Ultra Electronics Holdings plc – Annual report – 31 December 2015

Industry: manufacturing

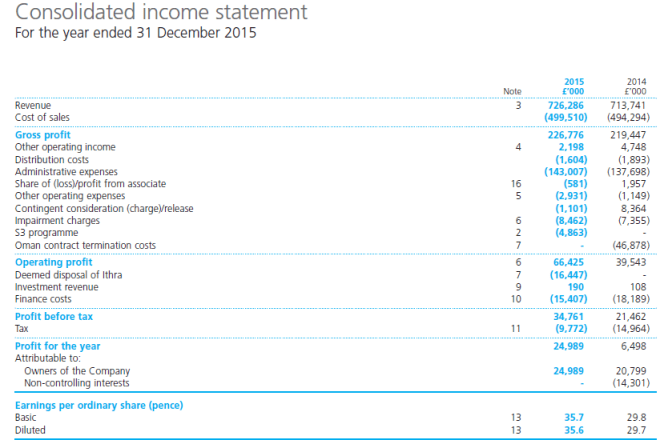

7 Deemed disposal of Ithra

On 4 March 2015, ‘Ithra’ (“Ultra Electronics in collaboration with Oman Investment Corporation LLC”), the legal entity established with the sole purpose of delivering the Oman Airport IT contract, was placed into voluntary liquidation. A liquidator was appointed and is pursuing claims against the customer on behalf of the interested parties. Ithra, upon liquidation, no longer meets the IFRS 10 criteria for consolidation as a subsidiary of the Group and is, consequently, a deemed disposal as at 4 March 2015.

During 2014 the full expected cost of the Oman contract termination of £46,878,000 was charged to the consolidated income statement and impacted the Group’s profit for the year in 2014. The loss attributable to the Oman Investment Corporation (‘OIC’) non-controlling interest of £14,301,000 was credited to reserves as mandated by IFRS 10 para B94. Upon deemed disposal, the existing non-controlling interest of £13,751,000 is not permitted to be debited back against reserves, even though the cost has already been reflected in full on the face of the 2014 income statement, and is consequently recycled through the income statement, together with £2,696,000 of foreign exchange losses recorded in the translation reserve over the life of the entity. The net charge booked to exceptional Oman termination related costs in the 2015 income statement is as follows: