Mitie Group plc – Annual report – 31 March 2018

Industry: support services

- Basis of preparation and significant accounting policies (extract)

Early adoption of IFRS 15

The Group decided to early adopt IFRS 15 ‘Revenue from contracts with customers’, with a date of initial application of 1 April 2017. As a result, the Group has changed its accounting policies and updated its internal processes and controls relating to revenue recognition.

The Group has applied IFRS 15 using the cumulative effect method – i.e. by recognising the cumulative effect of initially applying IFRS 15 as an adjustment to the opening balance of equity at 1 April 2017, calculated only for those contracts that were not completed as at 1 April 2017. Therefore, the comparative information has not been restated and continues to be reported under IAS 18 ‘Revenue’ and IAS 11 ‘Construction contracts’.

IFRS 15 provides a single, principles based five-step model to be applied to all sales contracts as outlined below. It is based on the transfer of control of goods and services to customers and replaces the separate models for goods, services and construction contracts.

- Identify the contract(s) with a customer

- Identify the performance obligations in the contract

- Determine the transaction price

- Allocate the transaction price to the performance obligations in the contract

- Recognise revenue when or as the entity satisfies its performance obligations

Set out below is the revenue recognition policy under IFRS 15 and the five-step model together with the impact of adopting the standard.

Revenue recognition policy under IFRS 15

The Group operates contracts with a varying degree of complexity across its service lines so accordingly, a range of methods are used for the recognition of revenue based on the principles set out in IFRS 15. Revenue represents income recognised in respect of services provided during the period based on the delivery of performance obligations and an assessment of when control is transferred to the customer.

Step 1 – Identify the contract(s) with a customer

For all contracts with customers, the Group determines if the arrangement creates enforceable rights and obligations. This assessment results in certain Framework arrangements or Master Service Agreements (MSAs) not meeting the definition of a contract under IFRS 15 unless it specifies the minimum quantities to be ordered. Usually the work order and any change orders together with the Framework or MSA will constitute the IFRS 15 contract.

Duration of contract

The Group frequently enters into contracts with customers which contain extension periods at the end of the initial term, automatic annual renewals, and/or termination for convenience and break clauses that could impact the actual duration of the contract. As the term of the contract impacts the period over which amortisation of contract assets and revenue from performance obligations may be recognised, the Group applies judgement to assess the impact that such clauses have in determining the relevant contract term. In forming this judgement, management considers certain influencing factors including the amount of discount provided, the presence of significant termination penalties in the contract, and the relationship, experience and performance of contract delivery with the customer and/or the wider industry, in understanding the likelihood of extension or termination of the contract.

Contract modifications

The Group’s contracts are frequently amended for changes to customer requirements such as change orders and variations. A contract modification takes place when the amendment creates new enforceable rights and obligations or changes the existing price or scope (or both) of the contract, and the modification has been approved. Contract modifications can be approved in writing, by oral agreement, or implied by customary business practices.

If the parties to the contract have not approved a contract modification, revenue is recognised in accordance with the existing contractual terms. If a change in scope has been approved but the corresponding change in price is still being negotiated, the Group estimates the change to the total transaction price.

Contract modifications are accounted for as a separate contract if the contract scope changes due to the addition of distinct goods or services and the change in contract price reflects the standalone selling price of the distinct good or service. The facts and circumstances of any modification are considered in isolation as these are specific to each contract and may result in different accounting outcomes.

Step 2 – Identify the performance obligations in the contract

Performance obligations are the contractual promises by the Group to transfer distinct goods or services to a customer. For arrangements with multiple components to be delivered to customers such as in the Group’s integrated facilities management contracts, the Group applies judgement to consider whether those promised goods and services are:

i. Distinct and accounted for as separate performance obligations;

ii. Combined with other promised goods or services until a bundle is identified that is distinct; or

iii. Part of a series of distinct goods and services that are substantially the same and have the same pattern of transfer over time i.e. where the customer is deemed to have simultaneously received and consumed the benefits of the goods or services over the life of the contract, the Group treats the series as a single performance obligation.

Step 3 – Determine the transaction price

At contract inception, the total transaction price is determined, being the amount to which the Group expects to be entitled and has rights under the current contract. This includes the fixed price stated in the contract and an assessment of any variable consideration, up or down, resulting from e.g. discounts, rebates, service penalties. Variable consideration is typically estimated based on the expected value method and is only recognised to the extent it is highly probable that a subsequent change in its estimate would not result in a significant revenue reversal.

Step 4 – Allocate the transaction price to the performance obligations in the contract

The Group allocates the total transaction price to the identified performance obligations based on their relative stand-alone selling prices. This is predominantly based on an observable price or a cost plus margin arrangement.

Step 5 – Recognise revenue when or as the entity satisfies its performance obligations

For each performance obligation, the Group determines if revenue will be recognised over time or at a point in time. Where revenue is recognised over time, the Group applies the relevant output or input revenue recognition method for measuring progress that faithfully depicts the Group’s performance in transferring control of the goods and services to the customer.

Certain long-term contracts use output methods based upon surveys of performance completed, appraisals of results achieved, or milestones reached which allow the Group to recognise revenue on the basis of direct measurements of the value to the customer of the goods and services transferred to date relative to the remaining goods and services under the contract.

Under the input method, measured progress and revenue are recognised in direct proportion to costs incurred where the transfer of control is most closely aligned to the Group’s efforts in delivering the service.

Where deemed appropriate, the Group will utilise the practical expedient within IFRS15, allowing revenue to be recognised at the amount which the Group has the right to invoice, where that amount corresponds directly with the value to the customer of the Group’s performance completed to date.

If performance obligations do not meet the criteria to recognise revenue over time, revenue is recognised at the point in time when control of the good or service passes to the customer. This may be at the point of physical delivery of goods and acceptance by a customer or when the customer obtains control of an asset or service in a contract with customer-specified acceptance criteria.

Long-term complex contracts

The Group has a number of long-term complex contracts which are predominantly integrated facilities management arrangements. Typically, these contracts involve the provision of multiple service lines, with a single management team providing an integrated service. Such contracts tend to be transformational in nature where the business works with the client to identify and implement cost saving initiatives across the life of the contract.

The Group considers the majority of services provided within integrated facilities management contracts meet the definition of a series of distinct goods and services that are substantially the same and have the same pattern of transfer over time. The series constitutes services provided in distinct time increments (e.g. monthly or quarterly) and therefore the Group treats the series of such services as one performance obligation.

The Group also delivers major project-based services under long-term complex contracts that include performance obligations under which revenue is recognised over time as value from the service is transferred to the customer. This may be where the Group has a legally enforceable right to remuneration for the work completed to date, or at milestone periods, and therefore revenue will be recognised in line with the associated transfer of control or milestone dates.

Repeat service-based contracts (single and bundled contracts)

The Group operates a number of single or joint-service line arrangements where repeat services meet the definition of a series of distinct services that are substantially the same (e.g. the provision of cleaning, security, catering, waste, and landscaping services). They have the same pattern of transfer of value to the customer as the series constitutes core services provided in distinct time increments (e.g. monthly or quarterly). The Group therefore treats the series of such services as one performance obligation.

Short-term service-based arrangements

The Group delivers a range of other short-term service based performance obligations and professional services work across certain reporting segments for which revenue is recognised at the point in time when control of the service has transferred to the customer. This may be at the point when the customer obtains control of the service in a contract with customer-specified acceptance criteria e.g. the delivery of a strategic operating model or report.

Sales of goods are recognised when goods are delivered and control has passed to the customer.

Other revenue

Interest income is accrued on a time basis, by reference to the principal outstanding and at the effective interest rate applicable, which is the rate that exactly discounts estimated future cash receipts through the expected life of the financial asset to that asset’s net carrying amount.

Contract assets

Pre-contract costs

The Group incurs pre-contract expenses (e.g. legal costs) when it is expected to enter into a new contract. The incremental costs to obtain a contract with a customer are recognised within contract assets if it is expected that those costs will be recoverable. Costs to obtain a contract that would have been incurred regardless of whether the contract was obtained are recognised as an expense in the period.

Contract fulfilment costs

Costs incurred to ensure that the project or programme has appropriate organisational, operational and technical infrastructures, and mechanisms in place to enable the delivery of full services under the contract target operating model, are defined as contract fulfilment costs. Only costs which meet all three of the criteria below are included within contract assets on the balance sheet:

i. the costs directly relate to the contract (e.g. direct labour, materials, sub-contractors);

ii. the Group is building an asset that belongs to the customer that will subsequently be used to deliver contract outcomes; and

iii. the costs are expected to be recoverable i.e. the contract is expected to be profitable after amortising the capitalised costs.

Contract fulfilment costs covered within the scope of another accounting standard, such as inventories, intangible assets, or property, plant and equipment are not capitalised as contract fulfilment assets but are treated according to the other standard.

Amortisation and impairment of contract assets

The Group amortises contract assets (pre-contract costs and contract fulfilment costs) on a systematic basis that is consistent with the entity’s transfer of the related goods or services to the customer. The expense is recognised in profit or loss in the period.

A capitalised pre-contract cost or contract fulfilment cost is derecognised either when it is disposed of or when no further economic benefits are expected to flow from its use or disposal.

The Group is required to determine the recoverability of contract related assets at each reporting date. An impairment exists if the carrying amount of any asset exceeds the amount of consideration the entity expects to receive in exchange for providing the associated goods and services, less the remaining costs that relate directly to providing those goods and services under the relevant contract. In determining the estimated amount of consideration, the Group uses the same principles as it does to determine the contract transaction price which includes estimates around variable consideration. An impairment is recognised immediately where such losses are forecast.

Accrued income and deferred income

The Group’s customer contracts include a diverse range of payment schedules which are often agreed at the inception of long-term contracts under which it receives payments throughout the term of the arrangement. Payments for goods and services transferred at a point in time may be at the delivery date, in arrears or part payment in advance.

Where revenue recognised at the period end date is more than amounts invoiced, the Group records accrued income for the difference. Where revenue recognised at the period end date is less than amounts invoiced, the Group recognises deferred income for the difference.

Certain arrangements with customers include a contractual obligation to make redundancies for which the Group is reimbursed for the costs incurred. Revenue is not recognised on these transactions. Instead, the Group expenses all redundancy costs in the period they are incurred and any reimbursement credit is matched against the associated cost included in the income statement up to the value of the redundancy cost incurred. Any cash payments received from the customer in excess of the reimbursement cost of redundancy are deferred over the contract term and unwound in line with the other services being delivered.

Where price step-downs are required in a contract and output is not decreasing, revenue is deferred from initial years to subsequent years in order for revenue to be recognised on a consistent basis.

Providing the option for a customer to obtain extension periods or other services at a significant discount may lead to a separate performance obligation where a material right exists. Where this is the case, the Group allocates part of the transaction price from the original contract to deferred income which is then amortised over the discounted extension period or recognised immediately when the extension right expires.

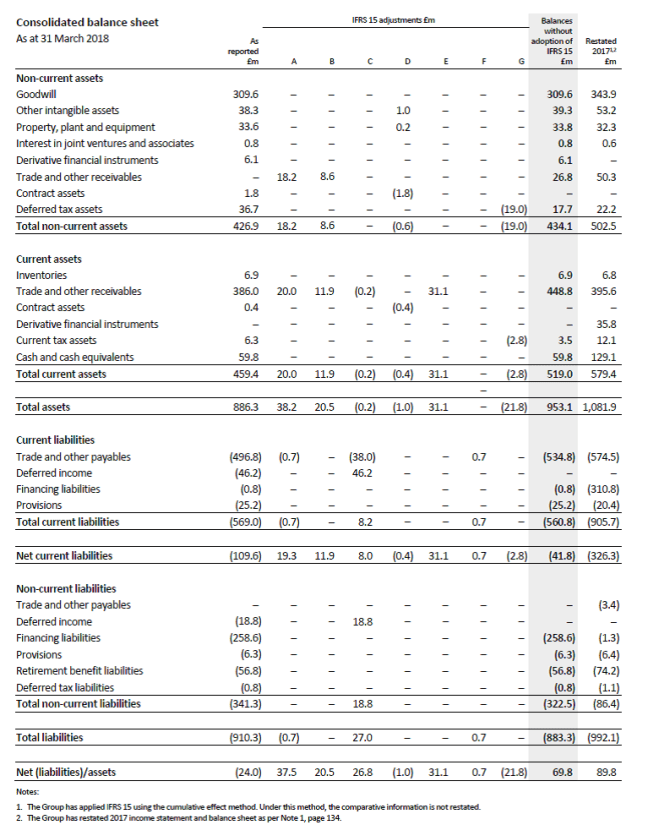

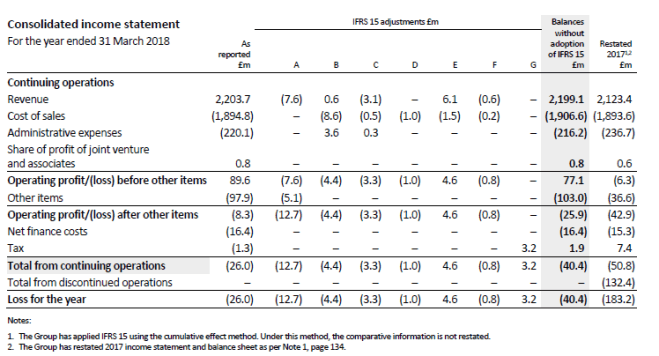

The following disclosures show the impact of the adoption of IFRS 15 on the Group’s primary financial statements.

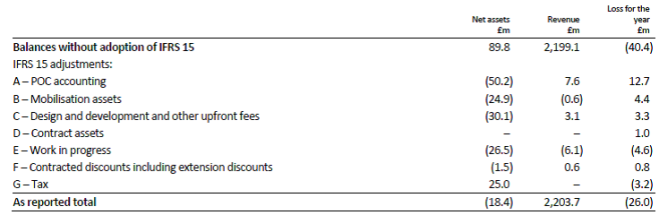

The following table details the impact on net assets as at 1 April 2017 and on the revenue and loss for the year recognised for the year ended 31 March 2018, as a result of the adoption of IFRS 15:

Adjustment A – POC accounting

IFRS 15 introduces the concept of performance obligations which are the contractual promises by an entity to transfer goods or services to a customer. Under IFRS 15, revenue is recognised on a contract specific basis and in line with the satisfaction of performance obligations. This is a change from the Group’s previous accounting policy and the use of a percentage of completion model to measure the proportion of contract costs incurred for work performed to date compared to the total estimated contract costs. Percentage of completion accounting does not provide an appropriate representation of the satisfaction of performance obligations on these long-term complex contracts and consequently, is no longer applied.

The impact of this is a decrease in reserves of £50.2m to derecognise the percentage of completion asset held as accrued income on long-term complex contracts at 1 April 2017 and a £12.7m credit to the loss for the year ended 31 March 2018 comprising £7.6m to reverse the unwind of the asset movement, and £5.1m to reverse a percentage of completion asset write-off included within other items. The reversal of the asset write-off follows the net impact of a write-off of £6.6m in relation to the loss of two contracts which was offset by a £1.5m credit to reinstate a previously written off asset. These balances, which were presented in Other Items, would not have been recognised under IFRS 15 as percentage of completion accounting would not have been applied.

Adjustment B – Mobilisation assets

IFRS 15 specifies that certain costs to fulfil a contract are to be capitalised as contract assets if relevant criteria are met. The Group has determined that the existing mobilisation asset, whilst appropriate under the previous accounting standard, does not meet the more stringent criteria under IFRS 15.

The Group has therefore derecognised the asset (including £3.9m recognised in prepayments within trade and other receivables) as at 1 April 2017 leading to a decrease in reserves of £24.9m.

The adjustment to the loss for the year ended 31 March 2018 is a credit of £4.4m to reverse additions and write back amortisation on the mobilisation balance written off.

Adjustment C – Design and development and other upfront fees

On certain contracts, the Group receives upfront, non-refundable payments from the customer to cover significant costs incurred by the Group during the initial phase of the contract. Under IFRS 15, costs incurred from these transition and mobilisation activities, which are more than administrative in nature, are assessed to determine whether they form a separate performance obligation. Where such costs do not form a separate performance obligation under the contract, any upfront payments received from the customer are allocated to the performance obligations of the contract, deferred and recognised over the life of the other services.

The Group has determined that £30.1m of revenue previously recognised should be presented as deferred income at 1 April 2017 leading to a decrease in reserves by the same amount. The adjustment to the loss for the year ended 31 March 2018 is a £3.3m credit following the rephasing of upfront payments.

Following the adoption of IFRS 15, the Group has presented deferred income from contracts with customers separately on the balance sheet. The balance of pre-IFRS 15 current deferred income amounting to £46.2m has been reclassified as a result.

Adjustment D – Contract assets

IFRS 15 specifies that certain costs to fulfil a contract are to be capitalised as contract assets if relevant criteria are met. The Group capitalised a balance of £1.2m during the year ended 31 March 2018 (comprising £1.0m and £0.2m that would otherwise have been recorded in other intangible assets and property, plant and equipment respectively) that related to resources to allow it to deliver services under its contracts for which control had passed to the customer on installation. This amount has been recognised on the balance sheet as an addition to contract assets under IFRS 15.

During the year ended 31 March 2018, the Group capitalised costs of £1.0m that were previously expensed and which relate to assets to be used to deliver future contract outcomes.

Adjustment E – Work in progress

Under IFRS 15, revenue is only recognised when control has passed to a customer and it can be reliably measured. Income which was previously recognised under IAS 11 and IAS 18 has been remeasured against the more stringent criteria in IFRS 15, resulting in an amount being derecognised where it cannot be reliably measured.

The Group has therefore derecognised the asset held on balance sheet within accrued income leading to a reduction in reserves of £26.5m at 1 April 2017. The impact to the loss for the year ended 31 March 2018 is a debit of £4.6m.

Adjustment F – Contracted discounts including extension discounts

Where a contract provides the option for a customer to obtain an extension period at a significant discount, this may lead to a separate performance obligation where a material right exists. If a separate performance obligation exists then there would be an allocation of the transaction price from the original contract through the option period. A balance is therefore adjusted in reserves and recognised in deferred income with the unwind recognised over the extension period (or immediately if the option expires).

The Group has recorded a reduction of £1.5m in reserves at 1 April 2017 to reflect the material right with the balance recognised in deferred income, which will be unwound as future services are delivered. The impact to the loss for the year ended 31 March 2018 is a credit of £0.8m.

Adjustment G – Tax

Due to the changes in the pattern and timing of revenue recognition under IFRS 15, an additional deferred income liability is recognised on the balance sheet from 1 April 2017, via a charge to the opening balance of equity at 1 April 2017. Further, certain assets previously held in accrued income and recognised through the income statement in earlier periods have been derecognised from 1 April 2017, again via a charge to the opening balance of equity at 1 April 2017.

A tax deduction is available at 1 April 2017 for the one-off transitional adjustments recognised in opening equity. This tax deduction gives rise to tax losses at 1 April 2017, creating a deductible temporary difference for which a deferred tax asset of £25.0m is recognised at 1 April 2017, leading to an increase in reserves by the same amount. The tax impact of the IFRS 15 adjustments on the loss for the year ended 31 March 2018 is a charge of £3.2m, of which £1.0m arises on the adjustment to other items.

- Critical accounting judgements and key sources of estimation uncertainty (extract)

The preparation of consolidated financial statements under IFRS requires management to make judgements, estimates and assumptions that affect amounts recognised for assets and liabilities at the reporting date and the amounts of revenue and expenses incurred during the reporting period. Actual results may differ from these judgements, estimates and assumptions.

The judgements and estimates which have the most significant effect on the reported result for the period and upon the carrying value of assets and liabilities of the Group as at 31 March 2018 are described below.

Revenue recognition

The Group’s revenue recognition policies, which are set out under IFRS 15 in Note 1(a) for the financial year ended 31 March 2018 and under IAS 18 and IAS 11 in Note 1(b) in respect of prior years, are central to how the Group measures the work it has performed in each financial year.

The Group’s current policy under IFRS 15

Due to the size and complexity of the Group’s contracts, management is required to form a number of key judgements and assumptions in the determination of the amount of revenue and profits to record, and related balance sheet items such as contract assets, accrued income and deferred income to recognise (refer to Note 1(a)). This includes an assessment of the costs the Group incurs to deliver the contractual commitments and whether such costs should be expensed as incurred or capitalised.

In addition, for certain contracts, key assumptions are made:

i. concerning contract extensions and amendments which, for example, directly impact the phasing of upfront payments from customers which are recognised in deferred income and unwound over the expected contract term; or

ii. where options are granted to customers leading to the recognition of a material right.

These judgements are inherently subjective and may cover future events such as the achievement of contractual performance targets and planned cost savings or discounts.

The Group’s prior year policy under IAS 18 and IAS 11

The revenue recognised for certain long-term complex project-based services was based on the stage of completion of the contract activity. This was measured by comparing the proportion of costs incurred, which include transition costs reflecting costs incurred in the performance of transitioning services, against the estimated whole-life contract costs. This required significant judgements to be made in forecasting the outcomes of the long-term contracts.

Particular judgement was required in evaluating the operational and financial business plans for these contracts to forecast the expected whole-life contract billings, costs and margin and to assess the recoverability of any resulting accrued income through the life of the contract. In forming the judgement around expected whole-life contract billings, account was taken of potential deductions from and increments to revenue arising from the application of performance related measures under contracts.

This required management to apply judgements and estimates that drew on the knowledge and experience of the Group’s project managers and delivery teams together with the Group’s commercial and finance professionals. Whilst there may have been a broad range of possible outcomes based on the relevant circumstances of the individual contract, the Group had controls in place whereby all significant contracts were reviewed on a monthly basis and reforecast quarterly.

The amounts recognised as revenue, profit and contract assets were sensitive to changes in assumptions, for example:

- Revenue measurement – in line with the Group’s revenue recognition policy for long-term complex contracts, revenue was recognised on these contracts to the extent that the outcome of the project could be reliably measured. For long-term complex contracts this required judgements to be made on which elements of the contract could be accurately forecast. These contracts would usually comprise fixed revenue streams, variable works and project works. Project works were not included as part of a long-term complex contract on the basis that these amounts were discretionary and consequently could not be reliably forecast. Therefore, these projects were accounted for separately. The revenue streams that could be reliably forecast comprised the fixed elements (for example for ongoing cleaning and security services) and variable works.

- Contract profitability and costs to complete – long-term complex contracts are transformational in nature and there is a commitment to work in partnership with the client from the outset of the contract to drive significant cost savings and efficiencies throughout the life of the contract. During the mobilisation of a contract a target operating model is developed. This target operating model shows how the services that are part of the contract will be delivered during the contract and is subject to a continuous review/improvement process throughout the duration of the contract. The target operating model, cost saving initiatives identified and revenue pipeline were combined into a financial plan for the individual contract. Only cost saving initiatives that were considered to be reasonably certain in terms of timing and scale were included in the plan. Management’s ability to accurately forecast the costs to complete the contract involved judgements around cost savings to be achieved over time, anticipated profitability of the contract, as well as contract specific performance KPIs. Where a contract was anticipated to make a loss, these judgements were also relevant in determining whether or not an onerous contract provision was required and how this was to be measured.

- Renegotiation of terms – the Group often entered into renegotiations of existing contract terms such as the timing or the specifications of the services to be delivered. Depending on the outcome of such negotiations, the timing and amount of revenue recognised may have been different.

- Recoverability of contract related assets – linked to the profitability of contracts above, management was also required to determine the recoverability of contract related assets, accrued income and accounts receivable. Judgement was required in determining whether or not the future economic benefits from contracts were sufficient to recover these contract assets.