, but at least annual, valuations prepared by an external independent expert. A revaluation reserve is credited in shareholders’ equity. All other property, plant and equipment is recorded at cost, less accumulated depreciation and impairment losses, if any. Historical cost comprises the purchase price and any costs directly attributable to the acquisition. Under the definition of Property plant and equipment includes the bearer plants, such as sugarcane.

Where individual components of an item of property, plant and equipment have different useful lives, they are accounted for as separate items, which are depreciated separately.

Subsequent costs are included in the asset’s carrying amount or recognized as a separate asset, as appropriate, only when it is probable that future economic benefits associated with the item will flow to the Group and the cost of the item can be measured reliably. The carrying amount of the replaced part is derecognized. All other repairs and maintenance are charged to the statement of income when they are incurred.

Major overhauls that restore an asset’s service capacity and are required for its continued use are capitalized when the recognition criteria are met and are depreciated over the period until the next major overhaul (generally on a straight-line basis). Costs of renewals and improvements that extend an asset’s useful life and/or improve its service capacity are capitalized when the recognition criteria are met. All other repairs and ordinary maintenance are charged to profit or loss when incurred.

Gains and losses on disposals are determined by comparing the proceeds with the carrying amount and are recognized within “Other operating income, net” in the consolidated statement of income.

32. Material accounting estimates and judgments (extract)

(b) Biological assets

The nature of the Group’s biological assets and the basis of determination of their fair value are explained under Note 33.11. The discounted cash flow model requires the input of highly subjective assumptions including observable and unobservable data. Generally the estimation of the fair value of biological assets is based on models or inputs that are not observable in the market and the use of such unobservable inputs is significant to the overall valuation of the assets. These inputs are determined based on the best information available, for example by reference to historical information of past practices and results, statistical and agronomic information, and other analytical techniques. The discounted cash flow model includes significant assumptions relating to the cash flow projections including future market prices, estimated yields at the point of harvest, estimated production cycle, future costs of harvesting and other costs, and estimated discount rate.

Market prices are generally determined by reference to observable data in the principal market for the agricultural produce. Harvesting costs and other costs are estimated based on historical and statistical data. Yields are estimated based on several factors including the location of the farmland and soil type, environmental conditions, infrastructure and other restrictions and growth at the time of measurement. Yields are subject to a high degree of uncertainty and may be affected by several factors out of the Group’s control including but not limited to extreme or unusual weather conditions, plagues and other crop diseases, among other factors.

The significant assumptions discussed above are highly sensitive. Reasonable shifts in assumptions including but not limited to increases or decreases in prices, costs and discount factors used would result in a significant increase or decrease to the fair value of biological assets. In addition, cash flows are projected over a number of years and based on estimated production. Estimates of production in themselves are dependent on various assumptions, in addition to those described above, including but not limited to several factors such as location, environmental conditions and other restrictions. Changes in these estimates could materially impact on estimated production, and could therefore affect estimates of future cash flows used in the assessment of fair value (see Note 16).

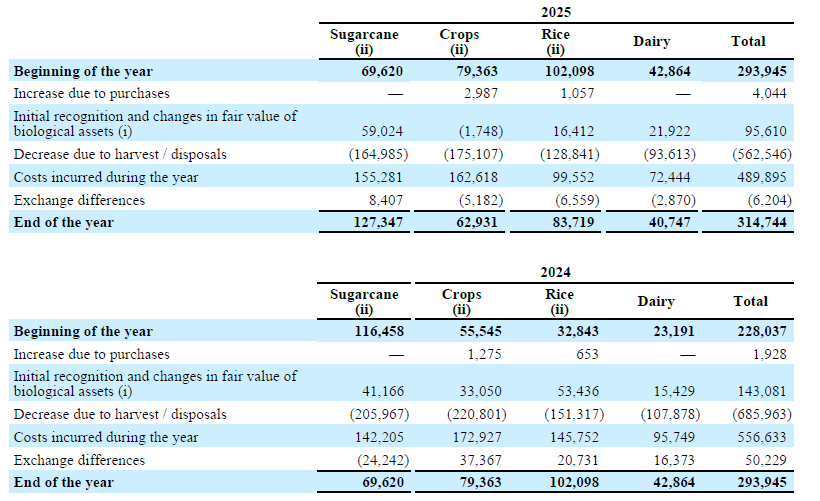

16. Biological assets

Changes in the Group’s biological assets in 2025 and 2024 were as follows:

(i) Biological asset with a production cycle of more than one year (that is dairy cattle) generated “Initial recognition and changes in fair value of biological assets” amounting to US$(22,321) for the year ended December 31, 2025 (2024: US$14,263). In 2025, an amount of US$(5,132) (2024: US$525) was attributable to price changes, and an amount of US$(17,190) (2024: US$13,738) was attributable to physical changes.

(ii) Biological assets that are measured at fair value within level 3 of the hierarchy.

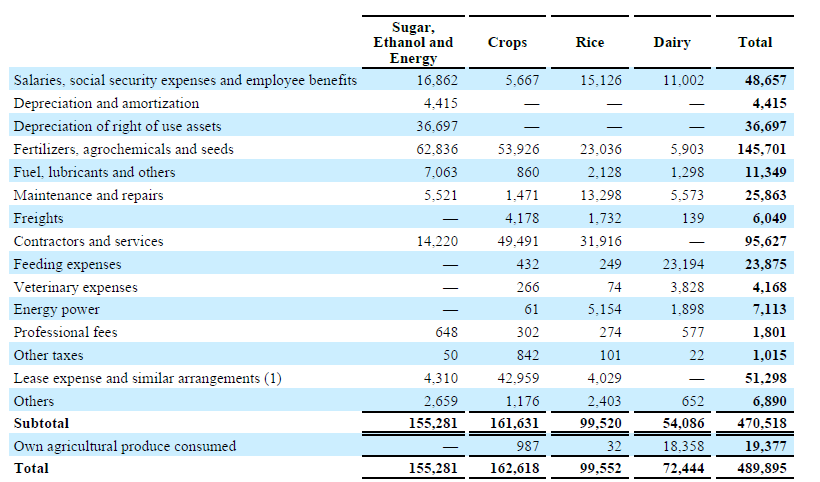

Cost of production for the year ended December 31, 2025:

(1) Correspond mainly to lease arrangement short term.

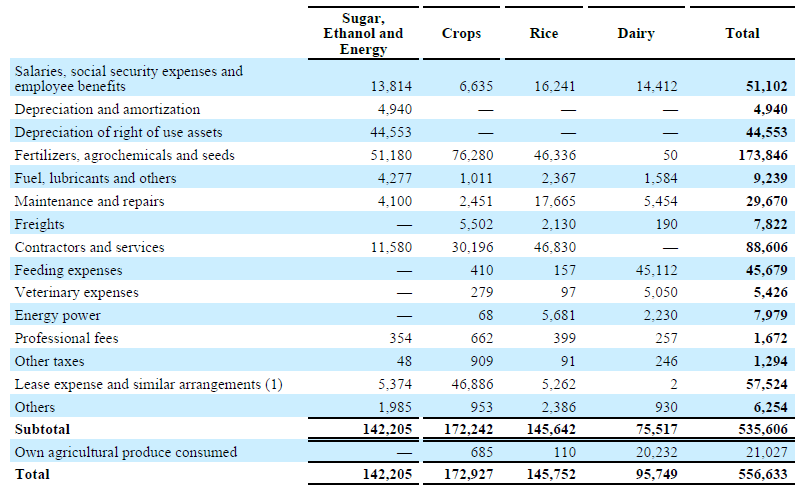

Cost of production for the year ended December 31, 2024:

(1) Correspond mainly to lease arrangement of short term periods.

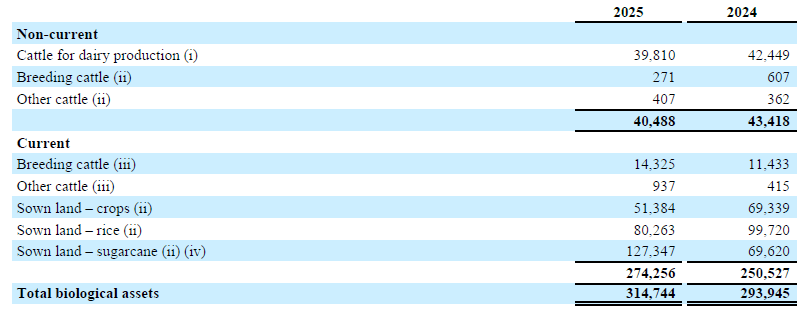

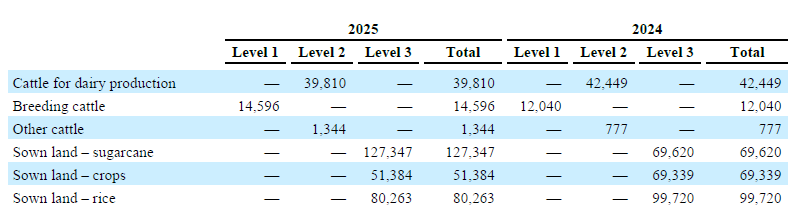

Biological assets in December 31, 2025 and 2024 were as follows:

(i) Classified as bearer and mature biological assets.

(ii) Classified as consumable and immature biological assets.

(iii) Classified as consumable and mature biological assets.

(iv) It includes US$7,837 and US$6,254 of crops planted in sugarcane farms.

The fair value less estimated point of sale costs of agricultural produce at the point of harvest amounted to US$468,933 for the year ended December 31, 2025 (2024: US$578,085).

The following table presents the Group’s biological assets that are measured at fair value at December 31, 2025 and 2024 (See Note 17 for the description of each fair value level):

There were no transfers between any levels during the year.

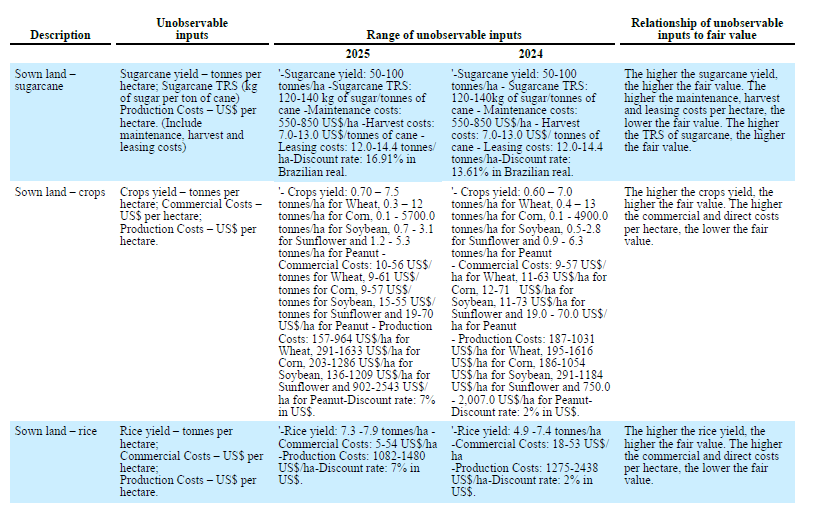

The following significant unobservable inputs were used to measure the Group’s biological assets using the discounted cash flow valuation technique:

As of December 31, 2025, the impact of a reasonable 10% increase / (decrease) in estimated costs, with all other variables held constant, would result in a decrease (increase) in the fair value of the Group’s biological asset less cost to sell of US$23.3 million for sugarcane, US$3.4 million for crops and US$6.5 million for rice.

As of December 31, 2024, the impact of a reasonable 10% increase / (decrease) in estimated costs, with all other variables held constant, would result in a decrease (increase) in the fair value of the Group’s biological asset less cost to sell of US$23.3 million for sugarcane, US$3.4 million for crops and US$6.5 million for rice.

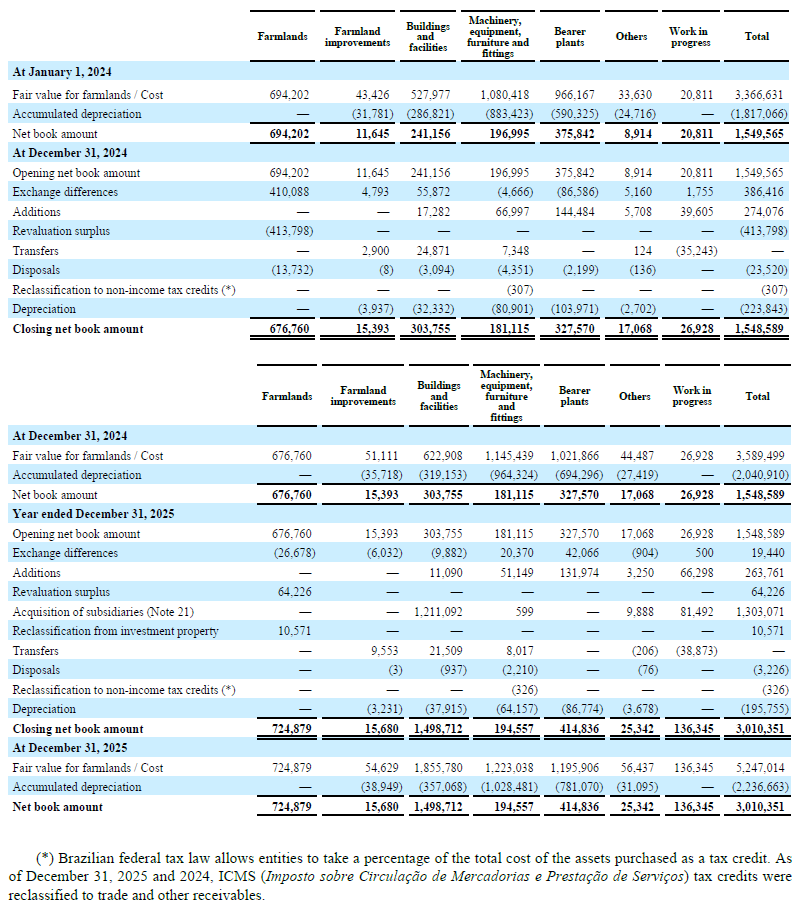

12. Property, plant and equipment, net

Changes in the Group’s property, plant and equipment, net in 2025 and 2024 were as follows:

Depreciation is calculated using the straight-line method to allocate their cost over the estimated useful lives. Farmlands are not depreciated, except for bearer plants.

The assets’ residual values and useful lives are reviewed, and adjusted if appropriate, at each statement of financial position date. Farmlands are measured at fair value using a sales comparison approach. prepared by an independent expert. Sale prices of comparable properties are adjusted considering the specific aspects of each property, the most relevant assumption being the price per hectare (Level 3). The Group estimated that, other factors being constant, a 5% reduction on the sales price for the year ended December 31, 2025 would have reduced the value of the farmlands on US$36.2 million (2024:

US$33.8 million), which would impact, net of its tax effect on the “Revaluation surplus” item in the statement of Changes in Shareholders’ Equity. Should farmlands be carried at historical cost, the net book value as of December 31, 2025 would have been US$288.1 million.

Depreciation charges are included in “Cost of production of Biological Assets,” “Cost of production of manufactured products,”“General and administrative expenses,”“Selling expenses” and capitalized in “Property, plant and equipment” for the years ended December 31, 2025, 2024 and 2023.

During the year ended December 31, 2025, borrowing costs of US$4.0 million (2024:US$4.9 million) were capitalized as components of the cost of acquisition or construction for qualifying assets.

Certain of the Group’s assets had been pledged as collateral to secure the Group’s borrowings and other payables. The net book value of the pledged assets amounts to US$205.1 million, both as of December 31, 2025 and 2024. As of December 31, 2025, all borrowings that had assets as guaranty were canceled. We are in the process of lifting the pledges.

2. Financial risk management (extracts)

- End-product price risk

Prices for commodity products have historically been cyclical, reflecting overall economic conditions and changes in capacity within the industry, which affect the profitability of entities engaged in the agribusiness industry. The Group combines different actions to minimize price risk. A percentage of crops are to be sold during and post-harvest period. The Group manages minimum and maximum prices for each commodity as well as gross margin per each crop as to decide when and how to sell. End-product price risks are hedged if economically viable and possible by entering into forward contracts with major trading houses or by using derivative financial instruments, consisting mainly of crops and sugar future contracts, but also includes occasionally put and call options. A movement in end-product futures prices would result in a change in the fair value of the end product hedging contracts. These fair value changes, after taxes, are recorded in the consolidated statement of income. The prices of Urea is affected by the volatility of the products in the international reference markets, affecting the margins and the results of operations of our fertilizer business segment.

Contract positions are designed to ensure that the Group would receive a defined minimum price for certain quantities of its production. The counterparties to these instruments generally are major financial institutions. In entering into these contracts, the Group has assumed the risk that might arise from the possible inability of counterparties to meet the terms of their contracts. The Group does not expect any material losses as a result of counterparty defaults. The Group is also obliged to pay margin deposits and premiums for these instruments. These estimates represent only the sensitivity of the financial instruments to market risk and not the Group exposure to end product price risks as a whole, since the crops and cattle products sales are not financial instruments within the scope of IFRS 7 disclosure requirements.

- Derivative financial instruments

As part of its business operations, the Group may uses a variety of derivative financial instruments to manage its exposure to the financial risks discussed above. As part of its strategy, the Group may enter into derivatives of (i) interest rate to manage the composition of floating and fixed rate debt; (ii) currency to manage exchange rate risk, and (iii) crop (future contracts and put and call options) to manage its exposure to price volatility stemming from its integrated crop production activities. The Group’s policy is not to use derivatives for speculative purposes.

Derivative financial instruments involve, to a varying degree, elements of market and credit risk not recognized in the financial statements. The market risk associated with these instruments resulting from price movements is expected to offset the market risk of the underlying transactions, assets and liabilities, being hedged. The counterparties to the agreements relating to the Group’s contracts generally are large institutions with credit ratings equal to or higher than BBB+. The Group continually monitors the credit rating of such counterparties and seeks to limit its financial exposure to any one financial institution. While the contract or notional amounts of derivative financial instruments provide one measure of the volume of these transactions, they do not represent the amount of the Group’s exposure to credit risk. The amounts potentially subject to credit risk (arising from the possible inability of counterparties to meet the terms of their contracts) are generally limited to the amounts, if any, by which the counterparties’ obligations under the contracts exceed the Group’s obligations to the counterparties.

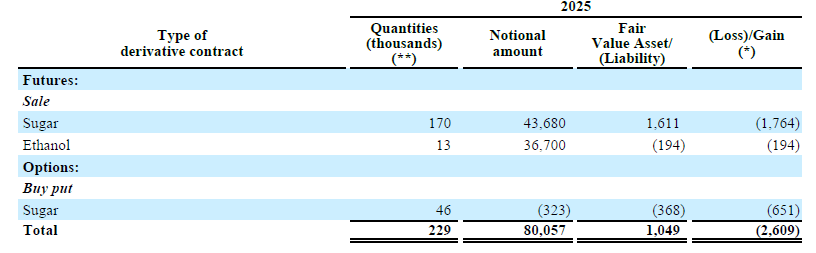

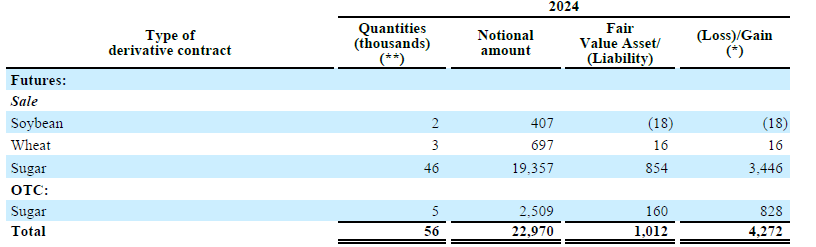

The following tables show the outstanding positions for each type of derivative contract as of the date of each statement of financial position:

▪ Futures / options

As of December 31, 2025:

As of December 31, 2024:

(*) Included in the line item “gain / (loss) from commodity derivative financial instruments” of Note 8.

(**) All quantities expressed either in tons or cubic meters, as applicable.

Commodity future contract fair values are computed with reference to quoted market prices on future exchanges.