International Consolidated Airlines Group S.A. – Annual report – 31 December 2024

Industry: airline

2 Significant accounting policies (extract)

Change in presentation of results (extract)

Balance sheet – presentation of convertible bond

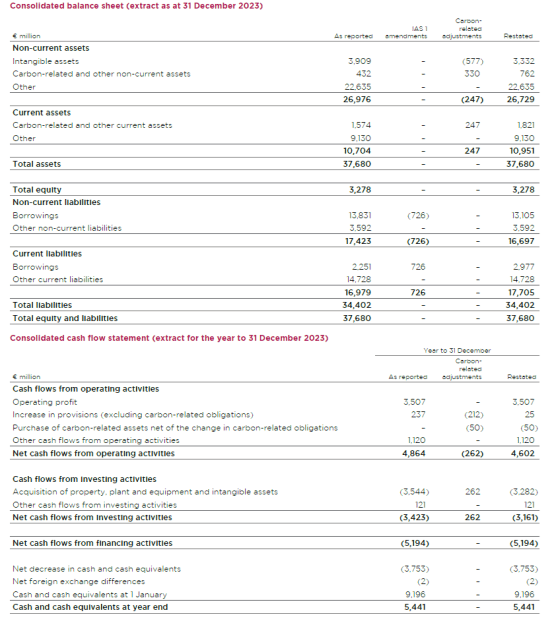

On 31 October 2022, the IASB issued the amendments to IAS 1 – Classification of liabilities as current or non-current (‘the Amendments’), which the Group has adopted from 1 January 2024. The Amendments require the €825 million convertible bond that matures in 2028 to be reclassified from a non-current liability to a current liability with the comparative presentation at 31 December 2023 also reclassified.

The Amendments require that where the conversion feature of a convertible instrument does not meet the recognition criteria for separate presentation within equity, and where the associated bondholders have the irrevocable right to exercise the conversion feature within 12 months of the balance sheet date, such convertible instruments be presented as current.

As a result, the prior year Balance sheet includes a reclassification to conform with the current year presentation of non-current and current Borrowings. Refer to note 37 for further details.

37 Change in accounting policies

The Group has applied the amendments to IAS 1 for the first for the year to 31 December 2024 with the year to 31 December 2023 restated to conform with the current presentation of the Balance sheet. Further information is given in note 2.

In addition, while the Group has maintained its accounting policy for emissions allowances, it has, during the year to 31 December 2024, changed how it presents the associated assets and liabilities in the Balance sheet and associated classification in the Cash flow statement. Further information is given in note 2.

The following tables summarise the impacts of these changes on the Balance sheet as at 31 December 2023 and on the Cash flow statement for the year to 31 December 2023: