Sime Darby Berhad – Annual report – 30 June 2025

Industry: conglomerate

3 MATERIAL ACCOUNTING POLICIES (extract)

p. Revenue recognition

Revenue from contracts with customers is recognised by reference to each distinct performance obligation in the contract with customer. Revenue from contracts with customers is measured at its transaction price, being the amount of consideration which the Group expects to be entitled in exchange for transferring promised goods or services to a customer, net of goods and service tax, returns, rebates and discounts. Transaction price is allocated to each performance obligation on the basis of the relative standalone selling prices of each distinct good or services promised in the contract. Depending on the substance of the contract, revenue is recognised when the performance obligation is satisfied, which may be at a point in time or over time.

The material performance obligations by segment are as follows:

i. Industrial

Industrial segment revenue consists primarily of sale and installation of equipment, sale of parts and provision of after-sales services.

(a) Sale and installation of equipment, parts and provision of after-sales maintenance

Revenue from sale of equipment and after-sales maintenance are recognised respectively in the period in which the customer accepts the delivery of the goods and services rendered.

Contracts that bundle the sale of equipment, after-sales maintenance, provision of parts credit and extended warranty are recognised as distinct performance obligations for revenue recognition purposes.

Parts credit represents prepaid amounts for equipment parts which customers will redeem in the future.

Credit is given together with the sale of machine based on negotiated terms with the customer. Revenue from parts credit is recognised upon utilisation of credit for parts exchange.

Contracts that bundle the sale and installation of generator sets are recognised as a single performance obligation as the installation includes a significant integration service. Revenue is recognised progressively based on the percentage of completion determined by reference to the completion of the physical proportion of contract work to-date.

There is no significant financing component in the revenue arising from sale and installation of equipment, parts and provision of after-sales maintenance as almost all sales are made on the normal credit terms not exceeding 12 months.

(b) Construction of equipment

Contracts for construction of equipment comprise multiple deliverables which include a significant integration service and are therefore recognised as a single performance obligation. Revenue is recognised progressively based on the percentage of completion determined by reference to the completion of the physical proportion of contract work to-date.

(c) Extended warranty programme

The Group operates an extended warranty programme where customers are given additional 12-month warranty in addition to the standard warranty. Revenue for the extended warranty is recognised in the period in which the warranty services are rendered. No element of financing is deemed present as the sales are made on normal credit terms. Obligations to repair or replace faulty products under standard warranty terms is recognised as a provision.

(d) Sales with a right of return

For certain parts sales, the customer has an option to sell the used products back to the Group within an agreed timeframe after the date of sale. Therefore, a refund liability (with corresponding adjustment to revenue) is recognised using the most likely method for the products expected to be returned.

ii. Motors

The Group is an authorised distributor of vehicles and parts and also operates a network of dealerships selling vehicles and parts and offering after-sales services. Motors segment revenue consists primarily of sale of vehicles and parts, after-sales services and assembly of vehicles.

(a) Sale of vehicles and parts

Revenue from sale of vehicles and parts is recognised when the Group sells the vehicle and parts to customers and control of the vehicle and parts has transferred, being when the vehicles and parts are delivered to the customer.

The vehicles and parts are often sold with volume based discounts and incentives based on aggregate sales over an agreed period. Accumulated experience is used to estimate and provide for the discounts and incentives, using expected value or most likely methods depending on the type of discounts and incentives. Revenue is recognised to the extent that it is highly probable that a significant reversal will not occur.

Consistent with market practice, the Group collects deposits from customers for the sale of vehicles. A contract liability is recognised for the customer deposits as the Group has an obligation to transfer vehicle to the customer in respect of deposits received. Customer deposits would be recognised as revenue upon sale of the vehicle to the customer.

No element of financing is deemed present as the sales are made with a credit term of 30 to 60 days, which is consistent with market practice. The Group’s obligation to provide warranty for the vehicles and parts under the standard warranty terms is recognised as a provision.

(b) After-sales services

The Group provides after-sales services or routine vehicle maintenance services within and/or outside of the warranty period in relation to the vehicle brands that the Group sells. The performance of maintenance services is often accompanied with the sale of parts. Therefore, revenue from sale of parts is reported with the performance of after-sales services. Revenue from after-sales services is recognised over the period of performance of services to customers.

The sale of vehicle to the customer may be bundled together with extended warranties and/or free services. The extended warranty provides assurance to the customer that the vehicle parts comply with agreed-upon specifications beyond the general standard warranty period. The extended warranties and free services are separate performance obligations and the transaction price is allocated to the service obligations based on its relative standalone selling prices. The extended warranties and free services are deferred and recognised over the period covered by the extended warranties and when the free services are performed respectively.

There is no significant financing component in the sale of extended warranties and/or free services as the sales are made on normal credit terms not exceeding 12 months. Where consideration is collected from customers in advance of services being performed, a contract liability is recognised. The contract liability would be recognised as revenue when the related services are rendered.

(c) Assembly of vehicles

The Group manufactures and assembles light commercial and passenger vehicles, and are contract assemblers of motor vehicles. Revenue arising from the assembly of vehicles is either recognised upon completion of the assembly service or over the period when assembly services are rendered based on the contractual terms with the customers.

(d) Handling and commission income

Revenue arising from rendering services, handling income and commission income is recognised when the relevant services are completed.

iii. UMW

UMW division’s revenue consists primarily of sale of vehicles, equipment and parts and provision of after-sales services or related services. The revenue recognition policy for these transactions are as per the revenue recognition of similar transactions under the Industrial and Motors segments as set out in Notes 3(p)(i) and 3(p)(ii).

iv. Other revenue

Revenue from other sources are recognised as follows:

(a) dividend income is recognised when the right to receive payment is established; and

(b) rental income is generally recognised on a straight-line basis over the tenure of the lease.

k. Contract assets and liabilities

Contract asset is the right to consideration for goods or services transferred to the customers. In the case of engineering contracts, contract asset is the excess of cumulative revenue earned over the billings to-date. See Note 3(l)(iii) on impairment of contract assets.

Contract liability is the obligation to transfer goods or services to customers for which the Group has received the consideration or has billed the customer. In the case of engineering contracts, contract liability is the excess of the billings to-date over the cumulative revenue earned. Contract liabilities include downpayments received from customers and other deferred income where the Group has billed or has collected the payment before the goods are delivered or services are provided to the customers.

l. Impairment (extract)

iii. Impairment of financial assets and contract assets

The Group recognises an allowance for expected credit loss (“ECL”) for all debt instruments not held at fair value through profit or loss (“FVTPL”).

ECLs are measured based on a general 3-stage approach and a simplified approach.

General 3-stage approach for other receivables and amounts due from subsidiaries

ECLs are recognised in two stages. For credit exposures for which there has not been a significant increase in credit risk since initial recognition, ECLs are provided for credit losses that result from default events that are possible within the next 12 months (a 12-month ECL).

For those credit exposures for which there has been a significant increase in credit risk since initial recognition, a loss allowance is required for credit losses expected over the remaining life of the exposure, irrespective of the timing of the default (a lifetime ECL).

Simplified approach for trade receivables, contract assets and finance lease receivables

For trade receivables, contract assets and finance lease receivables, the Group applies a simplified approach in calculating ECLs. Therefore, the Group does not track changes in credit risk, but instead recognises a loss allowance based on lifetime ECLs at each reporting date.

Significant increase in credit risk

The Group considers the probability of default upon initial recognition of the asset and whether there has been a significant increase in credit risk on an ongoing basis throughout each reporting period. To assess whether there is a significant increase in credit risk, the Group compares the risk of a default occurring on the asset as at the reporting date with the risk of default as at the date of initial recognition.

The Group considers a receivable as credit impaired when one or more events that have a detrimental impact on the estimated cash flow have occurred. These instances include adverse changes in the financial capability of the debtor and default or significant delay in payments. However, in certain cases, the Group may also consider a financial asset to be in default when internal or external information indicates that the Group is unlikely to receive the outstanding contractual amounts in full before taking into account any credit enhancements held by the Group. A financial asset is written off to profit or loss when there is no reasonable expectation of recovering the contractual cash flows.

Grouping of instruments for ECL measured on collective basis

Collective assessment

To measure ECL, trade receivables and contract assets are grouped into categories. The categories are differentiated by the different business risks and are subject to different credit assessments. Contract assets relate to unbilled work in progress and have substantially the same risk characteristics as the trade receivables for the same types of contracts. The Group considers the expected loss rates for trade receivables as a reasonable approximation of the loss rates for contract assets with similar risk characteristics.

Individual assessment

Trade receivables, contract assets, other receivables and amounts due from subsidiaries which are in default or credit-impaired are assessed individually.

4 CRITICAL ACCOUNTING ESTIMATES AND JUDGEMENT IN APPLYING ACCOUNTING POLICIES (extract)

c. Revenue recognition on maintenance income, extended warranties and parts credit

Revenue from customers include revenue derived from bundled contracts. The Group employs significant judgement in identifying separate performance obligations within these contracts. The Group regards the maintenance income (which is inclusive of free services), extended warranties and parts credit as separate performance obligations as the customers are able to benefit from each of the performance obligations on its own and they are distinct from each other. Revenue is allocated to the service obligations based on its relative stand-alone selling prices upon a sale of equipment or vehicle. These maintenance income and extended warranties are deferred and recognised over the period covered in the contracts or upon rendering of the services. Revenue from parts credit is recognised upon utilisation of credit for exchange of parts. Management estimates the stand-alone selling prices of the maintenance income, extended warranties and parts credit based on observable prices of the type of services likely to be provided and the services rendered in similar circumstances to customers. Where the stand-alone selling price of distinct goods or services is not directly observable, they are estimated based on expected cost-plus margin.

e. Provision for warranties for vehicles

The Group recognises provision for liabilities associated with the warranties provided on vehicles. This requires an estimation of the expenditure required to settle the present obligation at the reporting date. In determining the provision, the Group has made assumptions in relation to the expected cost to repair and/or replace the products and the expected timing of those costs.

Provision is recognised on product warranty claims for vehicles where the Group has undertaken to repair or replace items that fail to comply satisfactorily with agreed-upon specifications. The provision was estimated based on expected warranty claims on products sold, based on past experience of the level of repairs and return claims as well as recent trend analysis which are indicative of future claims. The estimation involves assumptions regarding the timing and cost of repairs or replacements, utilising historical claims data and applying a discount rate to present value future warranty obligations. The carrying amount of provision for warranties on vehicles at the end of the reporting period is RM298 million.

NOTES TO THE FINANCIAL STATEMENTS (extracts)

FOR THE FINANCIAL YEAR ENDED 30 JUNE 2025

Amounts in RM million unless otherwise stated

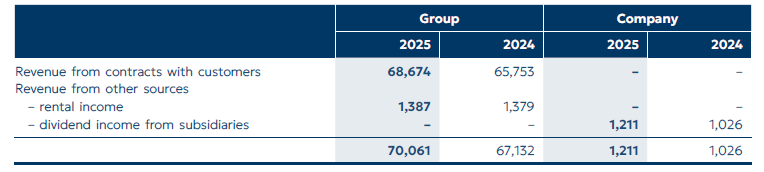

6 REVENUE

Revenue comprise the following:

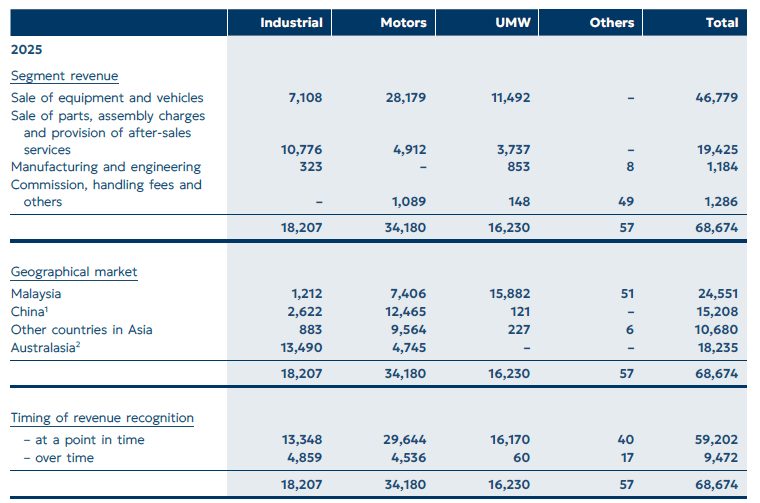

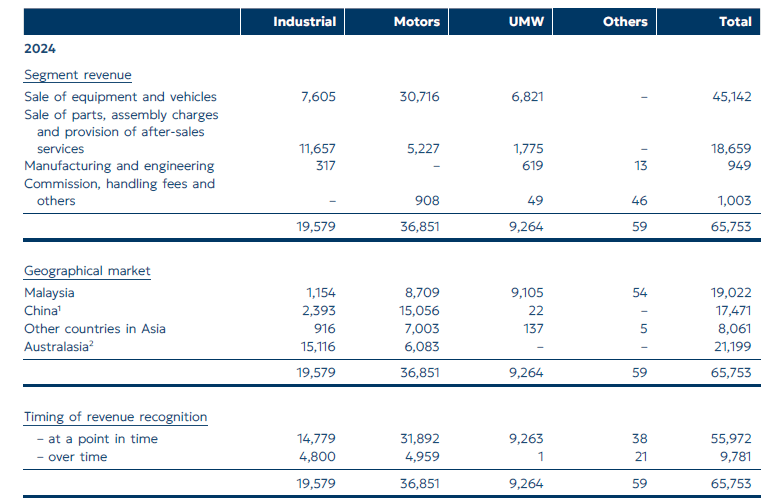

Analysis of the Group’s revenue from contracts with customers:

1 China consists of Mainland China, Hong Kong, Macau and Taiwan.

2 Australasia consists of Australia, New Caledonia, New Zealand, Papua New Guinea and the Solomon Islands.

1 China consists of Mainland China, Hong Kong, Macau and Taiwan.

2 Australasia consists of Australia, New Caledonia, New Zealand, Papua New Guinea and the Solomon Islands.

Revenue from contracts with customer of the Group includes RM2,049 million (2024: RM2,434 million) that was included in contract liabilities at the beginning of the reporting period.

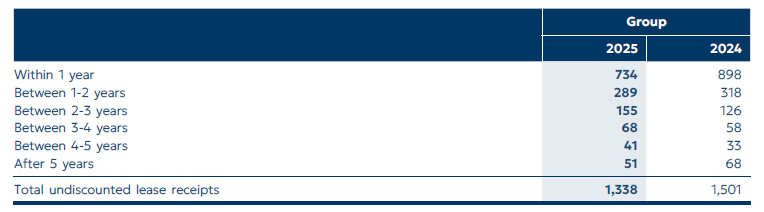

The Group generates rental revenue mainly from leasing of equipment and motor vehicles. It also receives rental income from the leasing of certain properties. The following table sets out the maturity analysis of lease receipts of the Group, showing the undiscounted lease payments to be received after the reporting date and includes operating lease income recognised as other operating income (Note 10):

Included in revenue is RM158 million (2024: RM146 million) arising from subleasing of right-of-use assets.

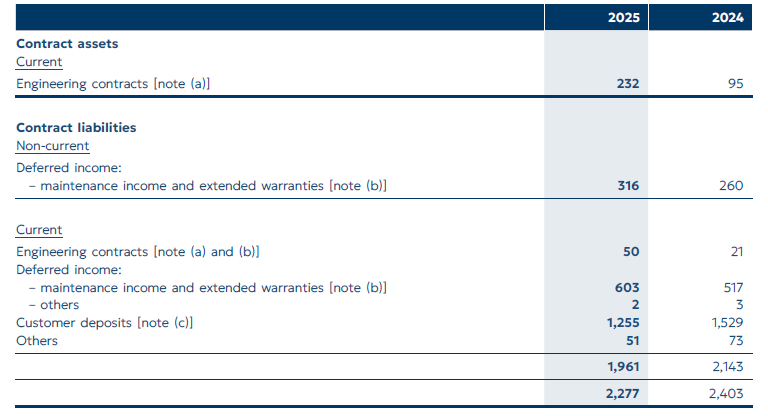

32 CONTRACT ASSETS AND LIABILITIES – GROUP

a. Engineering contracts

The engineering contracts represent timing differences between revenue recognition and the milestone billings. Milestone billings are structured and/or negotiated with customers to reflect physical completion of the contracts.

b. Contract value yet to be recognised as revenue

Revenue expected to be recognised in the future relating to performance obligations that are unsatisfied (or partially unsatisfied) at the reporting date, are as follows:

c. Customer deposits

Customer deposits relate to deposits made by customers for the purchase of equipment and vehicles which were partially delivered or have yet to be delivered by the Group at the reporting date. The Group applies the practical expedient in MFRS 15 “Revenue from Contracts with Customers” on not disclosing the aggregate amount of the revenue expected to be recognised in the future as the performance obligation is part of a contract that has an original expected duration of less than one year.