Equinor ASA – Annual report – 31 December 2025

Industry: oil and gas

Accounting judgement and key sources of estimation uncertainty

The preparation of the Consolidated financial statements requires management to make accounting judgements, estimates and assumptions.

Information about judgements made in applying the accounting policies that have the most significant effects on the amounts recognised in the Consolidated financial statements is described in the following notes:

Note 6 – Acquisitions and disposals

Note 7 – Total revenues and other income

Note 15 – Joint arrangements and associates

Note 25 – Leases

Estimates used in the preparation of these Consolidated financial statements are prepared based on customised models. The assumptions applied in these estimates are derived from historical experience, external sources of information and various other factors that management assesses to be reasonable under the current conditions and circumstances. These estimates and assumptions form the basis of making the judgements about carrying values of assets and liabilities when these are not readily apparent from other sources. Actual results may differ from these estimates. The estimates and underlying assumptions are continuously reviewed, taking into account the current and expected future set of conditions.

Equinor is exposed to several underlying economic factors affecting the overall results, such as commodity prices, foreign currency exchange rates, market risk premiums and interest rates as well as financial instruments with fair values derived from changes in these factors. The effects of the initiatives to limit climate changes and the transition to a lower carbon economy are relevant to several of these economic assumptions. In addition, Equinor’s results are influenced by the level of production, which in the short term may be impacted by, for instance, maintenance programmes, among other factors. In the long-term, the results are impacted by the success of exploration, field developments, operating activities, and progress within renewables and low carbon solutions.

The most important matters in understanding the key sources of estimation uncertainty are described in each of the following notes:

Note 3 – Climate change and energy transition

Note 11 – Income taxes

Note 12 – Property, plant and equipment

Note 13 – Intangible assets

Note 14 – Impairments

Note 23 – Provisions and other liabilities

Note 26 – Other commitments, contingent liabilities and contingent assets

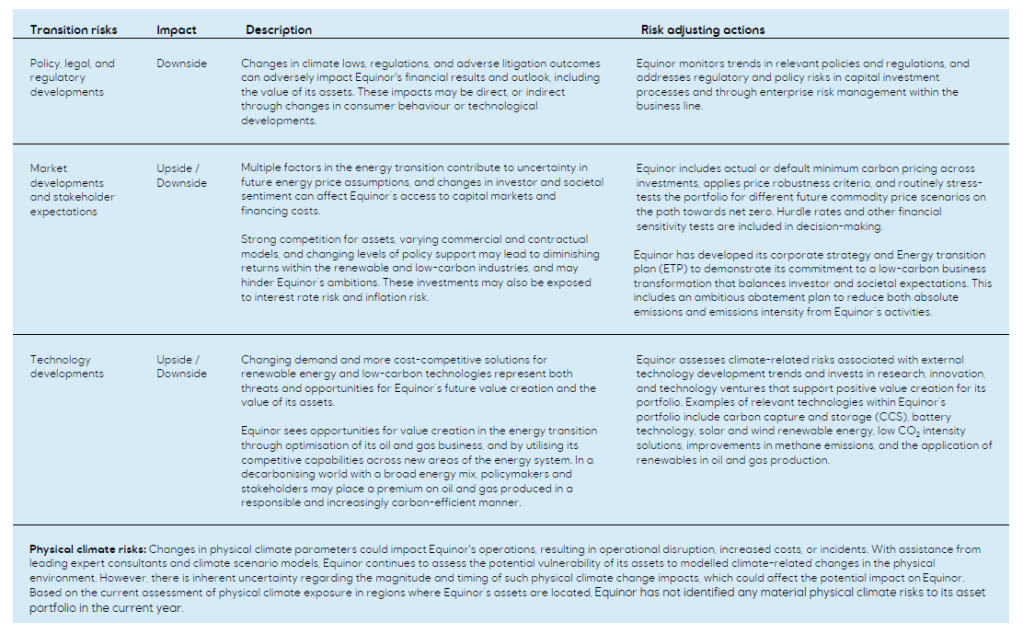

Note 3. Climate change and energy transition

Risks arising from climate change and the transition to a lower carbon economy

Developments in laws and regulations, policies, technology, and markets—including stakeholder sentiment towards climate change—can affect Equinor’s financial performance and business plans. In parallel, shifts in stakeholder focus between energy security, energy affordability, and sustainability present challenges for the energy sector.

Equinor’s risk assessment and management process incorporates short-, medium- and long-term perspectives. Climate-related risks are classified as either transition risks, which relate to the financial robustness of the company’s business model and portfolio under various decarbonisation scenarios, or physical climate risks, which relate to the exposure and potential vulnerability of Equinor’s assets to climate-related hazards.

Equinor’s double materiality assessment for 2025 identified transition risks as a material sustainability matter. The table to the right summarises the relevant climate-related risks with potential financial effects.

Equinor’s Energy transition plan and climate-related ambitions are responses to the challenges and opportunities presented by climate change and the energy transition.

Impact on Equinor’s financial statements

In preparing the 2025 financial statements, Equinor has conducted a range of sensitivity analyses and other assessments in relation to climate-related matters, as outlined in this note to the financial statements. The following information provides further detail on the specific climate-related risks and sensitivities considered, and how these have been evaluated in the context of our financial reporting. Based on these assessments, no climate-related effects have been identified that would have a significant impact on the 2025 financial statements.

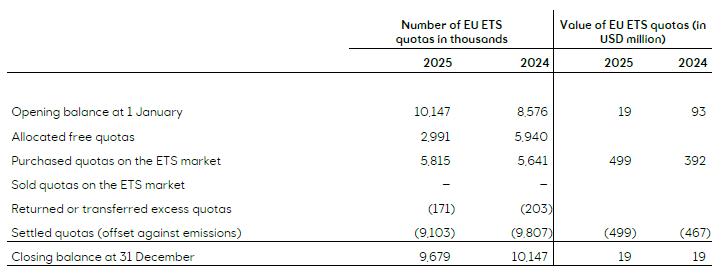

CO₂-cost and EU ETS carbon credits

Equinor’s oil and gas operations in Europe are part of the EU Emissions Trading System (EU ETS). Currently, Equinor receives a share of free quotas according to EU ETS regulations. This share of free quotas is expected to be significantly reduced in the future. Equinor purchases additional EU ETS allowances (quotas or carbon credits) when its oil and gas production and processing emissions exceed its free EU ETS quota allocation.

Total expensed CO₂ costs attributable to Equinor’s share of operated licences and land-based facilities amounted to USD 478 million in 2025, USD 465 million in 2024, and USD 486 million in 2023.

The table below presents the number and associated value of EU ETS and UK ETS quotas that have been received, purchased, and utilised by Equinor on an operated basis. Allocated free quotas consists of actual free quotas received under the ETS during the calendar year. In 2024, Equinor received allocated free quotas for both 2024 and 2023, due to a delay in the allocation schedule. The year-end quota balance consists mainly of free and purchased quotas remaining after the settlement of quotas against current and prior year emissions. The closing balance in USD consists of the value of the remaining quotas after a preliminary settlement allocation for the current year.

Numbers in the table are presented gross (100%) for Equinor operated licences and include EU ETS and UK ETS quotas, as received or settled during the calendar year.

Accounting policies

Cost of CO₂ quotas

Purchased CO₂ quotas under the EU Emissions Trading System (EU ETS) are reflected at cost in Operating expenses as incurred in line with emissions. Accruals for CO₂ quotas required to cover emissions to date are valued at market price and reflected as current liabilities within Trade and other payables. Quotas owned, but exceeding the emissions incurred to date, are carried in the balance sheet at cost price, classified as Other current receivables, as long as such purchased quotas are acquired in order to cover own emissions and may be kept to cover subsequent years’ emissions.

Obligations resulting from current year emissions and the corresponding amounts for quotas that have been bought, paid, and expensed, but which have not yet been surrendered to the relevant authorities, are reflected net in the balance sheet.

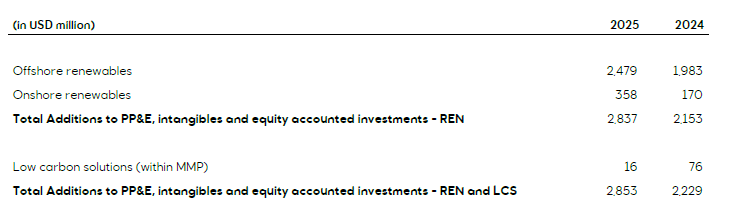

Investments in renewables and low-carbon solutions

Equinor’s ambition is to build a focused, carbon efficient oil and gas portfolio complemented by an integrated power portfolio and commercial opportunities in low carbon solutions. This diversified approach aims to maintain long-term value creation while supplying reliable energy, with progressively lower emissions, to our customers.

Equinor’s investments in renewables are included as Additions to PP&E, intangibles and equity accounted investments in the REN segment (refer to note 5 Segments). During 2025, the REN segment invested USD 2.1 billion in the Empire Wind project, USD 195 million to acquire the onshore Lyngsåsa wind farm in Sweden, and USD 258 million as contributions to equity accounted investments in Bałtyk 2 & 3.

Additions to PP&E, intangibles and equity accounted investments exclude changes to ARO, in alignment with note 5 Segments.

Equinor continues to take steps to industrialise carbon capture and storage (CCS). During 2025, the Northern Lights project received its first CO2 for storage, and a final investment decision was made to commence the project’s second phase. In addition, Equinor is developing the Net Zero Teesside and Northern Endurance Partnership projects to provide thermal power with applied CCS to local industries in the UK. Equinor contributed USD 16 million to equity accounted investments undertaking CCS projects in 2025 (USD 76 million in 2024).

Investments in electrification of oil and gas assets

During 2025, Equinor invested USD 168 million in electrification (USD 180 million in 2024). Equinor’s abatement projects primarily include full and partial electrification of offshore assets in Norway at key fields and plants, including Troll, Oseberg, Njord, and the Hammerfest LNG plant, mainly by power from shore.

Research and development activities (R&D)

Equinor is involved in several projects aimed at optimising oil and gas activities, reducing emissions, and developing new business opportunities in renewable energy generation and low carbon solutions. Equinor’s R&D expenditure is disclosed in note 9 Auditor’s remuneration and Research and development expenditures. The accounting policy for R&D is detailed in note 12 Property, plant and equipment.

Power Purchase Agreements (PPAs)

Equinor holds various long-term PPAs for power sourced from wind and solar parks, with expiry dates up until 2040. The agreements imply balancing activities, whereby Equinor assumes the long-term balancing risk related to production. The majority of these agreements are settled at the appropriate market price, less a balancing fee, and expire by the end of 2027. The agreements include pay-as-produced elements; however, as most of the power purchase agreements are linked to the applicable market prices, and the power purchased is mainly sold on power exchanges at market price, Equinor only holds a limited long-term price risk related to these agreements. For accounting policies related to power sales and related purchases, refer to note 7 Total revenues and other income.

Effects on estimation uncertainty

Initiatives to limit climate change, as well as the potential impact of the energy transition, are relevant to certain economic assumptions and future cash flow estimates used by Equinor. The resulting effects, and Equinor’s exposure to them, are sources of uncertainty. Estimating global energy demand and commodity prices towards 2050 is challenging due to various complex factors, including technological capabilities, regulatory policies, taxation, and production limits, all of which evolve over time. These uncertainties could result in significant changes to accounting estimates over time. Relevant accounting estimates include depreciation and asset retirement obligations (useful life of assets), impairment assessments, and deferred tax assets (see note 11 Income taxes for the expected utilisation period of tax losses carried forward and recognised as deferred tax assets).

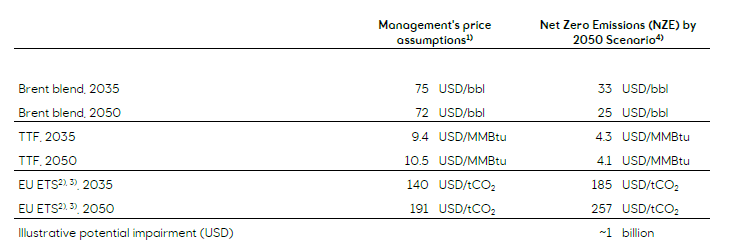

Commodity prices

Significant changes in oil and gas prices outside planning assumptions could impact our financial performance. Equinor’s commodity price assumptions, applied in its value-in-use calculations, are based on management’s best estimate of future market trends.

These price assumptions deviate from the price set out to achieve net zero emissions by 2050 and limit global warming to 1.5 °C, in alignment with the Paris Agreement and as outlined in the International Energy Agency’s World Energy Outlook (IEA’s WEO) Net Zero Emissions (NZE) Scenario.

Changes in how the world acts with regards to achieving the goals of the Paris Agreement could have a negative impact on the valuation of Equinor’s assets. An illustrative impairment effect to Equinor’s upstream production assets and certain intangible assets, using published price assumptions from the NZE Scenario, is provided in the Sensitivity table sub-section.

When computing this illustrative impairment, management’s price assumptions are applied until 2035. A linear interpolation is applied between the published NZE Scenario prices (2035-2050), after which prices are maintained at the 2050 level. This approach is consistent with prior year, where management’s price assumptions were applied until the first published price point in the relevant IEA’s WEO scenario (in 2024, this was 2030) before a linear interpolation was performed. To be comparable to Equinor’s management’s price assumptions, the crude oil prices in the NZE Scenario are adjusted for transportation costs, and all prices are adjusted for inflation and presented in real 2025 terms. The illustrative impairment sensitivity calculation is based on a simplified model with limitations, as described in note 14 Impairments.

Cost of CO2

Climate-related considerations are included in the impairment assessments through CO₂ tax estimations in the forecasted cash flows, and indirectly through estimated commodity prices relating to supply and demand. The CO₂ prices also influence the estimated production profiles and economic cut-off of the assets.

Carbon price assumptions are applied to all Equinor assets, including assets in countries outside the EU where CO2 is not already subject to taxation or where Equinor has not established specific estimates. Our default assumption, in real 2025 terms, is a price of USD 100 per tonne starting in 2027, increasing to USD 122 per tonne by 2030 and remaining flat thereafter.

The EU ETS price has increased over time and had an average cost of 74 EUR/tonne in 2025 (66 EUR/tonne in 2024). Equinor’s commodity price assumptions include an EU ETS price of 81 EUR/tonne for the next two years and assumes an increase to EU ETS prices over time. See note 14. Impairments for management’s forecasted EU ETS price assumptions for the years 2030, 2040, and 2050.

Equinor expects greenhouse gas emission costs to increase from current levels and to have a wider geographical range than today. Equinor recognizes CO₂-related costs in Norway, the UK and Germany for its own operated assets, as well as in Canada for partner-operated assets.

The CO₂ tax assumptions used in the impairment assessments of Norwegian upstream assets are based on Norway’s Climate Action Plan for the period 2021-2030 (Meld. St 13 (2020-2021)), assuming a gradual increase to the CO₂-related cost in Norway to 2,000 NOK/tonne (real 2020) in 2030 (the total of EU ETS + Norwegian CO₂).

Sensitivity table

The table below compares management’s price assumptions to the NZE Scenario price set and presents an illustrative impairment amount from applying the NZE Scenario prices to Equinor’s portfolio. Refer to section 3.2 E1 Climate change in the 2025 Annual Report for more details about the scenarios presented in the IEA’s WEO 2025.

An increase in systemic climate risk may result in higher discount rates used in impairment calculations. Refer to note 14 Impairments for general sensitivity analysis on discount rates and commodity prices.

1) Management’s future commodity price assumptions applied when estimating value in use, see note 14 Impairments for additional years disclosed.

2) Scenario: Price of CO₂ quotas in advanced economies with net zero pledges, not including any other CO₂ taxes.

3) Management’s EU ETS price assumptions have been translated from EUR to USD using Equinor’s assumptions for currency rates, EUR/USD = 1.15

4) An IEA WEO scenario where the world follows a potential path towards limiting global warming to 1.5 °C relative to pre-industrial levels. Values are adjusted for inflation and presented in 2025 real terms.

The illustrative potential impairment from applying the NZE Scenario price set, excludes MMP’s trading and refinery activities, as well as Equinor’s renewable assets and low-carbon projects. This is because the IEA’s WEO scenarios primarily stress oil and gas prices, with limited consideration of the potential impact these prices have on trading and refinery margins. For most MMP assets, margin movements are not directly correlated to oil and gas price fluctuations, and for many of Equinor’s renewable assets, prices are fixed in offtake contracts and therefore not directly sensitive to power prices. Furthermore, the MMP and REN segments represent around 15% of Equinor’s total non-current segment assets and equity accounted investments, as disclosed in note 5 Segments. Based on this, these assets would not have a material effect on the illustrative potential impairment calculation, if included.

Robustness of Equinor’s portfolio and risk of stranded assets

The transition to renewable energy, technological development, and the expected reduction in global demand for carbon-based energy may impact the future profitability of certain upstream oil and gas assets. Equinor uses scenario analysis to outline different possible energy futures, some of which imply lower oil and natural gas prices and higher CO₂ costs. If this materialises, it could lead to a decrease in cash flow from oil and gas, and potentially reduce the economic useful life of certain assets. Equinor seeks to mitigate this risk by improving the resilience of its existing upstream portfolio, maximising the efficiency of its infrastructure on the Norwegian Continental Shelf (NCS), and optimising its international portfolio. Equinor’s project portfolio is expected to remain robust to low oil and gas prices, and actions are in place to maintain cost discipline across the company. Equinor continues to pursue high-value barrels to enhance its portfolio through exploration and increased recovery, in addition to acquisitions and divestments, with the expectation of strong oil and gas cash flow from operations. Equinor aims to maintain capex flexibility in its current portfolio, with non-sanctioned projects representing a substantial part of the expected capex, particularly for 2027 and beyond. This approach enables capex optimisation and reprioritisation in future periods, ensuring sustained, long-term value generation.

Based on the current production profiles, approximately 78% of Equinor’s proved oil and gas reserves, as defined by the SEC, are planned to be produced in the period 2026-2035, and more than 99% in the period 2026-2050. In addition, approximately 69% of Equinor’s expected oil and gas reserves are planned to be produced in the period 2026-2035, and around 96% in the period 2026-2050. Both instances imply a low exposure of Equinor’s reserves value to early cessation, particularly after 2035, and provide flexibility in adapting to changing market conditions or a shift in global energy demand. Refer to note 12 Property, plant and equipment for the definition of proved and expected oil and gas reserves.

Continued exploration for hydrocarbons is important for maintaining long-term energy deliveries. Equinor will continue to supply oil and gas beyond 2035 but anticipate that it will form an increasingly smaller proportion of its portfolio over time. Achieving Equinor’s 2030 net 50% reduction ambition for operated scope 1 and 2 emissions will require a company-wide, co-ordinated effort to improve energy efficiency and to execute and mature abatement projects. Equinor aims to achieve a 5-15% reduction in net carbon intensity by 2030 and a 15-30% reduction by 2035, including scope 1, 2 and 3 emissions (category 11 & 15). Equinor’s climate-related ambitions have not resulted in impairment triggers for 2025.

Future exploration may be restricted by policies, regulations, market conditions, and strategic considerations that have not yet occurred. Should the economic assumptions deteriorate to such an extent that undeveloped assets controlled by Equinor do not materialise, the assets at risk would mainly comprise intangible assets: oil and gas prospects, signature bonuses, and capitalised exploration costs. The total carrying value is USD 3.8 billion in 2025, of which USD 1.5 billion is in E&P Norway and USD 2.3 billion is in E&P International (USD 3.6 billion in 2024, with USD 1.1 billion in E&P Norway and USD 2.5 billion in E&P International). See note 13 Intangible assets for further information regarding Equinor’s intangible assets.

Timing of Asset Retirement Obligations (ARO)

No assets to date have ceased operations early as a result of Equinor’s climate-related ambitions. However, should the business case for Equinor’s producing oil and gas assets change materially, this could affect the timing of asset retirement. A shorter production timeline would increase the carrying value of the ARO liability. Undertaking removal five years earlier than currently scheduled would increase the liability by approximately USD 1.5 billion before tax and excluding assets held for sale (approximately USD 1.1 billion in 2024), which is mainly related to E&P Norway. See note 23 Provisions and other liabilities for more information regarding Equinor’s ARO, including discount rate sensitivity and the expected timing of cash outflows for recognised ARO.

Note 14. Impairments

Accounting policies

Impairment of property, plant and equipment, right-of-use assets, intangible assets including goodwill and equity accounted investments

Equinor assesses individual assets or groups of assets for impairment when events or changes in circumstances indicate that the carrying value may not be recoverable. Assets are grouped into cash generating units (CGUs), typically individual oil and gas fields, plants, or equity accounted investments. Each unconventional asset play is considered a single CGU when no cash inflows from parts of the play can be readily identified as being largely independent of the cash inflows from other parts of the play. In impairment assessments, the carrying amounts of CGUs are determined on a basis consistent with that of the recoverable amount.

Properties that are not yet classified as reserves are assessed for impairment when facts and circumstances suggest that the carrying amount of the asset or CGU to which the unproved properties belong may exceed its recoverable amount, and at least once a year. Exploratory wells that have found hydrocarbon resources, but where classification of those resources as reserves depends on whether major capital expenditure can be justified or where the economic viability of that major capital expenditure depends on the successful completion of further exploration work, will remain capitalised during the evaluation phase for the exploratory finds. If, following evaluation, an exploratory well has not found hydrocarbon resources, the previously capitalised costs are tested for impairment. After the initial evaluation phase for a well, it will be considered a trigger for impairment testing of a well if no development decision is planned for the near future and there is no firm plan for future drilling in the licence.

Goodwill is reviewed for impairment annually or more frequently if events or changes in circumstances indicate that the carrying value might be impaired. Impairment is determined by assessing the recoverable amount of the CGU, or group of units, to which the goodwill relates. When conducting impairment testing of goodwill initially recognised as an offsetting item to the computed deferred tax provision in a post-tax transaction on the NCS, the remaining amount of the deferred tax provision will factor into the impairment valuation.

Impairment and reversals of impairment are presented in the Consolidated statement of income as either Exploration expenses or Depreciation, amortisation and net impairment losses. This classification depends on the nature of the impaired assets, whether they are as exploration assets (intangible exploration assets) or development and producing assets (property, plant and equipment and other intangible assets), respectively.

Measurement

The recoverable amount applied in Equinor’s impairment assessments is normally estimated value in use. Equinor may also apply the assets’ fair value less cost of disposal as the recoverable amount when such a value is available, reasonably reliable, and based on a recent and comparable transactions.

Value in use is determined using a discounted cash flow model. The estimated future cash flows are based on Equinor’s most recently approved forecasts by management, which are based on reasonable and supportable assumptions and represent management’s best estimates of the range of economic conditions that will exist over the remaining useful life of the assets. Assumptions and economic conditions in establishing the forecasts are reviewed by management on a regular basis and updated at least annually. For assets and CGUs with an expected useful life or timeline for production of expected oil and natural gas reserves extending beyond five years, including planned onshore production from shale assets with a long development and production horizon, the forecasts reflect expected production volumes, and the related cash flows include project or asset specific estimates reflecting the relevant period. Such estimates are established based on Equinor’s principles and assumptions and are consistently applied.

The estimated future cash flows are adjusted for risks specific to the asset or CGU and discounted using a real post-tax discount rate based on Equinor’s post-tax weighted average cost of capital (WACC). Country risk specific to a project is included as a monetary adjustment to the projects’ cashflow. Equinor considers country risk primarily as an unsystematic risk. The cash flow is adjusted for risk that influences the expected cash flow of a project and which is not part of the project itself. The use of post-tax discount rates in determining value in use does not result in a materially different determination of the need for, or the amount of, impairment that would be required if pre-tax discount rates had been used.

Impairment reversals

A previously recognised impairment is reversed only if there has been a change in the estimates used to determine the asset’s recoverable amount. Impairments of goodwill are not reversed in future periods.

Estimation uncertainty regarding impairment

Evaluating whether an asset is impaired or if an impairment should be reversed requires a high degree of judgement and may largely depend on the selection of key assumptions about future conditions. In Equinor’s business context, judgement is necessary in determining what constitutes a CGU. Development in production, infrastructure solutions, markets, product pricing, management actions and other factors may over time lead to changes in CGUs such as splitting one original CGU into multiple CGUs.

The key assumptions used are subject to change due to the inherently volatile nature of macro- economic factors such as future commodity prices and discount rates, as well as uncertainty in asset specific factors like reserve estimates and operational decisions impacting the production profile or activity levels. Fluctuations in foreign currency exchange rates will also affect value in use, especially for assets on the NCS, where the functional currency is NOK. When estimating the recoverable amount, the expected cash flow approach is applied to reflect uncertainties in timing and amounts inherent in the assumptions used in the estimated future cash flows. For example, climate-related matters (see also Note 3 Climate change and energy transition) are expected to have a pervasive impact on the energy industry, affecting not only supply, demand and commodity prices, but also technology changes, increased emission-related levies, and other matters with mainly mid-term and long-term effects. These effects have been factored into the price assumptions used for estimating future cash flows through probability-weighted scenario analyses.

Estimating future cash flows involves complexity, as it requires considering assumptions from Equinor’s, market participants’ and other external sources’ assumptions about the future and discounting them to present value. In order to establish relevant future cash flows, impairment testing requires long-term assumptions to be made concerning a number of economic factors such as future market prices, refinery margins, foreign currency exchange rates, future output, discount rates, impact of the timing of tax incentive regulations, and political and country risk among others. These long-term assumptions for major economic factors are made at a group level, and involve a high degree of reasoned judgement. This judgement is also required, in determining other relevant factors such as forward price curves, in estimating production outputs, and in determining the ultimate terminal value of an asset.

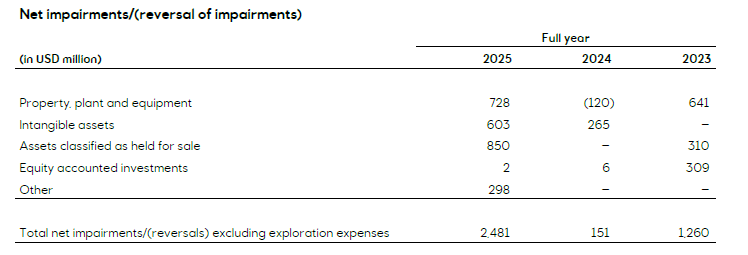

The intangible assets line includes Goodwill and amortisable intangible assets. Impairments classified as Exploration expenses in the Consolidated statement of income are excluded.

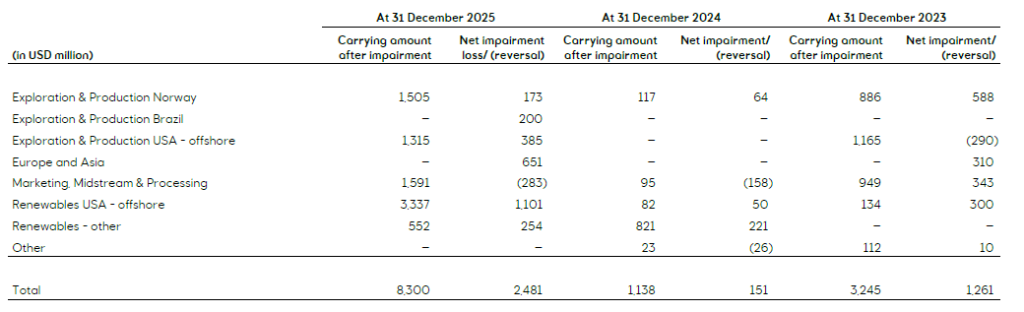

For impairment purposes, the asset’s carrying amount is compared to its recoverable amount. The recoverable amount is established based on a value in use approach unless otherwise stated below the table. The table below describes, per area, the Producing and development assets being impaired/(reversed), net impairment/(reversal), and the carrying amount after impairment.

Exploration & Production Norway

In 2023, the impairment mainly related to reduced expected reserves on a producing asset on the Norwegian Continental Shelf.

Exploration & Production USA – offshore

In 2025, the impairments related to producing assets in the Gulf of America following reduced production estimates, increased cost estimates and lower price assumptions. In 2023, the impairment reversal mainly related to increased expected reserves on a producing asset.

Exploration & Production International – Europe and Asia

In 2025 the impairment related to assets in the UK classified as held for sale and measured at fair value, due to an update of expected future commodity price assumptions. See note 6 Acquisitions and disposal. In 2023, the impairment related to the held for sale reclassification of Azerbaijan assets.

Marketing, Midstream & Processing

In 2025, the net impairment reversal mainly related to increased refinery margin assumptions combined with extended economic lifetime of the relevant asset. In 2023, the impairment mainly related to expectations of stabilizing refinery margins at a lower level than the margins consumed in recent periods.

Renewables USA – Offshore

In 2025, impairments mainly related to Equinor’s offshore wind projects on the US North East Coast. Regulatory changes leading to reduced expected synergies from future offshore wind projects and increased exposure to tariffs impacted the project economics for the combined cash generating unit encompassing Empire Wind 1 (EW1) and South Brooklyn Marine Terminal (SBMT) negatively, as well as the undeveloped Empire Wind 2 project. A discount rate of 3% real post-tax was applied.

There is an increased risk associated with offshore wind projects in the U.S., including the development of the Empire Wind project. The Bureau of Ocean Energy Management issued a second stop work order on 22 December 2025 (the Order), ordering the suspension of ongoing activities on the Outer Continental Shelf citing national security concerns. Empire Offshore Wind LLC has filed a lawsuit challenging the validity of the Order. Furthermore, on 15 January 2026, the U.S. District Court for the District of Columbia granted a preliminary injunction allowing construction to resume while the underlying case is considered. The injunction enables work to continue without significant delays or adverse financial consequences for the project. The case is still ongoing. On 31 December 2025, the gross book value of Equinor’s assets related to the Empire Wind project was around USD 3.7 billion, including SBMT. In addition, the total amount drawn under the project finance term loan facility per 31 December 2025 was USD 2.7 billion.

In 2023, Equinor’s offshore wind projects on the US North East Coast were facing increased costs and in October 2023, the New York State Public Service Commission (PSC) rejected price increase petitions related to the offtake agreement with Equinor’s equity accounted joint ventures. As a consequence, an impairment of USD 300 million was recognised applying a fair value approach.

Accounting assumptions

Management’s future commodity price assumptions and currency assumptions are used for value in use impairment testing. While there are inherent uncertainties in the assumptions, the commodity price assumptions as well as currency assumptions reflect management’s best estimate of the price and currency development over the life of the Group’s assets based on its view of relevant current circumstances and the likely future development of such circumstances, including energy demand development, energy and climate change policies, as well as the speed of the energy transition population and economic growth, geopolitical risks, technology, and cost development among other factors. Management’s best estimate also takes into consideration a range of external forecasts.

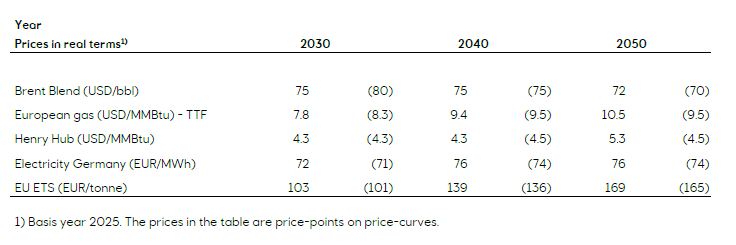

Equinor has performed a thorough and broad analysis of the expected development in drivers for the different commodity markets and exchange rates. Significant uncertainty exists regarding future commodity price development due to the transition to a lower carbon economy, future supply actions by OPEC+, and other factors. Such analysis resulted in changes in the long- term price assumptions with effect from the third quarter of 2025. The main price assumptions applied in impairment and impairment reversal assessments are disclosed in the table below as price-points on price curves. Previous price-points applied from the second quarter of 2024 and up to and including the second quarter of 2025 are provided in brackets.

The long-term NOK currency exchange rates are expected to remain unchanged compared to previous long-term assumptions. The NOK/USD rate from 2028 and onwards is kept at 10.0, the NOK/EUR rate at 11.5, and the USD/GBP rate at 1.30.

Climate considerations are included in the impairment calculations directly by estimating the CO₂ taxes in the cash flows. Indirectly, the expected effect of climate change is also included in the estimated commodity prices where supply and demand are considered. The prices also have an effect on the estimated production profiles and economic cut-off of the projects. Furthermore, climate considerations are a part of the investment decisions following Equinor’s strategy and commitments to the energy transition.

The CO₂-tax assumptions used for impairment calculations of Norwegian upstream assets are based on Norway’s Climate Action Plan for the period 2021-2030 (Meld. St 13 (2020-2021)), assuming a gradually increased CO₂ tax (the total of EU ETS + Norwegian CO₂ tax) in Norway to 2,000 NOK/tonne (real 2025) in 2030.

We apply carbon price assumptions for all Equinor’s assets, also for assets in countries outside EU where CO2 is not already subject to taxation or where Equinor has not established specific estimates.

The base discount rate applied in value in use calculations is 5.5% real after tax. The discount rate is derived from Equinor’s weighted average cost of capital. For projects, mainly within the REN segment in periods with fixed low risk income, a lower discount rate will be considered on a case-by-case basis. A pre-tax discount rate is derived based on the asset’s characteristics, such as specific tax treatments, cash flow profiles, and economic life. The pre-tax rates for 2025 were 6% for E&P USA, 4% for Renewables USA – Offshore and 7% for MMP.

Sensitivities

Significant downward adjustments in Equinor’s commodity price assumptions would result in impairment losses on certain producing and development assets, including intangible assets subject to impairment assessment, while an opposite adjustment could lead to impairment-reversals. Assuming a reasonably possible 30% decline in commodity price forecasts over the assets’ lifetime could result in an illustrative impairment recognition of approximately USD 6 billion before tax effects. See note 3 Climate change and energy transition for possible effect of using the prices in a 1.5ºC compatible Net Zero Emission by 2050 scenario.

Similarly, for illustrative purposes, Equinor assessed the sensitivity of the discount rate used in the value in use calculations for upstream producing assets and certain related intangible assets. An increase in the discount rate from 5.5% to 6.5% real after tax, in isolation, would have no material impact on the recognised impairment amount before tax effects.

The illustrative impairment sensitivities above are based on a simplified method, which assumes no changes to other input factors. However, Equinor notes that a price reduction of 30% or those representing Net Zero Emission scenario would likely impact business plans and other factors used in estimating an asset’s recoverable amount. The correlated changes reduce the stand-alone impact of the price sensitivities. Changes in such input factors would likely include a reduction in the cost level in the oil and gas industry and offsetting foreign currency effects, which have historically occurred following significant changes in commodity prices.