RS Group plc – Annual report – 31 March 2025

Industry: distribution

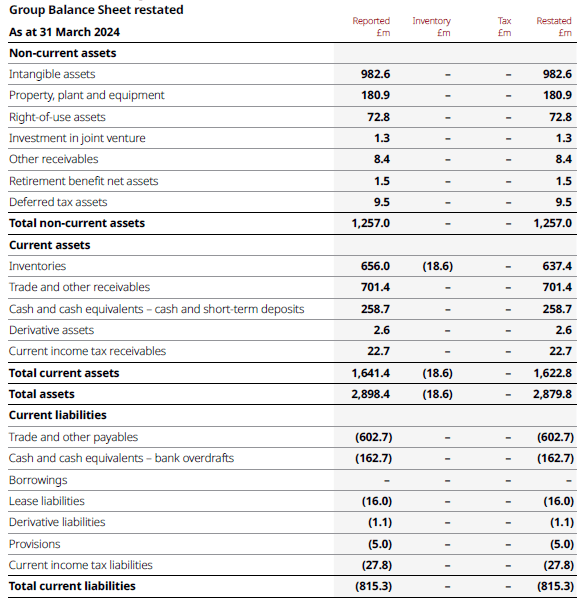

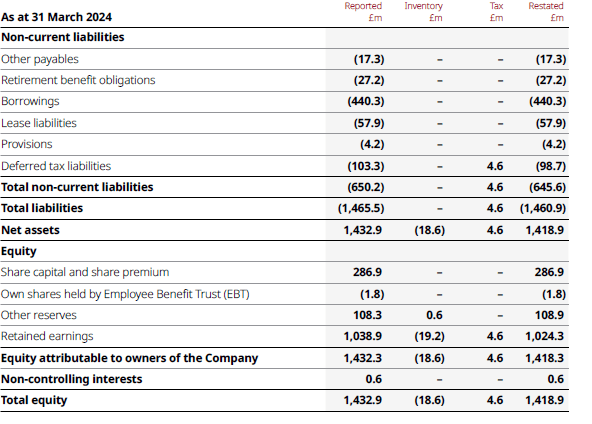

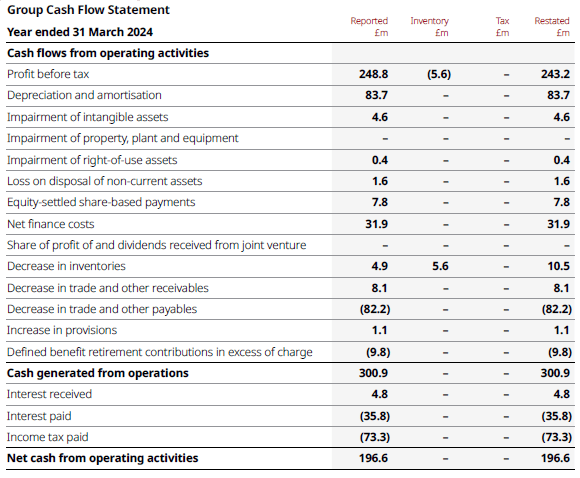

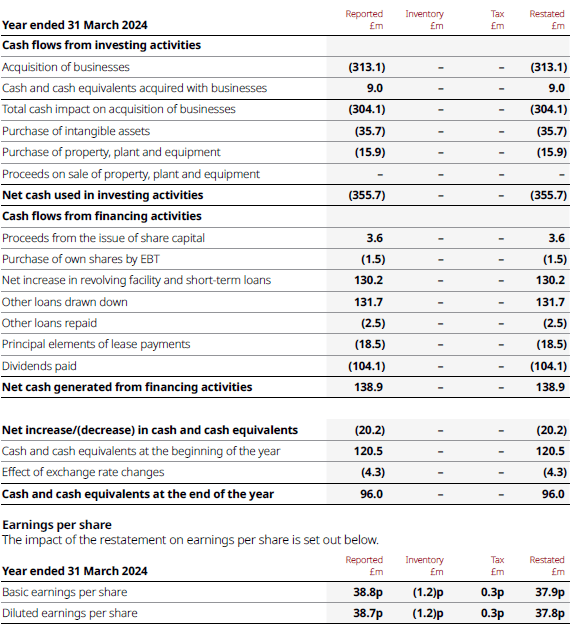

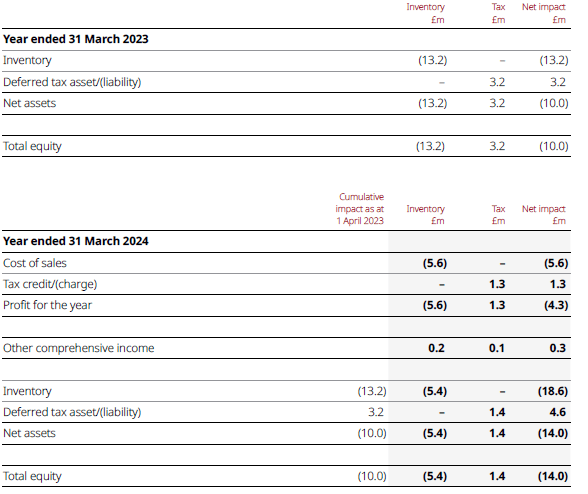

32 Prior Period Adjustments

The Group identified a prior period adjustment, impacting the opening position at 1 April 2023 and the year ended 31 March 2024. The impact of the prior period adjustment on the primary statements is presented in the tables below.

Inventory and related tax balances

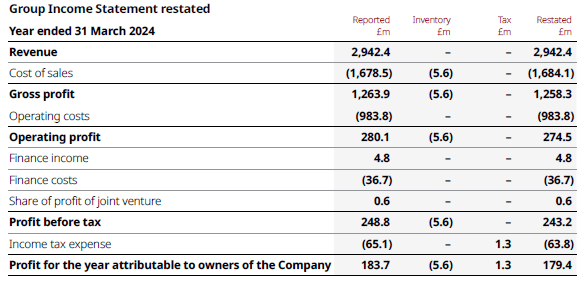

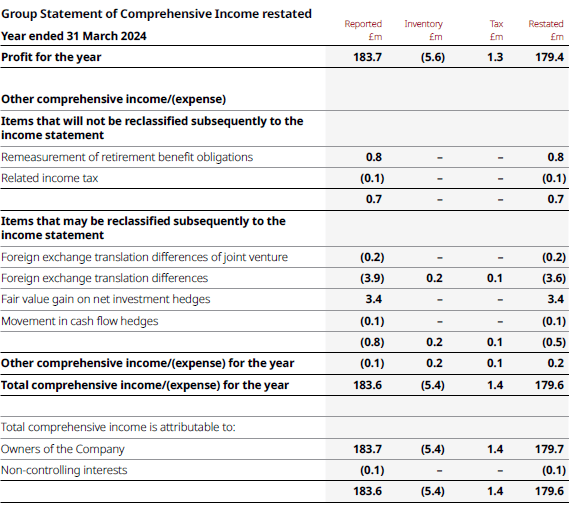

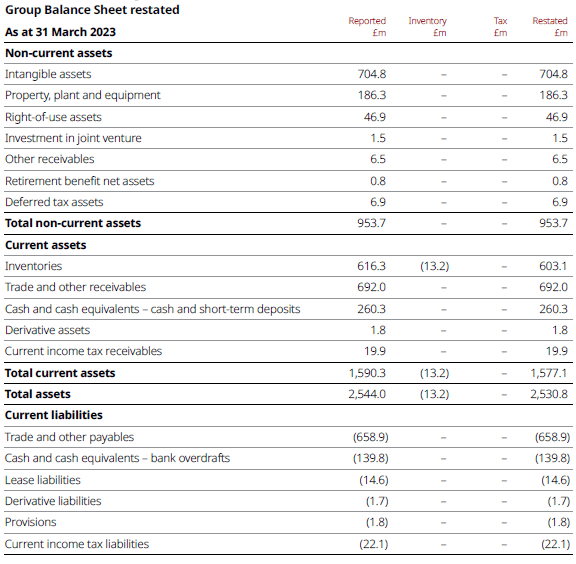

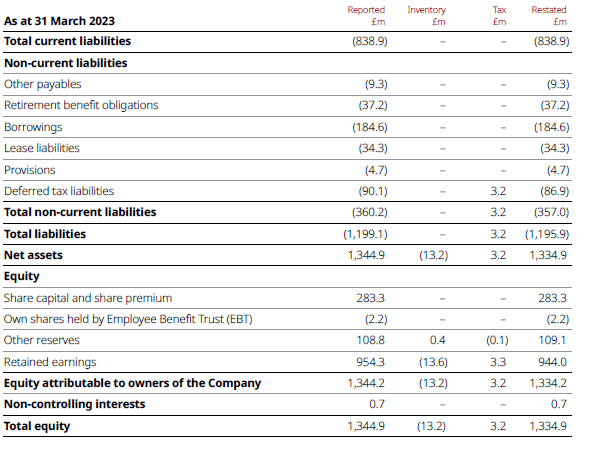

During the year ended 31 March 2025, the Group identified errors in relation to the calculation of the inventory obsolescence provision. As explained in Note 18, in order to determine the value of the inventory provision, inventory is allocated into different categories based on the number of years required to sell the amounts held, based on the current “run rate” of sales. Depending on the number of years’ sales required, different provisioning percentages are applied to each category in order to estimate the recoverable value.

During the year, the Group identified that certain inventory lines had been allocated to the incorrect category and as a result, an incorrect provisioning percentage had been applied in determining the inventory provision in previous periods. In addition, it was identified that the Group provisioning policy was not being consistently applied across the Group. As a result, comparative financial information has been restated to correct for the incorrect classification of amounts between categories, and the failure of certain components to comply with the Group’s internal provisioning policies.

The aggregate impact of the two errors is an overstatement of the Group inventory in the opening balance sheet and comparative period.

The restatement decreases the Group’s inventory balance by £13.2 million at 1 April 2023 and by a further £5.4 million for the year 2023/24.

As a consequence of the above change there is an impact on taxation. There is an additional credit to the deferred tax balance of £3.2 million as at 1 April 2023 and a further £1.3 million credit recognised in 2023/24.

The net impact on opening reserves as at 1 April 2023 was £10.0 million including £0.3 million impact on the translation reserve. In the year 2023/24, the impact on profit after tax was £4.3 million and on total comprehensive income was £0.3 million.

The table below details the impact of the prior year adjustment on the affected line items in the opening balance sheet (year ended 31 March 2023) and the comparative period (year ended 31 March 2024):

The following tables summarise the Group’s primary financial statements for the periods indicated, giving effect to the restatement described above.