AstraZeneca PLC – Annual report – 31 December 2025

Industry: pharmaceuticals

Applicable accounting standards and interpretations issued but not yet adopted (extract)

At the date of authorisation of these Financial Statements, certain new accounting standards and amendments were in issue relating to the following standards and interpretations but not yet adopted by the Group:

- IFRS 18 ‘Presentation and Disclosure in Financial Statements’ is effective for accounting periods beginning on or after 1 January 2027 and will replace IAS 1 ‘Presentation of Financial Statements’. IFRS 18 sets out new presentation requirements for the Statement of Comprehensive Income, as well as more stringent and additional requirements on the aggregation, disaggregation and categorisation of income and expenses within the Statement of Comprehensive Income. Additionally, alternative performance measures included within the Annual Report which meet the definition of Management-defined Performance Measures are required to be disclosed within the Notes to the Financial Statements. IFRS 18 was endorsed by the UKEB on 10 December 2025.

- The Group continues to advance with the implementation of IFRS 18 and is well progressed with the adoption impact assessment. The Group is not seeking to early adopt this new standard. However, as a means of illustrating the impact of IFRS 18 on the presentation of the Group’s results for the year ended 31 December 2025, the currently expected IFRS 18 adoption impacts for 2025 are shown in Note 1 to the Financial Statements. The Group continues to monitor IFRS 18 implementation guidance in advance of adoption for the accounting year beginning 1 January 2027.

1 IFRS 18 ‘Presentation and Disclosure in Financial Statements’

IFRS 18 ‘Presentation and Disclosure in Financial Statements’ is effective for accounting periods beginning on or after 1 January 2027 and will replace IAS 1 ‘Presentation of Financial Statements’. There are also consequential amendments to IAS 7 ‘Cash Flows’, IAS 8 ‘Accounting Policies, Changes in Accounting Estimates and Errors’, IAS 33 ‘Earnings per Share’ and IAS 34 ‘Interim Financial Reporting’, also effective for accounting periods beginning on or after 1 January 2027. The Group is well progressed with the impact assessment of the adoption of this new standard, with the expected impact for the year ended 31 December 2025 detailed below.

The Group will apply IFRS 18 retrospectively, in accordance with IAS 8. The Group has not elected to utilise the option to change the measurement of eligible investments in associates and joint ventures from the equity method to fair value through profit or loss at the date of transition.

The new standard introduces new requirements for the presentation, classification and disclosure of financial statement line items. The requirements were introduced to help achieve comparability of the financial performance of similar entities and provide more relevant information and transparency to users. The key changes include the requirement to classify all income and expense into one of five categories; operating, investing, financing, taxation and discontinued operations, and introduces new mandated subtotals within the Consolidated Statement of Comprehensive Income, including Operating profit, Profit before financing and income tax and Profit for the period. In addition, details of management-defined performance measures (‘MPMs’) will now be disclosed as well as further detailed disclosure related to operating expense by nature. The new standard also offers enhanced guidance on aggregation and disaggregation of financial information.

Although the adoption of IFRS 18 will have no impact on the Group’s Profit for the period or Total Revenue, the Group expects that grouping items of income and expense in the Consolidated Statement of Profit or Loss into the new categories will impact how Operating profit is reported.

The Group does not have a specified main business activity as defined in IFRS 18.

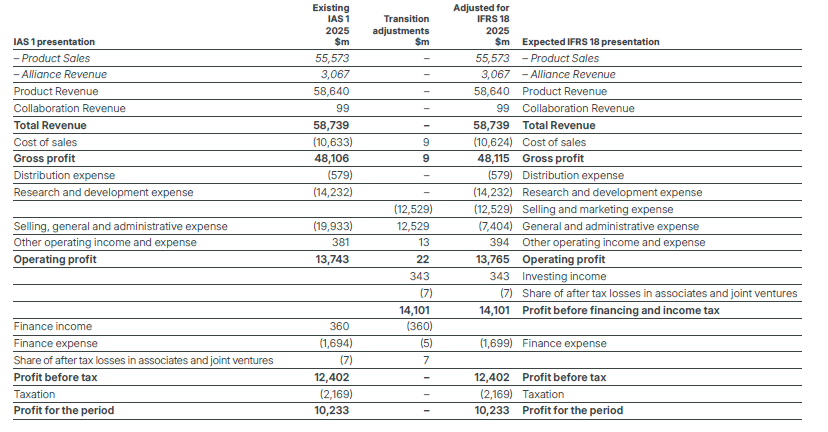

Reconciliation of the Consolidated Statement of Profit or Loss – Illustrative under IFRS 18 for the year ended 31 December 2025

Explanation of the adjustments due to IFRS 18

Share of after tax losses in associates and joint ventures will be presented within the investing category of the Consolidated Statement of Comprehensive Income, within the new subtotal of Profit or loss before financing and income tax which totals an expected $14,101m in 2025.

Returns on deposits and equity securities, and interest income on tax balances, previously reported within Finance income will be reclassified under IFRS 18 to Investing income, totalling an expected $360m in 2025.

Foreign exchange differences on cash and short-term deposits, previously included within Finance income and Finance expense, will be classified within the investing category under IFRS 18, expected to result in a reduction to Finance expense and a decrease in Investing income of $17m in 2025.

Gains and losses on certain designated hedges, previously included within Finance income and Finance expense, will be classified within the operating category under IFRS 18, resulting in an expected reduction to Finance expense and an increase in Other operating income and expense of $13m in 2025.

Under IFRS 18, Selling, general and administrative expense ($19,933m in 2025) will be disaggregated into Selling and marketing expense ($12,529m in 2025) and General and administrative expense ($7,404m in 2025).

Consolidated Statement of Cash Flows

The Consolidated Statement of Cash Flows under the amended IAS 7 requirements will start with Operating profit ($13,765m for 2025 under IFRS 18), rather than the previous starting point of Profit before tax ($12,402m in 2025 under IAS 1), removing the need to add back Finance income and expense ($1,334m in 2025) and Share of after tax losses of associates and joint ventures ($7m in 2025). In addition, Interest paid ($1,316m in 2025) will be reclassified to Cash flows from financing activities under IFRS 18, previously classified within Cash flows from operating activities.

Operating expenses by nature

The Group currently presents expenses in the Consolidated Statement of Comprehensive Income by function. While IFRS 18 continues to permit this presentation, it introduces additional disclosure requirements in the Notes to the Financial Statements. The following table presents 2025 operating expenses split by nature according to the requirements of IFRS 18.

The amounts disclosed are those expensed during the year, except for depreciation and employee benefits which include amounts capitalised to inventory and software development costs.

Management-defined performance measures (MPMs)

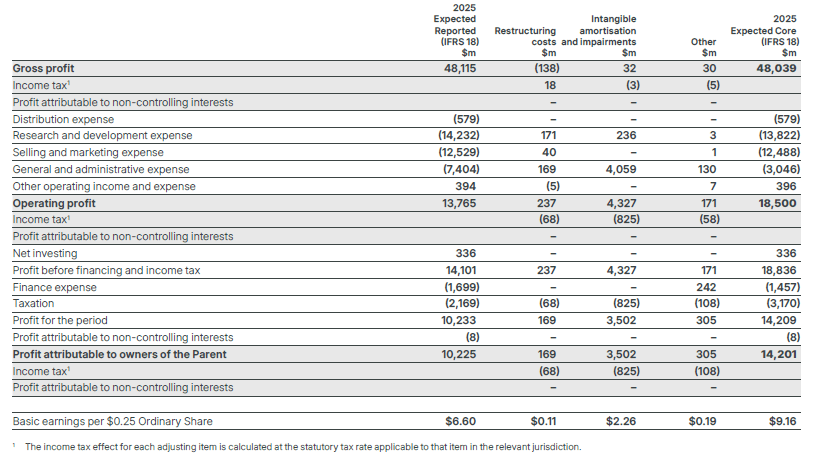

The Group has identified Core Gross profit ($48,039m in 2025 under IFRS 18), Core Operating profit ($18,500m in 2025 under IFRS 18) and Core Profit attributable to owners of the Parent (numerator of core basic earnings per share, $14,201m in 2025 under IFRS 18) as MPMs used in its public communications to communicate management’s view of an aspect of the operating performance of the Group as a whole. These measures are not specifically required to be presented or disclosed by IFRS, which means they may not be directly comparable with similarly labelled or described measures by other entities.

The reported IFRS results are adjusted to exclude certain significant items. In determining the adjustments to arrive at the Core result, we use a set of established principles relating to the nature or materiality of individual items or groups of items, excluding, for example, events which are (i) outside the normal course of business, (ii) incurred in a pattern that is unrelated to the trends in the underlying financial performance of our ongoing business, or (iii) related to major acquisitions, to ensure that investors’ ability to evaluate and analyse the underlying financial performance of our ongoing business is enhanced. Group management believes that these adjusted measures offer a relevant alternative perspective on the Group’s underlying operating performance by excluding the effects of the above mentioned items that are not indicative of the ongoing business activities. Group management considers this useful for understanding profitability trends and for evaluating the Group’s ability to generate sustainable earnings from its core operations.

Our Core adjustments are summarised as:

Restructuring costs, including charges and provisions related to our global restructuring programmes on our capitalised manufacturing facilities and IT assets. These can take place over multiple reporting periods, given the long life-cycle of our business.

Why we use them: We adjust for these charges and provisions because they primarily reflect the financial impact of change to legacy arrangements, rather than the underlying performance of our ongoing business.

Intangible amortisation and impairments, including impairment reversals but excluding any charges relating to IT assets. Intangibles generally arise from business combinations and individual licence acquisitions.

Why we use them: We adjust for these charges because their pattern of recognition is largely uncorrelated with the underlying performance of the business.

Other specified items, principally comprise acquisition-related costs and credits, which include the imputed finance charges and fair value movements relating to contingent consideration on business combinations, imputed finance charges and remeasurement adjustments on certain Other payables arising from intangible asset acquisitions, remeasurement adjustments relating to Other payables and debt items assumed from the Alexion acquisition and legal settlements.

Why we use them: We adjust for these items to enable a more meaningful comparison of the performance of acquired businesses and products to that of internally developed products, as well as removing charges whose pattern of recognition is largely uncorrelated to the underlying performance of the business. It should be noted that some costs excluded from our Core results, such as intangible amortisation and finance charges related to contingent consideration, will recur in future years, and other excluded items such as impairments and legal settlement costs, along with other acquisition-related costs, may recur in the future.

Limitations: Core results exclude significant costs (such as restructuring, intangible amortisation and impairments, and other acquisition-related adjustments), but incorporate associated benefits, including Product Sales arising from business combinations, asset acquisitions and assets which have been amortised, as well as the benefits resulting from restructuring activities and, as such, they should not be regarded as a complete picture of the Group’s financial performance, which is presented in its Reported results. The exclusion of the adjusting items may result in Core earnings being materially higher or lower than Reported earnings.

2025 Reconciliation of Expected Reported (IFRS 18) results to Expected Core (IFRS 18) results