Slater and Gordon Limited – Annual report – 30 June 2016

Industry: support services

1.3 Adoption of New Accounting Standards

The Group adopted all the new mandatory standards and interpretations for the current reporting period. The adoption of these standards and interpretations did not result in a material change on the reported results and position of the Group as they did not result in any changes to the Group’s existing accounting policies.

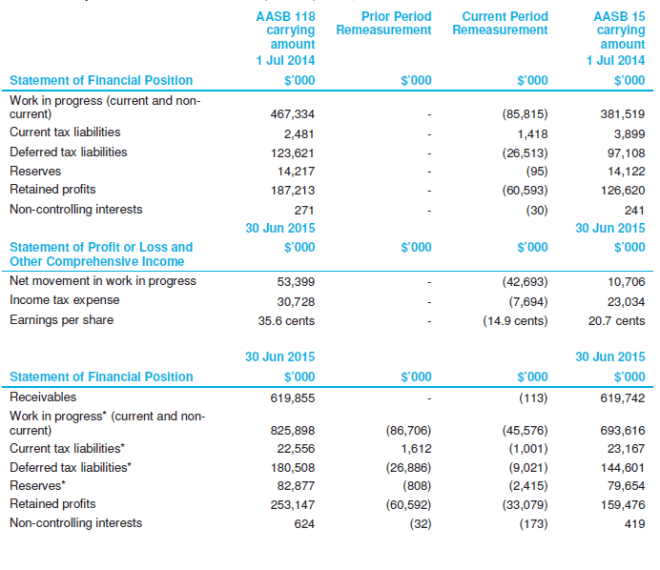

The Group has elected to early adopt AASB 15 Revenue from Contracts with Customers as issued in December 2014, which would otherwise be mandatorily effective for annual reporting periods beginning on or after 1 January 2018. The initial application date for the Group is 1 July 2015. The Group elected to apply the standard on a full retrospective basis as permitted by AASB 15 whereby the cumulative effect of retrospective application is recognised by adjusting opening retained profits or other relevant components of equity for the earliest comparative period presented (which for the Group is the comparative period beginning on 1 July 2014). See below for further details on the key impacts arising from the adoption of the new standard. Refer to Note 3.1 for additional details, however key judgements adopted as part of the adoption of the new standard include:

(i). Estimating variable consideration

Prior to the adoption of AASB 15, in previous reporting periods, variable consideration expected to be received from services (including services provided on a No Win – No Fee basis) was estimated based on historical average fees and success outcomes.

Under AASB 15, where consideration in respect of a contract is variable, revenue can only be recognised to the extent that it is highly probable that the cumulative amount of revenue recognised in respect of a contract will not be subject to a significant reversal when the uncertainty associated with the variable consideration is subsequently resolved (this is referred to as the “constraint” requirements). As a result, the Group has applied the new constraint requirements in estimating the amount of variable consideration included in the transaction price compared to the amount of variable consideration previously included.

(ii). Stage of completion As a result of more detailed requirements under AASB 15 with respect to measuring the stage of completion of a performance obligation, the Group has conducted a review of its methodology for measuring progress towards completion of relevant performance obligations.

In summary, as a result of early adopting AASB 15 on a full retrospective basis, the following adjustments were made to the amounts recognised in the statement of financial position and statement of profit or loss and other comprehensive income at 1 July 2014 and at the end of the comparative period (30 June 2015):