RS Group plc – Annual report – 31 March 2025

Industry: distribution

Viability statement

Assessment of prospects

Our business model and strategy, as described on page 11, is structured so that the Group is a digitally enabled global distributor of product and service solutions, providing small volumes of our suppliers’ products to satisfy our industrial customers’ MRO demands. We supply a very broad spread of customers both in terms of industry sector and geography. The Group is not reliant on one particular group of customers or suppliers, as its customer and supplier base continues to be diverse. Our business model is differentiated by: our global network of distribution sites; our customer-centric team; our strong supplier relationships; our broad and deep product offering and service solutions capabilities; and our strong digital presence. The Group has high inventory availability with products sourced from a large number of suppliers and provides customers with a reliable and fast service.

The Group’s results and financial position are reviewed monthly by both our ExCo and the Board. Every day the ExCo receives an analysis of the previous day’s revenue and gross margin. The Board receives and reviews regularly the monthly management accounts, including cash flows, and also receives regular performance and forecast updates from the CFO and CEO.

We update our detailed rolling forecast of the Group’s income statement, balance sheet and cash flows frequently which are regularly reviewed, and the assumptions approved, by the Board.

The Group’s long-term prospects are assessed primarily through our strategic and financial planning process. This includes the preparation of a five-year strategic plan and an annual budget setting process, involving both Group and regional management, which are updated annually and reviewed and approved by the Board. The ExCo receives and reviews progress against the strategic plan objectives regularly. The Board also receives updates and, if appropriate, the strategic plan is updated depending on progress and performance.

The Board also considers the long-term prospects of the Group as part of its regular monitoring and review of risk management and internal control systems, as described on page 36 and pages 86 to 88.

Our regular cash flow forecasts enable us to track our net debt position and to take any necessary actions on a timely basis. Our capital position is supported by regular reviews of the Group’s funding facilities and banking covenants’ headroom, through the Group’s Treasury Committee. In 2024/25 we agreed an extension to our €150 million loan, which now matures in October 2028. Our £400 million multi-currency revolving facility now matures in November 2029. Only £113 million of this facility was drawn down at 31 March 2025.

As described throughout this Annual Report and Accounts, the Group’s performance was impacted by the challenging macroeconomic environment over the past year and the further unwinding of our pandemic-related trading benefit. As a result, like-for-like revenue declined by 2%. An improvement in working capital led to an increase of 40% in adjusted free cash flow to £215 million and net debt of £364 million (including lease liabilities of £57 million) at 31 March 2025. We also paid dividends during the year of £105 million (2023/24: £104 million). We have ended the year with a strong balance sheet.

Details of our sources of finance are outlined in Note 23 on pages 179 to 183. The earliest facilities maturing being two tranches of our private placement loan notes in 2026/27 totalling £76.9 million.

The Group’s debt covenants are EBITA to interest to be greater than 3:1 and net debt to adjusted EBITDA to be less than 3.25:1. At 31 March 2025 EBITA to interest was 10.9x (2023/24 restated: 10.3x) and net debt to adjusted EBITDA was 1.1x (2023/24 restated: 1.2x) (see Note 3 on pages 154 to 158 for reconciliations) and under our strategic plan these are also comfortably met.

Viability assessment period

In its assessment of the Group’s viability, the Board has reviewed the assessment period and has determined that a three-year period to 31 March 2028 continues to be most appropriate. The robustness of the strategic plan is higher in the first three years. The Group has few contracts with either customers or suppliers extending beyond three years and, in the main, contracts are for one year or less. The business operates with a minimal forward order book, generally taking orders and shipping them on the same day. In addition, as more business becomes digital and we become more agile, speed of change increases and so visibility is relatively short term. Of the Group’s long-term obligations, the UK pension scheme is the largest and its triennial funding valuation forms the basis of our agreeing its funding with its trustee. Our share-based payment schemes are also mainly for three years.

Assessment of viability

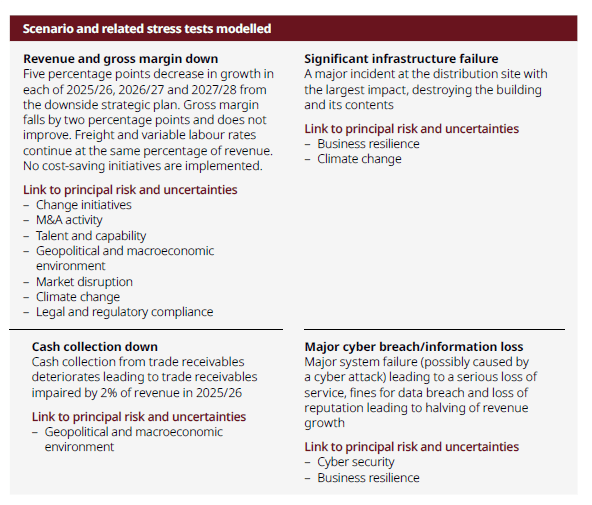

Each of the Group’s principal risks and uncertainties on pages 38 to 42 has a potential impact on the Group’s viability and so the Board considered various scenarios and examined a number of factors that could impact each in the future. It decided which scenarios would have the most impact on the viability of the Group and determined an appropriately severe, but plausible, stress test for each of these scenarios.

The strategic plan approved at the January 2025 Board meeting is considered to reflect the Board’s current best estimate of the future prospects of the Group. Therefore, in order to assess the viability of the Group, the scenarios and stress tests were modelled by overlaying them onto the downside version of the strategic plan to quantify the potential impact of one or more of them crystallising over the assessment period.

In performing the above tests it was assumed that capital expenditure is unchanged from that in the

strategic plan, there are no cost mitigation actions taken, dividends continue to be paid and there are no changes in or extensions to debt financing.

The results of the above stress tests showed the Group would be able to withstand the impact of these scenarios occurring.

Reverse stress tests were also undertaken to assess the circumstances that would threaten the Group’s current financing arrangements. These included significant declines in revenue, significant declines in both revenue and gross margin and a major deterioration in cash collection and would have to result in adjusted operating profit margin falling to under 3% in at least one of the following three years. Also, a reverse stress test of an acquisition of a significantly loss-making business was undertaken and would have to cost more than £300 million to use up our debt facilities. All these reverse stress tests assumed that no major reorganisations or significant working capital initiatives occur in mitigation, capital expenditure is unchanged from that in the strategic plan, dividends continue to be paid and there are no changes in or extensions to debt financing. The Board considers the risk of these circumstances occurring to be remote.

The above scenarios are hypothetical and extremely severe for the purpose of creating outcomes that have the ability to threaten the viability of the Group; however, multiple control measures are in place to prevent and mitigate any such occurrences from taking place. If any of these scenarios actually happened, various options are available to the Group to maintain liquidity so as to continue in operation.

Confirmation of viability

Based on the assessment outlined above, the Board has a reasonable expectation that the Group will be able to continue in operation and meet its liabilities as they fall due over the three years to 31 March 2028.

Going concern

The going concern period is defined as a period of at least 12 months from 20 May 2025. The same reverse stress tests were applied for the going concern period as for the viability modelling. These included significant declines in revenue, significant declines in both revenue and gross margin, a major deterioration in cash collection, and major under-performing acquisition. These reverse stress tests assumed that capital expenditure and operating costs are unchanged from those in the forecast, no significant working capital initiatives occur in mitigation, dividends continue to be paid and there are no changes in or extensions to debt financing.

Based on the assessment outline above and the output of our detailed rolling forecasts, the Board believes that it is appropriate to continue to adopt the going concern basis in preparing the Group’s accounts.