ČEZ, a. s. – Annual report – 31 December 2024

Industry: utilities

2. Summary of Significant Accounting Policies (extract)

2.23. Nuclear Provisions

The Group makes a provision for nuclear decommissioning, a provision for interim storage of spent nuclear fuel and other radioactive waste, and a provision for the funding of subsequent permanent disposal of spent nuclear fuel and irradiated reactor components (see Note 21.1).

The provisions made correspond to the best estimate of the expenditure required to settle the present obligation at the end of the reporting period. The estimate, expressed at the price level at the date of estimate, is discounted using an estimated long-term risk-free real interest rate of 1.9% and 2.1% per annum as at December 31, 2024 and 2023, respectively, so as to take into account the timing of expenditure. While estimating future expenses, an associated risk related to these future expenses is taken into account. This risk adjustment can be expressed as a reduction of the used discount rate by 1.5% and 1.9% as at December 31, 2024 and 2023, respectively. Initial discounted costs are capitalized as part of property, plant and equipment and then amortized for the duration of time for which nuclear power plants will generate electricity. Each year, the provision is increased to reflect the accretion of discount and to accrue an estimate for the effects of inflation. Such expenses are recognized in the statement of income in the line item Interest expense on provisions. The effect of the expected rate of inflation is estimated at 2.2% and 2.6% as at December 31, 2024 and 2023, respectively.

The process of nuclear power plant decommissioning is estimated to continue for approximately 45 years after the termination of electricity generation. It is assumed that a permanent repository for spent nuclear fuel will commence operation in 2050 and the disposing of stored spent nuclear fuel at the repository will continue until approximately 2090. Although the Group has made the best estimate of the amount of nuclear provisions, potential changes in technology, changes in safety and environmental requirements, and changes in the duration of such activities may result in actual costs varying considerably from the Group’s current estimates.

Changes in estimates concerning the provisions for nuclear decommissioning and permanent disposal of spent nuclear fuel resulting from new estimates of the amount or timing of cash flows required to settle these obligations or from a change in the discount rate are added to, or deducted from, the amount recognized as an asset in the balance sheet. Should the amount of the asset be negative, i.e., should the deducted amount exceed the amount of the asset, the difference is recognized directly in profit or loss.

2.7. Fuel Costs

Fuel is recognized as costs when it is consumed. Fuel costs include the depreciation of nuclear fuel (see Note 2.9).

2.8. Property, Plant and Equipment (extract)

Property, plant and equipment are measured at cost less accumulated depreciation and impairments. The cost of property, plant and equipment comprises the purchase price and the related cost of materials and labor and the cost of debt financing used in the construction. The cost also includes the estimated cost of dismantling and removing a tangible asset to the extent specified by IAS 37, Provisions, Contingent Liabilities, and Contingent Assets. Government grants and similar subsidies received for the acquisition of property, plant and equipment decrease the cost.

2.9. Nuclear Fuel

The Group recognizes nuclear fuel as part of property, plant and equipment because the period for which it is used for electricity generation exceeds 1 year. Nuclear fuel is measured at cost less accumulated depreciation and, if applicable, impairments. Nuclear fuel includes a capitalized portion of the provision for interim storage of spent nuclear fuel. The depreciation of nuclear fuel in a reactor is determined on the basis of the amount of energy generated and presented in the statement of income in the line item Fuel and emission rights. The depreciation of nuclear fuel includes additions to the provision for interim storage of spent nuclear fuel.

2.24. Provisions for Decommissioning and Reclamation of Mines and Mining Damages

The Group has recognized a provision for obligations to decommission and reclaim (see Note 21.2). The provision recognized represents the best estimate of the expenditures required to settle the present obligation at the current balance sheet date. Such estimate, expressed at the price level at the date of estimate, are discounted at December 31, 2024 and 2023, using an estimated long-term risk-free real interest rate to take into account the timing of payments in amount of 1.9% and 2.1% per annum, respectively. While estimating future expenses, an associated risk related to these future expenses is taken into account. This risk adjustment can be expressed as a reduction of the used discount rate by 1.5% and 1.9% as at December 31, 2024 and 2023, respectively. The initial discounted cost amounts are capitalized as part of property, plant and equipment and are depreciated over the lives of the mines. Each year, the provision is increased to reflect the accretion of discount and to accrue an estimate for the effects of inflation. These expenses are presented in the income statement in the line Interest on provisions. The effect of the expected rate of inflation is estimated at 2.2% and 2.6% as at December 31, 2024 and 2023, respectively.

Although the Group has made the best estimate of the amount of provision for decommissioning and reclamation of mines and mining damages, potential changes in technology, changes in safety and environmental requirements, and changes in the duration of such activities may result in actual costs varying considerably from the Group’s current estimates.

Changes in a decommissioning liability that result from a change in the current best estimate of timing and/or amount of cash flows required to settle the obligation or from a change in the discount rate are added to (or deducted from) the amount recognized as the related asset. However, to the extent that such a treatment would result in a negative asset, the effect of the change is recognized directly in profit or loss.

2.25. Provision for Demolition and Dismantling of Fossil-fuel Power Plants

The Group has recognized a provision for demolition and dismantling of fossil-fuel power plants after their decommissioning (see Note 21.2). The provision created corresponds to the best estimate of the expenditures required to settle the present obligation at the balance sheet date. The estimate, expressed in the price level at the date of estimate, is discounted using an estimated risk-free real interest rate of 1.5% and 1.7% per annum as at December 31, 2024 and 2023, respectively, in order to take into account the timing of expenditures. While estimating future expenses, an associated risk related to these future expenses is taken into account. This risk adjustment can be expressed as a reduction of the used discount rate by 1.7% and 1.8% as at December 31, 2024 and 2023, respectively. Initial discounted costs are capitalized as part of property, plant and equipment and then depreciated over the period during which coal power plants will generate electricity. Each year, the provision is increased to reflect the accretion of discount and to accrue an estimate for the effects of inflation. These expenses are recognized in the statement of income in the line item Interest on provisions. The effect of the expected rate of inflation is estimated at 2.2% and 2.9% as at December 31, 2024 and 2023, respectively.

Although the Group has made the best estimate of the amount of provision for demolition and dismantling of fossil-fuel power plants, potential changes in technology, changes in safety and environmental requirements, and changes in the duration of such activities may result in actual costs varying considerably from the Group’s current estimates.

Changes in estimates concerning the provision resulting from new estimates of the amount or timing of cash flows required to settle these obligations or from a change in the discount rate are added to, or deducted from, the amount recognized as an asset in the balance sheet. Should the amount of the asset be negative, i.e., should the deducted amount exceed the amount of the asset, the difference is recognized directly in profit or loss.

2.4. Estimates and Accounting Judgments

The Group makes significant estimates when determining the recoverable amounts of property, plant and equipment and intangible assets (see Note 7), accounting for the nuclear provisions (see Note 21.1), provisions for reclamation of mines, mining damages and waste storage reclamation (see Note 21.2), provision for demolition and dismantling of fossil-fuel power plants (see Note 21.2), unbilled electricity and gas (see Note 2.6), fair value of commodity contracts (see Notes 2.15 and 19), non-commodity derivatives (see Notes 2.14 and 19), incremental borrowing rate and lease terms to measure lease liabilities (see Notes 2.27 and 25) and deferred tax calculation (see Notes 2.21 and 36). Actual outcome may vary from these estimates.

The most significant changes in estimates in 2024 related to the provision for long-term spent fuel storage due to the increase of expected contribution to the nuclear account depending on electricity generated in nuclear power plants and to the change of the discount rate and provision for nuclear decommissioning due to the change of the discount rate.

Another significant change in estimates in 2024 related to adjustment of depreciations and depreciating methods of certain asset classes. IFRS accounting standards require depreciation methods to be reviewed periodically and that the depreciation methods used reflect the expected way in which the economic benefits of the assets will be consumed. When significant changes occur in the expected distribution of consumption of future economic benefits from certain assets, the method is being changed to reflect the changed distribution of consumption of benefits.

Regarding the effects of decarbonization and the assumptions of further market development, the Group examined depreciation methods. The result is a change in the accounting estimate for the depreciation method for coal generation resources 1) and for assets used in lignite mining (collectively “coal assets”). Up to September 30, 2024, coal assets were depreciated on a linear basis over the expected remaining useful life. From October 1, 2024, the Group depreciates coal assets using a method in which depreciation decreases evenly over the remaining useful life (the so-called sum-of years’ digits method). This method for coal assets appropriately captures the expected way of consumption of economic benefits in the future, when the gradually decreasing usage of these assets is expected.

The depreciable amount of the Group’s coal assets was CZK 73.2 billion as at September 30, 2024. The following table shows the depreciation schedule as a percentage of the depreciable amount as at September 30, 2024, after the change in the depreciation method until 2030, which represents the currently expected end of operation of the coal assets:

Compared to the linear method of depreciation previously used, there is therefore a significant change in the distribution of depreciation over time. With regard to the different effective income tax rate in individual future years, which is affected by the windfall tax, which applies in the Czech Republic until December 31, 2025, and is relevant for ČEZ, a. s., there is a change in the estimate of when the taxable temporary differences related to the different net book value for accounting and tax purposes of the coal assets will be realized by depreciation (tax-deductible depreciation of ČEZ, a. s., does not change). Higher temporary differences realized in periods with a higher effective tax rate led to an increase in the deferred tax liability in the amount of CZK 4,885 million as at September 30, 2024. The related deferred income tax expense was reported as a one-off item in the line item Income tax in the statement of income as at September 30, 2024.

The most significant changes in estimates in 2023 related to the provision for nuclear decommissioning due to update of the expert decommissioning studies for Dukovany and Temelin Nuclear Power Plants, change of the discount rate and determining the recoverable amount of property, plant and equipment and intangible assets.

1.1. Strategy of the Company in the Context of Climate Changes

The “VISION 2030 – Clean Energy of Tomorrow” strategy is focused on dynamic transformation of the generation portfolio to low-emission one and achievement of full climate neutrality already by 2040. The strategy includes a commitment to fundamentally limit the production of heat and electricity from coal and fundamentally reduce the emission intensity by 2030. In areas of distribution and sales, the basic goal is to provide the most advantageous energy solutions and the best customer experience on the market. The goal to develop CEZ Group responsibly and sustainably in accordance with ESG principles is also among the main priorities.

This strategy considers and responds to the regulatory environment of the European Union and its expected development. A key element is the EU’s climate goals contained in particular in the European Green Deal communication from 2019, which includes, among other things, an increase in the goal in the area of reducing greenhouse gas emissions and the full decarbonization of Europe (the goal for reducing emissions by 2030 compared to 1990 was increased to 55%). Furthermore, in 2021, the European Commission came up with the Fit for 55 package and, in response to the Russian invasion of Ukraine, with the REPowerEU measure, which ultimately led to the setting of a target for the share of renewable energies in the total gross final energy consumption at a level of at least 42.5% in 2030. In December 2024, the government of the Czech Republic approved the updated National Energy and Climate Plan, which main points cover the continuance of generation of electricity by nuclear and renewable sources to decrease emissions; gas should be used as a temporary source of energy, which will be fully replaced by renewable sources and low-emission gasses, mainly by hydrogen, by the year 2050. The goal is to reduce green-house gas emissions by 55% until the year 2030 through the expansion of renewable sources, energy savings and gradual cessation of use of fossil fuels, including the cessation of coal mining and combustion by the year 2033.

As one of the tools for achieving these climate goals, which has a significant impact on the Company, is the emission rights market in Europe. The European Union influences the market for these emission rights, for example by introducing a Market Stability Reserve (MSR), by reducing the total number of emission rights or by releasing them onto the market (back-loading). With increased decarbonization efforts, the market price of CO2 emission rights receives a long-term growth stimulus; older, less efficient coal-fired power plants and heating plants or, in general, equipment cost-linked to the price of emission rights get under considerable economic pressure.

The biggest impact of these trends is on the assets of segment Mining and on coal and gas generation assets of the Group. CEZ Group’s strategy anticipated this development in the long term, and therefore measures and strategic steps are being continuously implemented with the aim of minimizing the negative impact of these factors on the Group’s value and at the same time making maximum use of the new opportunities that these trends bring for the Group.

The impacts of climate changes, but also a number of other factors, are evaluated in the various estimates and accounting judgments that the preparation of financial statements according to IFRS requires (see Note 2.4). Mainly it relates to determination of recoverable amount of property, plant and equipment and intangible assets (Note 7), of the provision for mine reclamation and mining damages (Note 21.2), of the provision for demolition and dismantling of fossil-fuel power plants (Note 21.2) and of remaining useful life and depreciation methods of property, plant and equipment used for depreciation (Note 2.8).

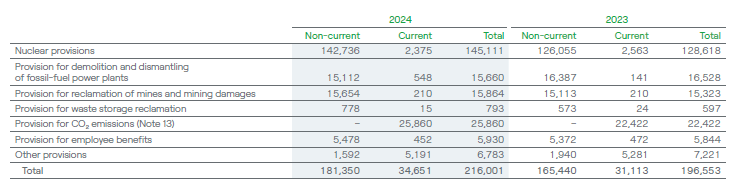

21. Provisions (extract)

The following table provides an overview of provisions as at December 31, 2024 and 2023 (in CZK millions):

21.1. Nuclear Provisions

The Company operates two nuclear power plants. The Dukovany Nuclear Power Plant comprises four units commissioned for continuous operation between 1985 and 1987. The Temelin Nuclear Power Plant consists of two units that were commissioned for continuous operation in 2002 and 2003. The Nuclear Energy Act sets down obligations for nuclear facility decommissioning and disposal of radioactive waste and spent nuclear fuel. In accordance with the Nuclear Energy Act, all the nuclear parts and equipment of a nuclear power plant must be disposed of after the end of operation. For the purpose of determining the amount of nuclear provisions, it is estimated that the Dukovany Nuclear Power Plant will stop generating electricity in 2047, the Temelin Nuclear Power Plant in 2062. Decommissioning cost studies for Dukovany Nuclear Power Plant from 2022 and for Temelin Nuclear Power Plant from 2023 assume that the total costs of decommissioning of so-called nuclear island and conventional part of these power plants will reach the amount of CZK 45.3. billion and CZK 36.9 billion, respectively. The Company makes contributions to a restricted bank accounts in the amount of the nuclear provisions recorded under the Nuclear Energy Act. These funds can be invested in government bonds in accordance with legislation. These restricted financial assets are reported in the balance sheet as part of the line item Restricted financial assets (see Note 4).

The Ministry of Industry and Trade established the Radioactive Waste Repository Authority (SURAO) as the central organizer and operator of facilities for the final disposal of radioactive waste and spent fuel. The SURAO operates, supervises and is responsible for disposal facilities and for disposal of radioactive waste and spent fuel therein. The activities of the SURAO are financed through a nuclear account funded by the originators of radioactive waste. Contribution to the nuclear account is stated by Nuclear Energy Act at CZK 55 per MWh produced at nuclear power plants. In 2024 and 2023, the payments to the nuclear account amounted to CZK 1,633 million and CZK 1,673 million, respectively. The originator of radioactive waste and spent fuel directly covers all costs associated with interim storage of radioactive waste and spent fuel.

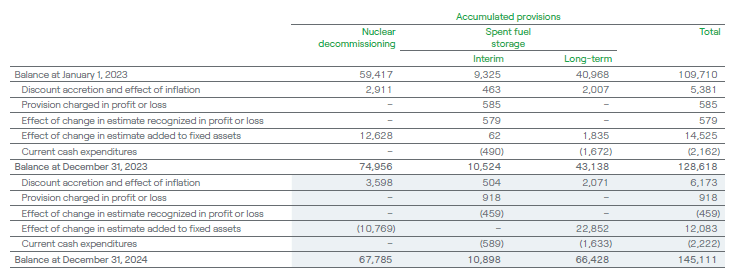

The Group has established provisions for estimated future expenses on nuclear decommissioning and interim storage and permanent disposal of spent nuclear fuel in accordance with the principles described in Note 2.23.

The following is a summary of the provisions for the years ended December 31, 2024 and 2023 (in CZK millions):

The use of the provision for permanent disposal of spent nuclear fuel in a current year comprises payments made to the government-controlled nuclear account and the use of the provision for interim storage represents, in particular, purchases of containers for spent nuclear fuel and other related equipment for these purposes.

In 2024, the Company recorded the change in estimated provision for interim storage of spent nuclear fuel. The change relates to the change in expected future storage costs and change in discount rate. The change in estimated provision for nuclear decommissioning is due to the change in the amount of costs for decommissioning of Dukovany Nuclear Power Plant and Temelin Nuclear Power Plant and due to the change in discount rate. The change in estimated provision for long-term spent fuel storage is connected with the modification of the expected output of the nuclear power plants, change of expected contribution to the nuclear account per MWh in future years and change in discount rate.

In 2023, the Company recorded the change in estimated provision for interim storage of spent nuclear fuel. The change relates to the change in expected future storage costs and change in discount rate. The change in estimated provision for nuclear decommissioning is due to the update of the expert decommissioning studies for Dukovany Nuclear Power Plant and for Temelin Nuclear Power Plant and due to the change in discount rate. The change in estimated provision for long-term spent fuel storage is connected with the modification of the expected output of the nuclear power plants, change of expected contribution to the nuclear account per MWh in future years and change in discount rate.

The actual decommissioning and spent fuel storage costs could vary substantially from the above estimates because of new regulatory requirements, changes in technology, increased costs of labor, materials and equipment and/or the actual time required to complete all decommissioning, disposal and storage activities.

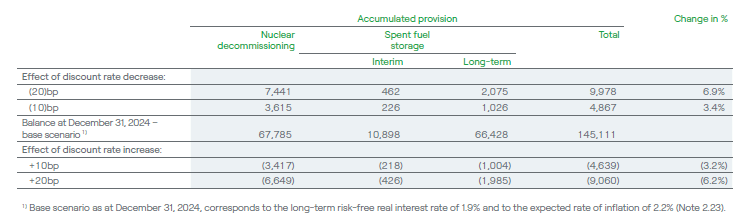

The following table shows the sensitivity of nuclear provisions to changes in the discount rate, keeping all other parameters unchanged, as at December 31, 2024 (in CZK millions):

21.2. Provisions for Mine Reclamation and Mining Damages, Waste Storage Reclamation and Demolition and Dismantling of Fossil-fuel Power Plants

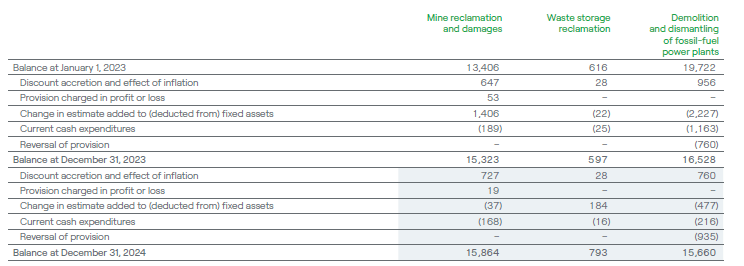

The following table shows the movements of provisions for the years ended December 31, 2024 and 2023 (in CZK millions):

The provision for decommissioning and reclamation of mines and the provision for mining damages were recorded by Severočeske doly a.s., a mining subsidiary of ČEZ. Severočeske doly a.s. operates open pit coal mines and is responsible for decommissioning and reclamation of the mines as well as for damages caused by the operations of the mines. Current cash expenditures represent cash payments for current reclamation of mining area and settlement of mining damages. The use of the provision for decommissioning and reclamation of mines is not so intense during the period, when the mining is in progress (the cease of mining is expected in 2030). The highest use of the provision is expected during years 2031–2040 (CZK 11.5 billion in present value) in relation to solution of the residual pits. Mine reclamation should be finalized in 2045, during years 2041–2045 is expected the use of provision of CZK 1.6 billion in present value. This expected future time course of using the provision is uncertain and corresponds to the current strategy of the Group (Note 1.1). Changes in estimate in 2024 and 2023 represent change in provision as result of updated cost estimates in the current period, mainly due to changes in expected prices of reclamation activities, and also due to changes in their timing and in the discount rate.

The use of the provision for demolition and dismantling of fossil-fuel power plants in 2023 was related especially to generation unit Pruneřov I, whose demolition and dismantling was completed in 2023. For the next years, the use of provision is expected mainly in 2029–2030 for power plant Dětmarovice (CZK 2.3 billion in present value), in 2031–2034 for remaining coal-fired power plants (CZK 9.9 billion in present value) and in 2047–2048 for combined-cycle gas turbine in Počerady (CZK 0.5 billion in present value). This expected future time course of using the provision is uncertain and corresponds to the current strategy of the Group (Note 1.1). In 2024 and 2023, the Group recorded the change in estimate in provision for demolition and dismantling of fossil-fuel power plants due to the update of the amount and scope of the decommissioning costs and due to change in discount rate.

The actual decommissioning and reclamation of mines and mining damages could vary substantially from the above estimates, because of new regulatory requirements, changes in technology, increased costs of labor, materials and equipment and/or the actual time required to complete all related operations.

4. Restricted Financial Assets

The overview of restricted financial assets at December 31, 2024 and 2023, is as follows (in CZK millions):

The Czech government bonds are measured at fair value through other comprehensive income. The restricted financial assets contain in particular restricted financial assets to cover the costs of nuclear decommissioning, to cover the costs for mine reclamation and mining damages and for waste storage reclamation.