Co-operative Group Limited – Annual report – 4 January 2025

Industry: retail, financial

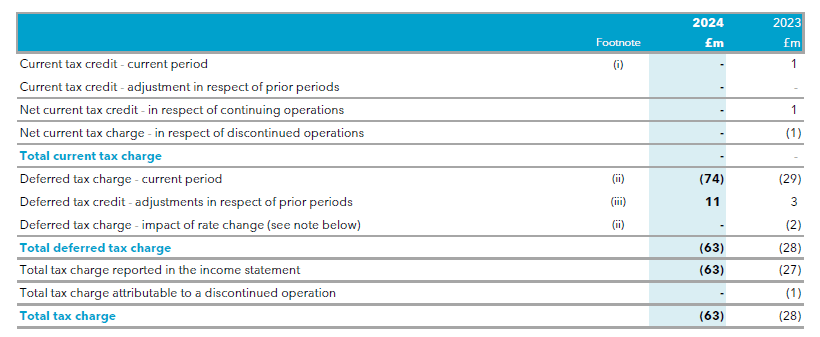

8 Taxation

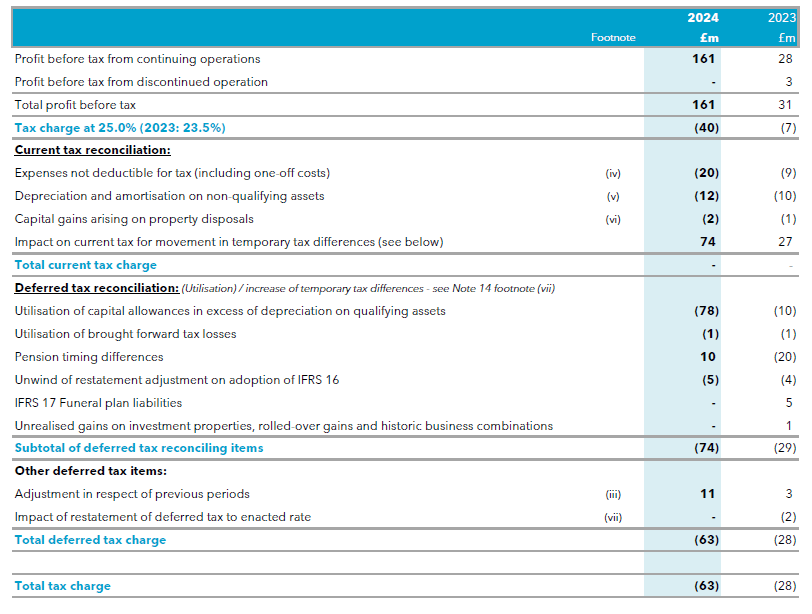

The tax on the Group’s net profit before tax differs from the theoretical amount that would arise using the standard applicable rate of corporation tax of 25.0% (2023: 23.5%) as follows:

Tax expense on items taken directly to consolidated statement of comprehensive income:

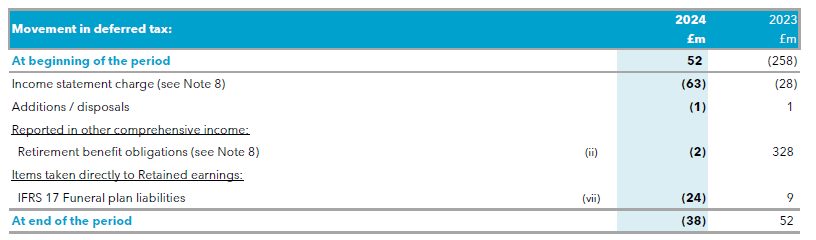

Of the £26m tax taken directly to the consolidated statement of comprehensive income, £2m debit (2023: £328m credit) arises on the actuarial movement on employee pension schemes with the main movement through OCI being the £24m debit in relation to IFRS 17. There was no movement this year directly to the consolidated statement of comprehensive income in respect of investment properties revaluations.

Based on legislation previously passed, the corporation tax rate increased from 19% to 25% with effect from 1 April 2023. To the extent the above deferred tax assets and liabilities are expected to crystalise after this date they should be valued using 25%. The bulk of the deferred tax assets and liabilities, as shown in Note 14, are expected to crystalise over a much longer time frame, being mainly the retirement benefit obligations, capital allowances on fixed assets and unrealised gains on investment properties, rolled-over gains and historic business combinations. As the rate of corporation tax will be 25% for all periods after the period end, it is appropriate to recognise deferred tax at that rate.

Tax policy

We publish our tax policy on our website (https://www.co-operative.coop/ethics/tax-policy) and have complied with the commitments set out in that policy.

Pillar 2

The OECD has promoted Pillar 2 reform and this has now been introduced into the UK tax system. The new rules are designed to promote the international actions put forward by the OECD to impose a minimum tax rate of 15%. The Co-op have considered the new rules and concluded that its prevailing Effective Tax Rate is above 15% and that therefore the Pillar 2 rules have no application in terms of affecting the Group’s tax cost. This is mainly due to prevailing and integral permanent differences in the Group’s tax calculations which will have the impact of increasing the accounting Profit Before Tax for the foreseeable future.

Footnotes to Taxation note 8:

i) The Group is not tax-paying in the UK in respect of 2024 due to the fact it has offset its current year profits by utilising some of its brought forward tax attributes. The tax attributes used have mainly been brought forward capital allowances (£373m gross claimed in 2024) and tax losses (£5m gross utilised in 2024) that offset its taxable profits for the period. These allowances and losses are explained in more detail in Note 14. The current tax charge nets to £nil.

Outside of the UK, our Isle of Man resident subsidiary, Manx Co-operative Society, a convenience retailing business in the Isle of Man showed a small profit in 2024, giving rise to a small current tax liability of £0.2m (2023: £0.1m). This is the Group’s only non-UK resident entity for tax purposes, which employs 89 parttime and 147 full-time colleagues out of our total Group headcount figure. All other income in the consolidated income statement is generated by UK activities and all other colleagues are employed in the UK.

The 2024 revenue of Manx Co-operative Society is £42m and all other revenue reflected in the consolidated income statement is generated by UK trading activities. The net assets of Manx Co-operative Society at 4 January 2025 were £16m, compared to net assets of the consolidated Group of £2,198m. The Manx assets represent the only overseas trading assets within the Group. A full copy of the most recent accounts is available here https://www.cooperative.coop/investors/rules. The presence of this Isle of Man resident subsidiary has not resulted in any additional tax charge in 2024 over and above that payable to the Isle of Man authorities stated above. If these activities had been carried out in the UK, these profits would have been included within the Group’s taxable profit prior to the availability of capital allowances and tax losses.

ii) Deferred tax is an accounting concept that reflects how some income and expenses can affect the tax charge in different periods to when they are reflected for accounting purposes. These differences are a result of tax legislation which require us to make these adjustments in our annual tax returns. The £73m deferred tax charge mainly relates to the net use of temporary differences in respect of the movements on pension assets and capital allowances not yet claimed. Note 14 gives further detail on how each deferred tax balance has moved in the year.

iii) The deferred tax adjustments in respect of prior years is a common adjustment. It reflects the difference between what is known at the time and reflected in the notes to these accounts and when the final tax returns are submitted to HMRC. In this year, we have made an £11m credit adjustment in respect of prior years.

iv) Some expenses incurred by the Group may be entirely appropriate charges for inclusion in its financial statements but are not allowed as a deduction against taxable income when calculating the Group’s tax liability. Examples of this include some repairs, entertaining costs and certain legal costs.

v) During the year the Group incurred expenditure on depreciating fixed assets which do not qualify for capital allowances. As this expenditure will never attract tax relief, this has led to an adjusting difference on the reconciliation.

vi) During the year a number of properties were sold, where the net taxable profit was more than the accounting profit.

vii) It is a requirement to measure deferred tax balances at the substantively enacted corporation tax rate at which they are expected to unwind. As the enacted deferred tax rate is the same as the current tax rate of 25%, there has been no difference to record this year.

Accounting policies

Income tax on the profit or loss for the period is made up of current and deferred tax. Income tax is recognised in the income statement except to the extent that it relates to items recognised directly in reserves, in which case it is recognised in other comprehensive income. Current tax is the expected tax payable on the taxable income for the period, using tax rates enacted or substantively enacted at the balance sheet date, and any adjustment to tax payable in respect of previous years.

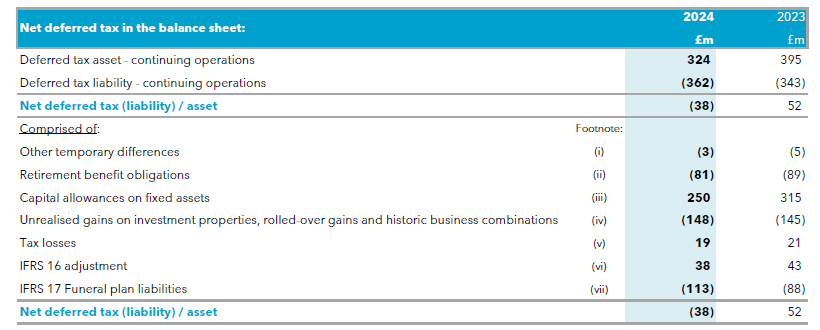

14 Deferred taxation

Deferred income taxes are calculated on all temporary differences under the liability method using an effective tax rate of 25.0% (2023: 25.0%). Temporary differences arise because sometimes accounting and tax requirements mean that transactions are treated as happening at a different time for accounting purposes than they are for tax purposes.

The movements in the net deferred tax (liability) / asset during the period are set out below:

Finance Act 2021 enacted an increase in the main rate of corporation tax to 25% to take affect from 1 April 2023. As the temporary differences which would give rise to a corporation tax charge at the point they unwind, will fall after the increase in rate to 25%, the appropriate rate at which to charge deferred tax, is also 25%. Due to the Group’s improved performance during the year, the Group has utilised deferred tax assets to the extent that the net deferred tax balance is now a net deferred tax liability of £38m (2023 net deferred tax asset was £52m).

Footnotes:

i) This amount includes deferred tax liabilities that arose on the acquisition of Nisa Retail Limited in 2018 and the adoption of IFRS 9, also in 2018. These are partially offset by a deferred tax asset in respect of provisions. Expenses that have not yet been incurred are able to be recorded in the accounts as provisions. However, of these certain expenses don’t receive tax relief until they have been paid for and so the related tax relief is delayed to a future period. During 2024 the amount of expense provisions deferred for tax purposes increased leading to a slightly smaller net liability being shown.

ii) During the period, the Group’s pension scheme surplus decreased by £32m resulting in a decrease in the corresponding deferred tax liability of £8m. This amount represents the theoretical future tax cost to the Group in respect of the current pension scheme surplus.

iii) A deferred tax asset arises on capital allowances where the tax value of assets is higher than the accounts value of the same fixed assets. The reason the Group has a higher tax value for these fixed assets is due to the fact the Group has not made a claim to its maximum entitlement to capital allowances since 2013 due to reduced levels of trading profits in the intervening years. However, impairment, disposals and depreciation have continued to reduce the accounts value for our assets. The Group expects to use these allowances to reduce future trading profits.

iv) This amount represents the theoretical amount of tax that would be payable by the Group on (a) the sale of all investment properties, (b) the sale of properties that have been restated at their fair value on historic mergers and transfers of engagements and (c) the sale of any property that has had an historic capital gain ‘rolled into’ its base cost (which is an election available by statute designed to encourage businesses to reinvest proceeds from the sale of trading properties into new trading properties and ventures). The £4m increase in the liability over the year is mainly due to disposal of properties under class (c) above.

v) The Group has incurred trading losses and interest losses that were in excess of taxable profits in the past. These losses can be used to reduce future trading profits and capital gains which are included in future tax forecasts for the Group. The restriction on the amount of losses that can be used in any one year post 1 April 2017, being £5m plus 50% of any surplus taxable profits above this amount, is not expected to limit the use of these losses other than extend the time over which they will be claimed.

The decrease in asset of £1m is in respect of amounts offset against taxable profits this year.

vi) Deferred tax that arose on the adoption of IFRS 16 in 2019 will unwind over a number of years and reduce taxable profits in those future years. The decrease in asset of £5m is mainly in respect of the unwind during the year.

(vii) These movements relate to the application of IFRS 17 which require us to recognise gains and losses through our Profit Before Tax as well as through our Other Comprehensive Income. Both of these amounts are treated as taxable and have led to an £24m deferred tax charge in Other Comprehensive Income.

Accounting policies

Deferred tax is provided for, with no discounting, using the balance sheet liability method, providing for temporary differences between the carrying amounts of assets and liabilities for financial reporting purposes and the amounts used for taxation purposes. The following temporary differences are not provided for: the initial recognition of assets or liabilities that affect neither accounting nor taxable profits, and differences relating to investments in subsidiaries to the extent that they will probably not reverse in the foreseeable future. The amount of deferred tax provided is based on the expected manner of realisation or settlement of the carrying amount of assets and liabilities, using tax rates enacted or substantively enacted at the balance sheet date. A deferred tax asset is recognised only to the extent that it is probable that future taxable profits will be available to use the asset against. Deferred tax assets are reduced to the extent that it is no longer probable that the related tax benefit will be realised.