Drax plc – Annual report – 31 December 2024

Industry: utilities

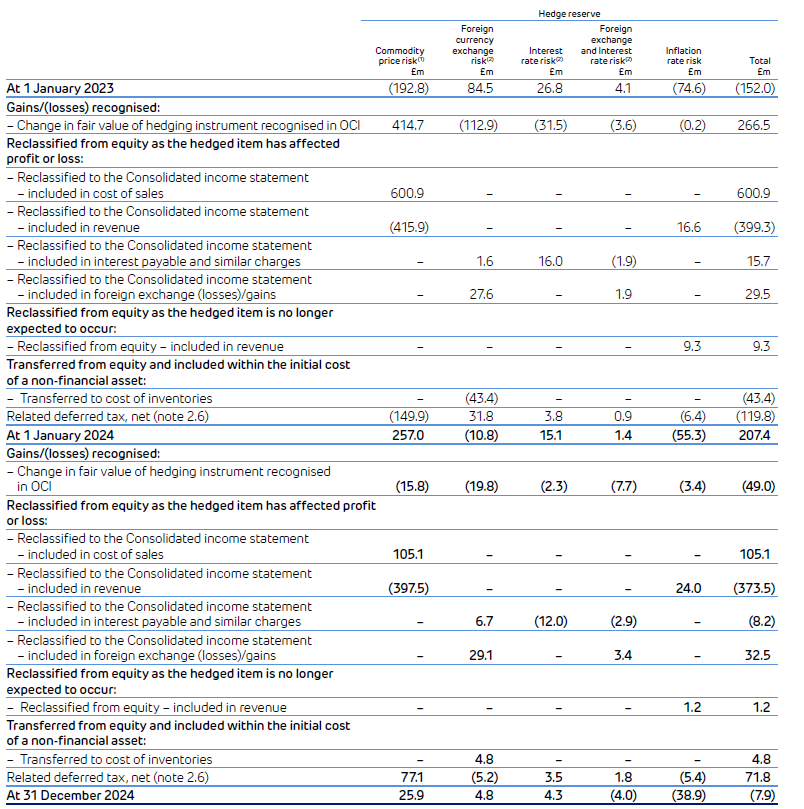

7.3 Hedge reserve (extract)

The Group designates certain hedging instruments that are used to address commodity price risk, foreign exchange risk, interest rate risk and inflation rate risk as cash flow hedges. At the inception of the hedge, the relationship between the hedging instrument and hedged item is documented, along with its risk management objectives. Furthermore, at the inception of the hedge and on an ongoing basis, the Group documents whether the hedging instruments used in hedging transactions are effective in offsetting changes in cash flows of the hedged items. Changes in the fair value of contracts designated into such hedging relationships are recognised within the hedge reserve to the extent they are effective. Amounts accumulated in the hedge reserve are reclassified in the periods when the hedged item affects profit or loss. If the hedged item results in the recognition of a non-financial asset then the amount accumulated in the hedge reserve is transferred and included within the initial cost of the asset.

The table below details the gains and losses recognised in the current and prior year on hedging instruments, the amounts reclassified from equity due to the hedged item affecting the Consolidated income statement, and the amounts reclassified due to the hedged future cash flows no longer being expected to occur. See section 7.2 for further details on these amounts.

(1) The table above has been re-presented to split the prior year reclassified amounts in commodity price risk column between amounts included in revenue and amounts included within cost of sales.

(2) The above table has been re-presented to include a foreign exchange and interest rate risk column. The amounts included within foreign exchange and interest rate risk relate to the Group’s floating-to-fixed cross-currency interest rate swaps that were previously disclosed partially within foreign currency exchange risk and partially within interest rate risk.

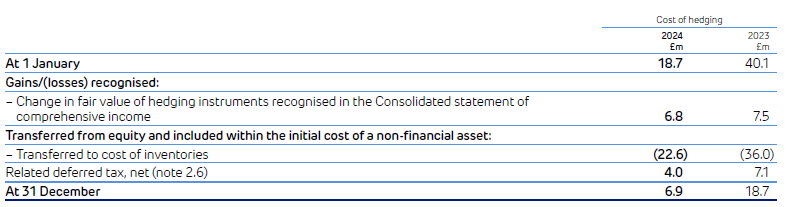

7.4 Cost of hedging reserve

Where the Group has designated the spot foreign exchange risk as the hedged risk, the Group allocates unrealised gains and losses on the forward rate of hedge accounted foreign currency derivative contracts to a cost of hedging reserve in accordance with IFRS 9.

A large proportion of the derivative contracts held relate to foreign currency exchange contracts, including forward contracts, options and swaps. Consistent with prior periods, for foreign currency exchange contracts hedging the purchase of inventory denominated in foreign currencies to which the Group has applied hedge accounting, the Group has continued to designate the change in the spot rate as the hedged risk in the Group’s cash flow hedge relationships. The Group designates the cost of hedging – being the change in fair value associated with forward points including currency basis – to equity. All amounts within the cost of hedging reserve relate to foreign currency exchange risk.

The table below details the cost of hedging gains or losses recognised in the year on hedging instruments and the amounts transferred from equity and included within the initial cost of a non-financial asset:

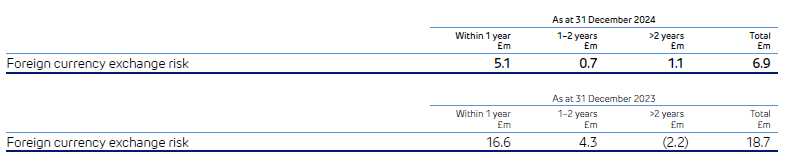

The expected release profile from equity of post-tax cost of hedging gains and losses is as follows:

7.2 Financial risk management (extract)

Foreign currency risk hedge accounting (extract)

The Group designates certain foreign currency exchange contracts, predominantly forwards, as hedging instruments of the foreign currency risk of biomass purchases denominated in foreign currencies. Gains and losses on these foreign currency exchange contracts are transferred from equity to inventories for these hedges when the Group takes ownership of the biomass. The Group designates the spot element of these foreign currency exchange contracts and applies a hedge ratio of 1:1.