Sasol Limited – Annual report – 30 June 2025

Industry: oil and gas, mining

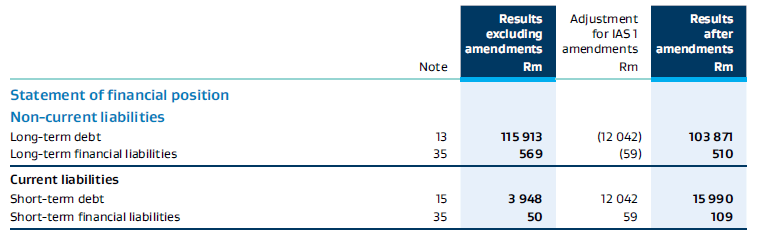

Amendments to IAS 1 ‘Presentation of Financial Statements’

The Group has applied “Classification of Liabilities as Current or Non-current and Non-current liabilities with Covenants – Amendments to IAS 1”, as issued in 2020 and 2022, which were effective for the Group from 1 July 2024. The amendments apply retrospectively for annual reporting periods beginning on or after 1 January 2024.

The amendments provide guidance on the classification of liabilities as current or non-current in the statement of financial position and does not impact the amount or timing of recognition of any asset, liability income or expenses, or the information that entities disclose about those items. The amendments clarify that the classification of liabilities as current or non-current should be based on rights that are in place at the end of the reporting period which enable the reporting entity to defer settlement by at least twelve months. The amendments further make it explicit that classification is unaffected by expectations or events after the reporting date.

The amendments are applicable to the net debt to EBITDA covenant (as defined in the debt agreements) on our revolving credit facility (RCF) and term loan. As the Group’s current practice is aligned to the clarification provided by the amendments, the adoption thereof has not significantly impacted the Group.

The amendments also cover how a company classifies a liability that can be settled in its own shares – e.g. convertible debt. When a liability includes a counterparty conversion option that involves a transfer of the company’s own equity instruments, the conversion option is recognised as either equity or a liability separately from the host liability. The amendments now clarify that when a company classifies the host liability as current or non-current, it ignores only those conversion options that are recognised as equity.

The conversion feature contained in the Group’s US$750 million convertible bond was bifurcated and accounted for separately from the host liability as an embedded derivative financial liability. Previously the Group ignored all counterparty conversion options, whether they were recognised as equity or liabilities, when classifying the related liabilities as current or non-current. This amendment resulted in the host liability and embedded derivative liability being classified as current liabilities retrospectively.

The Group’s other liabilities were not impacted by the amendments.

The impact of applying the amendments for the year ended 30 June 2024 is:

The amendments had no impact on the balances of 2023.