Lonmin Plc – Annual report – 30 September 2017

Industry: mining

NOTES TO THE ACCOUNTS (extract)

29 Impairment of non-financial assets

At each financial reporting date, the Group assesses whether there is any indication that non-financial assets are impaired. If any such indication exists, the recoverable amount of the assets is estimated in order to determine the extent of the impairment (if any). The recoverable amount is the higher of fair value less costs to sell and value in use.

For impairment assessment, the Group’s net assets are grouped into CGUs being the Marikana CGU, Akanani CGU, Limpopo CGU and Other. The Marikana, Limpopo and Akanani CGUs relate to the PGM segment.

The Marikana CGU is located in the Marikana district to the east of the town of Rustenburg in the North West province of South Africa. It contains a number of producing underground mines, various development properties, concentrators and tailings storage.

The Akanani CGU is located on the Northern Limb of the Bushveld Igneous Complex in the Limpopo province of South Africa. A pre-feasibility study was completed in 2012.

The Limpopo CGU is located on the Northern Sector of the Eastern Limb of the Bushveld Igneous Complex in the Limpopo province of South Africa and comprises two resource blocks (Boabab and Boabab east). The CGU includes mines which were placed on care and maintenance in 2009 and a concentrator complex.

For the Marikana CGU the recoverable amount was calculated using a value-in-use valuation. The key assumptions contained within the business forecast and management’s approach to determine appropriate values in use are set out below:

For impairment testing, management projects cashflows over the life of the relevant mining operations which is significantly greater than five years. For the Marikana CGU a life of mine spanning until 2070 was applied. Whilst the majority of mining licences are currently valid until 2037 the Director’s expect the licences will be renewed until beyond 2070.

In arriving at the VIU for the Marikana CGU, post-tax cash flows expressed in real terms have been estimated and discounted using a post-tax discount rate of 14.2% (2016 – 12.0%), giving consideration to the specific amount and timing of future cash flows as well as the risks specific to the Marikana CGU. This equates to a pre-tax discount rate of 17.5% real (2016 – 15.6% real).

The Akanani asset was fully impaired at 30 September 2015. There have been no significant changes since that date to lead us to believe that the valuation of this asset is different. Therefore expenditure capitalised since 30 September 2015 has been fully impaired.

The non-financial assets of the Limpopo CGU were also fully impaired at 30 September 2015.

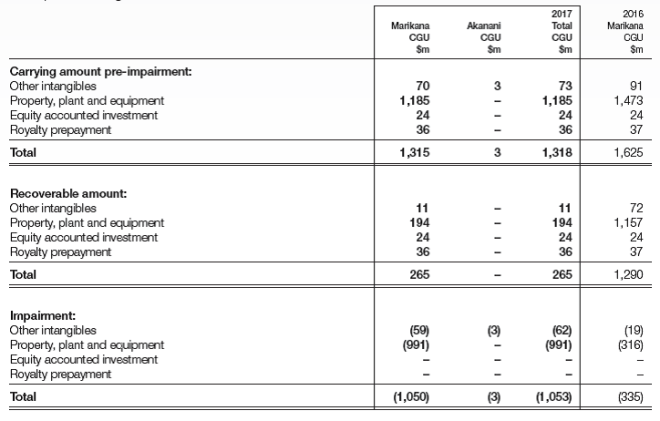

For the 2017 financial year, the Group’s non-financial assets were impaired by $1,053 million (2016 – $335 million) primarily due to changes to the Business Plan and revisions to underlying assumptions. Whilst we have made a downward revision to our Platinum price outlook this was more than offset by an upward revision on price for the other PGMs and base metals, especially Palladium. The net impact of the change in these assumptions led to the value in use declining below the carrying amount of the non-financial assets of the operations.

The impairment charge was allocated as follows:

For the Marikana CGU, the impairment charge was allocated pro-rata to intangibles and property, plant and equipment, but limited to the assets’ recoverable amounts.

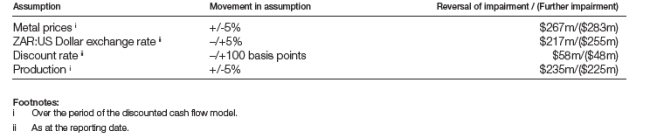

In preparing the financial statements, management has considered whether a reasonably possible change in the key assumptions on which management has based its determination of the recoverable amounts of the CGUs would cause the units’ carrying amounts to exceed their recoverable amounts. A reasonably possible change in any of the assumptions used to value the Marikana CGU will lead to a reduction or increase in the impairment charge as follows: