Fomento Economico Mexicano S.A.B. de C.V. – Annual report – 31 December 2017

Industry: food and drink

2.3 Critical accounting judgments and estimates (extract)

2.3.2 Judgements (extract)

2.3.2.3 Venezuela exchange rates and deconsolidation

As is further explained in Note 3.3 below, as of December 31,2017, the exchange rate used to translate the financial statements of the Company’s Venezuelan subsidiary for reporting purposes into the consolidated financial statements was 22,793 bolivars per U.S. dollar.

As is also explained in Note 3.3 below, effective December 31, 2017 the Company deconsolidated its Coca-Cola FEMSA subsidiary’s operations in Venezuela due to the challenging economic environment in that country and began accounting for the operations under the fair value method.

Note 3. Significant Accounting Policies (extract)

3.3 Foreign currencies, consolidation of foreign subsidiaries and accounting for investments in associates and joint ventures

In preparing the financial statements of each individual subsidiary and accounting for investments in associates and joint ventures, transactions in currencies other than the individual entity’s functional currency (foreign currencies) are recognized at the rates of exchange prevailing at the dates of the transactions. At the end of each reporting period, monetary items denominated in foreign currencies are retranslated at the rates prevailing at that date. Non-monetary items that are measured in terms of historical cost in a foreign currency are not retranslated.

Exchange differences on monetary items are recognized in consolidated net income in the period in which they arise except for:

- The variations in the net investment in foreign subsidiaries generated by exchange rate fluctuation which are included in other comprehensive income, which is recorded in equity as part of accumulated translation adjustment within the cumulative other comprehensive income.

- Intercompany financing balances with foreign subsidiaries are considered as long-term investments when there is no plan to pay such financing in the foreseeable future. Monetary position and exchange rate fluctuation regarding this financing is recorded in the exchange differences on translation of foreign operations within the accumulated other comprehensive income (loss) item, which is recorded in equity.

- Exchange differences on transactions entered into in order to hedge certain foreign currency risks.

Foreign exchange differences on monetary items are recognized in profit or loss. Their classification in the income statement depends on their nature. Differences arising from fluctuations related to operating activities are presented in the “other expenses” line (see Note 19) while fluctuations related to non-operating activities such as financing activities are presented as part of “foreign exchange gain (loss)” line in the income statement.

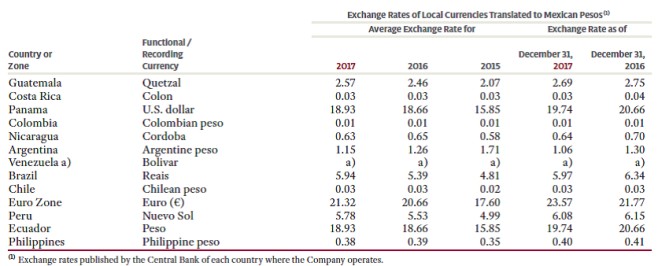

For incorporation into the Company’s consolidated financial statements, each foreign subsidiary, associates or joint venture’s individual financial statements are translated into Mexican pesos, as follows:

- For hyperinflationary economic environments, the inflation effects of the origin country are recognized pursuant IAS 29 Financial Reporting in Hyperinflationary Economies, and subsequently translated into Mexican pesos using the year-end exchange rate for the consolidated statements of financial position and consolidated income statement and comprehensive income; and

- For non-hyperinflationary economic environments, assets and liabilities are translated into Mexican pesos using the year-end exchange rate, equity is translated into Mexican pesos using the historical exchange rate, and the income statement and comprehensive income is translated using the exchange rate at the date of each transaction. The Company uses the average exchange rate of each month if the exchange rate does not fluctuate significantly.

In addition, in relation to a partial disposal of a subsidiary that does not result in the Company losing control over the subsidiary, the proportionate share of accumulated exchange differences are re-attributed to non-controlling interests and are not recognized in profit or loss. For all other partial disposals (i.e., partial disposals of associates or joint ventures that do not result in the Company losing significant influence or joint control), the proportionate share of the accumulated exchange differences is reclassified to profit or loss. In September 2017, the Company sold shares equal to 5.2% of economic interest in Heineken, consequently it reclassified the proportionate share of the accumulated exchange differences, recognized previously in other comprehensive income, for a total profit of Ps. 6,632 to the consolidated statement of income.

Goodwill and fair value adjustments on identifiable assets and liabilities acquired arising on the acquisition of a foreign operation are treated as assets and liabilities of the foreign operation and translated at the rate of exchange prevailing at the end of each reporting period. Foreign exchange differences arising are recognized in equity as part of the cumulative translation adjustment.

The translation of assets and liabilities denominated in foreign currencies into Mexican pesos is for consolidation purposes and does not indicate that the Company could realize or settle the reported value of those assets and liabilities in Mexican pesos. Additionally, this does not indicate that the Company could return or distribute the reported Mexican peso value in equity to its shareholders.

a) Venezuela

Effective December 31, 2017, the Company determined that the deteriorating conditions in Venezuela had led Coca-Cola FEMSA to no longer meet the accounting criteria to consolidate its Venezuelan subsidiary. Such deteriorating conditions had significantly impacted Coca-Cola FEMSA’s ability to manage its capital structure, its capacity to purchase raw materials and limitations of portfolio dynamics. In addition, certain government controls over pricing, restriction over labor practices, acquisition of U.S. dollars and imports, has affected the normal course of business. Therefore, and due to the fact that its Venezuelan subsidiary will continue doing operations in Venezuela, as of December 31, 2017, Coca-Cola FEMSA changed the method of accounting for its investment in Venezuela from consolidation to fair value measured using a Level 3 concept.

As a result of the deconsolidation, Coca-Cola FEMSA also recorded an extraordinary loss within other expenses for an amount of Ps. 28,177 on December 31, 2017. Such effect includes the reclassification of Ps. 26,123 to the income statement previously recorded within accumulated foreign currency translation losses in equity, impairment equal to Ps. 745 and Ps. 1,098 mainly from distribution rights and property, plant and equipment, respectively, and Ps. 210 for the remeasurement at fair-value of Venezuelan investment.

Prior to deconsolidation, during 2017, Coca-Cola FEMSA’s Venezuelan operations contributed Ps. 4,005 to net sales, and losses of Ps. 2,223 to net income. It’s total assets were Ps. 4,138 and the total liabilities were Ps. 2,889.

Beginning January 1, 2018, Coca-Cola FEMSA will recognize its investment in Venezuela under the fair value method following the new IFRS 9 Financial Instruments standard.

Until December 31, 2017, Coca-Cola FEMSA’s recognition of its Venezuelan operations involved a two-step accounting process in order to translate into bolivars all transactions in a different currency than bolivars and then to translate the bolivar amounts to Mexican Pesos.

Step-one.- Transactions are first recorded in the stand-alone accounts of the Venezuelan subsidiary in its functional currency, which is bolivar. Any non-bolivar denominated monetary assets or liabilities are translated into bolivars at each balance sheet date using the exchange rate at which Coca-Cola FEMSA expects them to be settled, with the corresponding effect of such translation being recorded in the income statement. See 3.4 below.

As of December 31, 2016 Coca-Cola FEMSA had U.S. $629 million in monetary liabilities recorded using DIPRO (Divisa Protegida) exchange rate at 10 bolivars per U.S. dollar, mainly because as of that date Coca-Cola FEMSA belived it continued to qualify for that rate to pay for the import of various products into Venezuela, and its ability to renegotiate with their main suppliers, if necessary, the settlement of such liabilities in bolivars. In addition, Coca-Cola FEMSA has U.S. $104 million recorded at DICOM (Divisas Complementarias) exchange rate at 673.76 bolivars per U.S. dollar.

Step-two.- In order to integrate the results of the Venezuelan operations into the consolidated figures of Coca-Cola FEMSA, such Venezuelan results are translated from Venezuelan bolivars into Mexican pesos.

In December 2017, Coca-Cola FEMSA translated the Venezuela entity figures at an exchange rate of 22,793 bolivars per U.S. dollar, as such exchange rate better represents the economic conditions in Venezuela. Coca-Cola FEMSA considers that this exchange rate provides more useful and relevant information with respect to Venezuela’s financial position, financial performance and cash flows. On January 30, 2018, a new auction of the DICOM celebrated by Venezuela’s government resulted on an estimated exchange rate of 25,000 bolivar per U.S. dollar.

3.4 Recognition of the effects of inflation in countries with hyperinflationary economic environments

The Company recognizes the effects of inflation on the financial information of its Venezuelan subsidiary that operates in hyperinflationary economic environments (when cumulative inflation of the three preceding years is approaching, or exceeds, 100% or more in addition to other qualitative factors), which consists of:

- Using inflation factors to restate non-monetary assets, such as inventories, property, plant and equipment, intangible assets, including related costs and expenses when such assets are consumed or depreciated;

- Applying the appropriate inflation factors to restate capital stock, additional paid-in capital, net income, retained earnings and items of other comprehensive income by the necessary amount to maintain the purchasing power equivalent in the currency of Venezuela on the dates such capital was contributed or income was generated up to the date those consolidated financial statements are presented; and

- Including the monetary position gain or loss in consolidated net income.

The Company restates the financial information of subsidiaries that operate in hyperinflationary economic environment using the consumer price index of each country (CPI).

As disclosed in Note 3.3, Coca-Cola FEMSA deconsolidated its operations in Venezuela. Consequently, there will not be financial impacts associated to inflation adjustments in future financial statements, however, Coca-Cola FEMSA’s Venezuelan subsidiary will continue operating.

As of December 31, 2017, 2016, and 2015, the operations of the Company are classified as follows:

a) Argentina

a) Argentina

As of December 2017 and 2016 there are multiple inflation indices (including combination of indices in the case of CPI) or certain months without official available information in the case of National Wholesale Price Index (WPI), as follows:

i) CPI for the City and Greater Buenos Aires Area (New CPI-CGBA), for which the IMF noted improvements in quality, this new consumer price index will only be provided for periods after April 2016 and does not provide national coverage.

ii) “Coeficiente de Estabilización de Referencia” (CER or Reference Stabilization Ratio) to calculate the three-year cumulative inflation rate in Argentina, the CER is used by the government of Argentina to adjust the rate they pay on certain adjustable rate bonds they issue. At April 30, 2017, the three-year cumulative inflation rate based on CER data is estimated to be approximately 95.5%.

iii) WPI with a cumulative inflation for three years of 92.2% at November 2016 but not including information for November and December 2015 since it was not published by the National Bureau of Statistics of Argentina (INDEC). The WPI has historically been viewed as the most relevant inflation measure for companies by practitioners in Argentina.

As a result of the existence of multiple inflation indices, the Company believes it necessitates an increased level of judgment in determining whether the economy of Argentina should be considered highly inflationary.

The Company believes that general market sentiment is that on the basis of the quantitative and qualitative indicators in IAS 29, the economy of Argentina should not be considered as hyperinflationary as of December 31, 2017. However, it is possible that certain market participants and regulators could have varying views on this topic both during 2017 and as Argentina’s economy continues to evolve in 2018. The Company will continue to carefully monitor the situation and make appropriate changes if and when necessary.

13.2 Other financial assets

(1) Investment in Venezuela subsidiary, Coca-Cola FEMSA determined that the deteriorating conditions in Venezuela had led the Company to no longer meet the accounting citeria to consolidate its Venezuelan subsidiary, the impacts of such deconsolidation are discussed in Note 3.3 above.

As of December 31, 2017 and 2016, the fair value of long term accounts receivable amounted to Ps. 707 and Ps. 541, respectively. The fair value is calculated based on the discounted value of contractual cash flows whereby the discount rate is estimated using rates currently offered for receivable of similar amounts and maturities, which is considered to be level 2 in the fair value hierarchy.