The Village Building Co. Limited – Annual report – 30 June 2017

Industry: real estate

NOTE 3. CRITICAL ACCOUNTING JUDGEMENTS, ESTIMATES AND ASSUMPTIONS (extract 1)

The preparation of the financial statements requires management to make judgements, estimates and assumptions that affect the reported amounts in the financial statements. Management continually evaluates its judgements and estimates in relation to assets, liabilities, contingent liabilities, revenue and expenses. Management bases its judgements, estimates and assumptions on historical experience and on other various factors, including expectations of future events, management believes to be reasonable under the circumstances. The resulting accounting judgements and estimates will seldom equal the related actual results. The judgements, estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities (refer to the respective notes) within the next financial year are discussed below.

NOTE 3. CRITICAL ACCOUNTING JUDGEMENTS, ESTIMATES AND ASSUMPTIONS (extract 2)

Revenue

Identifying the separate performance obligations in a contract with a customer

Most of the revenue recognised by the Group relates to contracts with customers for the sale of land, house and land packages and apartments as well as services revenue generated from construction, project management and selling activities. In accounting for these contracts, the Group is required to identify which promised goods or services are distinct and therefore represent separate performance obligations to which revenue is assigned. Management uses judgement to determine whether a good or service is distinct by assessing if the customer can benefit from the promised good or service on its own or together with other resources that are readily available to the customer and by ascertaining whether the Group’s promise to transfer the good or service to the customer is separately identifiable from other promises in the contract.

Determination of transaction prices for revenue recognition

The Group is required to determine the transaction price in respect of each of its contracts with customers. Where consideration is variable due to a contract containing liquidated damages provisions or where the consideration is based on a percentage of the customer’s gross property sales, the Group uses the ‘constants on estimates approach’ to estimate the amount of variable consideration to be is included in the transaction price. Management uses judgement based on significant industry experience to determine this amount and whether the variable consideration is constrained and adjusts the transaction price accordingly.

In determining the transaction price, management also assesses the existence of any significant financing component based on whether the timing of payments agreed to by the parties to the contract provides the customer or the Group with a significant benefit of financing.

Allocation of transaction price to performance obligations in contracts with customers

The Group uses the stand-alone selling price of the distinct goods and services underlying each performance obligation to apportion the transaction price to identified performance obligations.

Satisfaction of performance obligations for revenue recognition

The Group assesses each of its customer contracts to determine whether performance obligations are satisfied over time or at a point in time in order to determine when revenue is recognised. Refer to note 4 for further details.

Transfer of control when performance obligation satisfied at a point in time

Significant judgement is required to determine when control over the asset is transferred to the customer which is the point in time when revenue is recognised. Refer to note 4 for further details.

Method of measuring progress of completion of performance obligations and recognition of revenue

For performance obligations satisfied over time, management uses judgement to select a method for measuring its progress towards complete satisfaction of that performance obligation. In exercising that judgement, management selects a method that depicts its performance in transferring control of goods or services to the customer. For the provision of construction services, management has determined that progress should be measured using quantity surveyor reports (an output method). For the provision of project management services, management has determined that progress should be measured based on consultant spend (an input method) and is calculated as the amount of consultant spend incurred year to date as a percentage of total estimated consultant spend for the contract. For selling services, management has determined that progress should be measured over the short period of time relating to the procedural steps required in finalising a transaction of sale of a property to a purchaser.

NOTE 4. REVENUE

To the extent the Group has contract assets and liabilities, they are detailed in notes 9 and 13.

Accounting for revenue recognition

The Group recognises revenue to depict the transfer of promised goods or services to customers in an amount that reflects the consideration to which it expects to be entitled in exchange for those goods or services. Revenue is recognised at an amount that reflects the consideration that the Group is expected to be entitled to in exchange for transferring goods or services to a customer, using a five-step model for each revenue stream.

Revenue from contracts with customers

Most of the revenue recognised by the Group relates to sales generated from contracts with customers for construction services. In accounting for these contracts, the Group recognises revenue in an amount that reflects the consideration to which it expects to be entitled in exchange for goods or services. For each contract with a customer, the Group:

- identifies the contract with a customer;

- identifies the performance obligations in the contract;

- determines the transaction price;

- allocates the transaction price to the performance obligations in the contract; and

- recognises revenue when (or as) each performance obligation is satisfied in a manner that depicts the transfer to the customer of the goods or services promised.

The Group first identifies and accounts for each contract, or group of contracts, with a customer that establishes enforceable rights and obligations. A subsequent change in the price or scope of a contract that is approved by the parties to the contract is a contract modification. Depending on the price of the modification and on nature of the goods or services promised, the modification may be accounted for as either a separate contract, the termination of the existing contract and the creation of a new contract, or a modification of the existing contract.

At contract inception, the Group identifies the performance obligations in the contract. A performance obligation is a promise to transfer a distinct good or service to the customer. A good or service is distinct if the customer can benefit from the good or service on its own or together with other resources that are readily available to the customer and the Group’s promise to transfer the good or service to the customer is separately identifiable from other promises in the contract.

The transaction price is determined as the amount of the consideration in a contract to which the Group expects to be entitled in exchange for transferring the promised goods or services. In many of the Group’s contracts, the transaction price is fixed. However, the contracts may have a variable component such as liquidated damages provisions or the consideration is based on a percentage of the customer’s gross property sales. If the consideration is variable, the Group estimates the amount of variable consideration using either a ‘most likely’ method or an ‘expected value’ method. Variable consideration is included in the transaction price only to the extent that it is highly probable that a significant reversal in the amount of cumulative revenue recognised will not occur when the uncertainty associated with the variable consideration is subsequently resolved. This is known as the constraint on estimates of variable consideration. The transaction price is also adjusted for the effects of the time value of money if the contract includes a significant financing component. However, the consideration is not adjusted for the effects of a significant financing component if, at contract inception, the Group expects that the period between the transfer of a promised good or service and when the customer pays for that good or service is one year or less. At the end of each reporting period, the Group updates the estimated transaction price including updating its assessment of whether an estimate of variable consideration is constrained.

The transaction price is allocated to the separate performance obligations on the basis of the relative stand-alone selling prices of each distinct good or service. Where available, the stand-alone selling price is an observable price of the good or service when it is sold separately by the Group in similar circumstances to similar customers. If a stand-alone selling price is not directly observable, it is estimated. In specific circumstances, an amount of variable consideration may be allocated to one or more performance obligations in the contract. Subsequent changes in the transaction price are allocated on the same basis as at contract inception.

Revenue is recognised when or as each performance obligation is satisfied, at the amount of the transaction price allocated to that performance obligation. A performance obligation is satisfied over time, when either the customer simultaneously receives and consumes the benefits provided by the Group’s performance, the performance creates or enhances an asset that the customer controls as the asset is created or enhanced or its performance does not create an asset with an alternative use to the Group and the Group has an enforceable right to payment for performance completed to date. Where a performance obligation is satisfied over time an ‘input method’ or an ‘output method’, as deemed appropriate by management, is used for measuring progress towards complete satisfaction of the performance obligation.

A performance obligation is satisfied at a point in time if the criteria for a good or service to be transferred over time are not met. Control of an asset refers to the ability to direct the use of, and obtain substantially all of the remaining benefits from the asset. Factors considered in determining when the customer has obtained control of a good or service at a point in time include whether the Group has obtained a present right to receive consideration; the customer has legal title to the asset; the customer has taken physical possession of the asset; the customer has the significant risks and rewards of ownership; or the customer has accepted the asset.

When a performance obligation is satisfied by transferring a promised good or service to the customer before the customer pays consideration or before payment is due, the Group presents the contract as a contract asset, unless the Group’s rights to that amount of consideration are unconditional, in which case the Group recognises a receivable. When an amount of consideration is received from a customer prior to the Group transferring a good or service to the customer, the Group presents the contract as a contract liability.

Revenue recognition with respect to the Group’s specific business activities are as follows:

(i) Land, house & land and units

The contract for the sale of land, house & land packages and units are assessed to have a number of performance obligations being the provision of finished dwellings, land and/or finishes. The Group satisfies each of these performance obligations at the point in time when control of land, house & land or unit (as appropriate) has transferred to the customer, which is at legal settlement.

(ii) Construction services

Construction of a dwelling is deemed to represent a single performance obligation to the customer, which is a performance obligation satisfied over time. The performance obligation is satisfied progressively over the construction period, with the Group’s performance being measured using the ‘output method’, by reference to regular quantity surveyor reports.

(iii) Project management fees

Project management services represent a performance obligation that is satisfied over time for the oversight and management of the development of multi-dwelling residential construction projects. Revenue is recognised using an input method, based on the percentage of consultant spend for the project incurred to date as a proportion of total project consultant spend. Consultant spend has been deemed the best measure of performance as the Group is required to manage the team of consultants in order to deliver the project. Proportion of consultant spend incurred therefore provides an appropriate input method of work performed.

(iv) Selling services

A sales service represents a performance obligation to facilitate the sale of individual dwellings which is satisfied over the short period of time relating to procedural steps of finalising transaction of sale of a property to a purchaser. The Group does not carry any obligations towards the purchaser post settlement.

Transaction price allocated to remaining performance obligations pursuant to customer contracts

The transaction price associated with unsatisfied or partially unsatisfied performance obligations does not include variable consideration that is constrained.

Revenue other than contracts with customers:

Dividend revenue

Dividend revenue is recognised when the Group’s right to receive the payment is established.

Other revenue

Other revenue is recognised when it is received or when the right to receive payment is established.

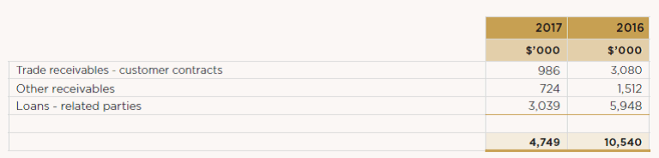

NOTE 9. RECEIVABLES

IMPAIRMENT OF RECEIVABLES

The Group has not impaired any customer contract receivables nor any other receivables during the years ended 30 June 2017 and 30 June 2016.

PAST DUE BUT NOT IMPAIRED

There were no receivables (current and non-current) that were either past due or impaired.

Accounting for receivables

Trade receivables are initially recognised at fair value and subsequently measured at amortised cost using the effective interest method, less any provision for impairment. Trade receivables are generally due for settlement within 14-35 days.

Collectability of trade receivables is reviewed on an ongoing basis. Debts which are known to be uncollectable are written off by reducing the carrying amount directly. A provision for impairment of trade receivables is raised when there is objective evidence that the Group will not be able to collect all amounts due according to the original terms of the receivables.

Other receivables are recognised at amortised cost, less any provision for impairment.

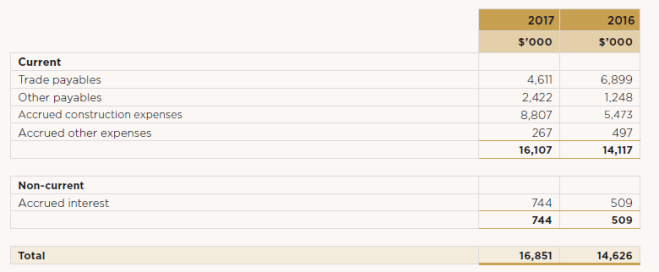

NOTE 13. TRADE AND OTHER PAYABLES

Refer to note 19 for further information on financial instruments

Accounting for trade and other payables

These amounts represent liabilities for goods and services provided to the Group prior to the end of the reporting period and which are unpaid. Due to their short-term nature, they are measured at amortised cost and are not discounted. The amounts are unsecured and are usually paid within 30 days of recognition.

Accounting for cost of sales accruals

These amounts represent accruals for goods and services provided to the Group prior to the end of the reporting period and which are unpaid.