Rolls-Royce Holdings plc – Annual report – 31 December 2025

Industry: manufacturing

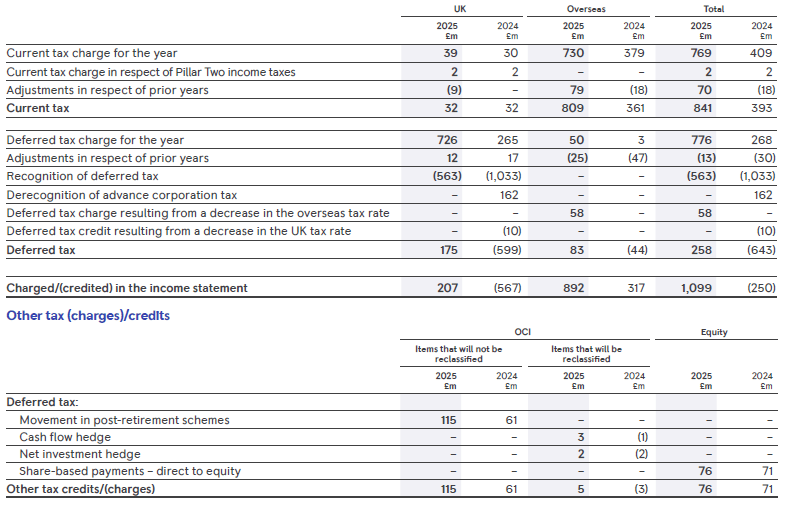

5 Taxation (extract 1)

5 Taxation (extract 2)

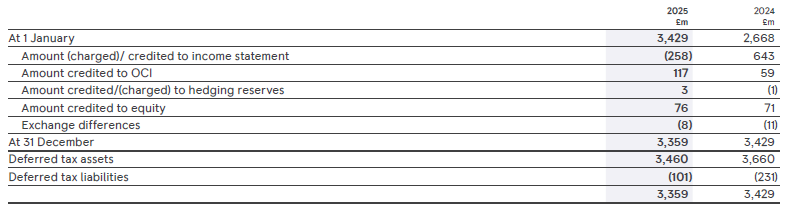

Deferred taxation assets and liabilities

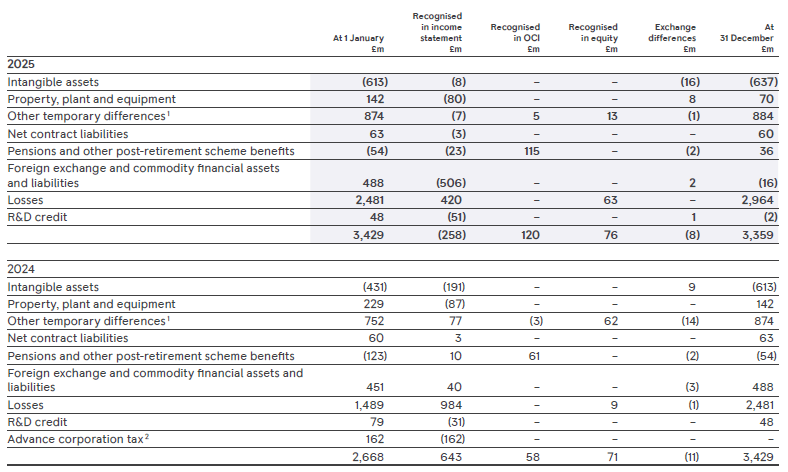

The analysis of the deferred tax position is as follows:

1 Other temporary differences mainly relate to the deferral of relief for interest expenses and share based payments in the UK and revenue recognised earlier under local GAAP compared to IFRS in Germany. The amount recognised in the income statement includes a £1m credit (2024: £8m credit) relating to share-based payments

2 Prior to 1999 advance corporation tax (“ACT”) was paid to the UK Tax Authority when cash dividends were paid by the Group. This was a payment on account which was available to offset against UK corporation tax liabilities. Any unused balance remaining after 1999 can be carried forward indefinitely and utilised against future UK corporation tax liabilities. See page 144 for further details