Stora Enso Oyj – Annual report – 31 December 2025

Industry: agriculture

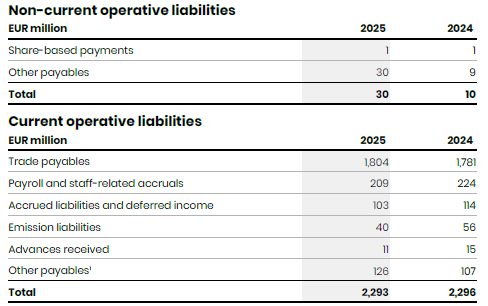

4.8 Operative liabilities (extract)

1 Other payables consist especially of taxes payable to government, such as VAT and payroll taxes.

In 2024, EUR 16 million of grants were paid back to the authorities in Belgium, as a result of a 2019 legionella related incident being considered as an environmental infringement.

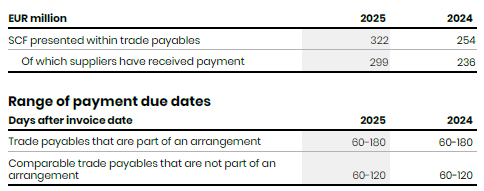

Supplier Chain Finance arrangements

Stora Enso has entered into several supply chain finance agreements. Supply chain finance arrangements are recognised as trade payables and are not reclassified after initial recognition.

Supply chain finance arrangements have the following terms and conditions:

Suppliers offered chance to join the programme, either as part of contract negotiations or during the contract period to update the terms the agreement. This is a trade payable programme where invoices are paid to the bank under the same payment terms that Stora Enso has agreed upon with the supplier, while the bank pays the supplier early for the invoice according to the arrangement. The bank conducts negotiations for the supplier’s participation in the programme, with Stora Enso acting as an agent to connect the two parties. The only cost to the supplier is the early payment of invoices. The programme is funded on a non-recourse basis by the funder, and the supplier predominantly bears the cost of the discounting in the programme. No joint and several liability clause is included in the programme, with all invoices treated the same in Stora Enso’s subsidiaries.

There were no material non-cash changes that would have caused changes in the carrying amounts.

5.1 Financial risk management (extract)

Liquidity and refinancing risk (extract)

As disclosed in note 4.8, the Group has entered into several supply finance agreements to improve the Group’s working capital. The finance providers are in good financial condition and the Group has no significant concentration of liquidity risk with the finance providers. The Group’s supplier finance agreements are discussed in more detail in note 4.8