Stora Enso Oyj – Annual report – 31 December 2025

Industry: agriculture

1.2 Critical accounting estimates and judgements

The preparation of consolidated financial statements in accordance with IFRS requires management to make estimates, judgements and assumptions that affect the reported assets and liabilities, as well as the disclosure of contingent assets and liabilities at the reporting date and the reported income and expenses during the period. These estimates, judgments and assumptions might have a significant impact on the amounts recognised in the consolidated financial statements. The estimates are based on historical experience and various other assumptions that are believed to be reasonable and reflect management’s best estimates, though actual result and timing could differ from these. The estimates, judgements and assumptions are reviewed regularly and updated if there are changes in circumstances or as a result of new information. The accounting items presented below represent those matters which include the most estimation uncertainty and exercise of judgement. More details are included in the respective notes.

- Property, plant and equipment, intangible assets and right-of-use assets and Goodwill – note 2.4 Depreciation, amortisation and impairments

- Income taxes – note 2.6 Income taxes

- Post-employment benefits – note 3.3 Post-employment benefit obligations

- Leases – note 4.1 Intangible assets, property, plant and equipment and right-of-use assets

- Forest assets – note 4.2 Forest assets

- Fair value of financial instruments – note 4.4 Equity instruments and note 5.2 Fair values.

- Provisions – note 4.9 Provisions

4.2 Forest assets

Accounting principles

Stora Enso’s forest assets are defined as standing growing trees, classified as biological assets, and related forest land. Biological assets consist of standing trees to be used as raw material for pulp and mechanical wood production and as biofuels. Forest asset valuation is based on continuous operations and sustainable forest management, while also taking into account environmental restrictions and other reservations. Biological assets are recognised and valued in accordance with IAS 41 Agriculture at fair value, while forest land assets are recognised in accordance with IAS 16 Property, plant and equipment. Leased forest land assets are presented as part of right-of-use assets in note 4.1 Intangible assets, property, plant and equipment and right-of-use assets.

Nordic and plantation forest assets are classified as different asset classes due to their differing nature, usage, and characteristics. The main difference is the short-term growing cycle of 6–12 years in plantations versus the long-term growing cycle of 60–100 years in Nordic forests. There are also differences in regeneration methods, forest management, and the use of assets for other purposes.

Nordic forest assets include holdings in Sweden and Finland, while plantation forest assets include holdings in China, Brazil and Uruguay. Accounting policies for the different classes of forest assets are presented separately below. Additionally, the Group has minor forest asset holdings in Estonia and Romania through the associate company Tornator. The Group holds forest assets in its own subsidiaries in Sweden and China as well as in joint operations in Brazil and Uruguay, and in associate companies in Finland and Sweden. Stora Enso also ensures that the Group’s share of the valuation of forest holdings in associated companies and joint operations is consistent with Group accounting policies. At harvesting, biological assets are transferred to inventory.

Nordic forest assets

Forest assets in Sweden and Finland are recognised at fair value and valued using a market approach method based on forest market transactions in the areas where Stora Enso’s forests are located. Stora Enso’s forest assets create value by securing wood supply, increasing long-term yield, optimising land use and securing financial flexibility. They play an important role in mitigating climate change impacts, as growing trees absorb CO2. The forest lands offer additional opportunities for future value streams, such as wind power.

The total forest assets value is calculated with verified inventory data and regional standing stock prices, considering, among others:

- regional market transaction data based on the geographical locations of forest assets,

- standing stock prices by forest cubic metre (m³ fo) combined from traded forest estates and

- regional standing stock inventory.

Information relating to forest asset transactions is available from market data suppliers. Stora Enso applies three-year (36-month) weighted average market transaction prices which are considered to include a sufficient number of transactions and are estimated to represent market conditions at the reporting date. The market transaction information is viewed as market-corroborated inputs. Certain adjustments are made to refine the market-corroborated inputs using unobservable inputs; therefore, inputs are categorised based on Level 3 of the fair value hierarchy.

The total value of the forest assets in the Nordics is allocated across biological assets and forest land. The allocation of the combined fair value of forest assets is based on the income approach where the present values of expected net cash flows for both biological assets and forest land are calculated separately. The discount rate is determined as the rate at which the valuation, based on market transaction prices, matches the combined cash flows of total forest assets for biological assets and forest land. The discount rate is estimated to be the same for biological assets and forest land as the nature and timing of the cash flows are similar.

Biological assets are measured at fair value in accordance with IAS 41. The fair value is based on the income approach and the discounted cash flow method, whereby the fair value of the biological assets is calculated using cash flows from continuous operations, taking into account the growth potential of one cycle. Forest land is measured at fair value using the revaluation method, as defined in IAS 16. The fair value of forest land is measured based on the income approach, including net cash flows related to trees to-be-planted in the future as well as other land related income, such as wind power leases, hunting rights and soil material sales. The valuation of forest assets owned through Tornator Oyj in Estonia and Romania is based on the discounted cash flow method both for biological and land assets.

Changes in the fair value of biological assets are recognised in the income statement. Changes in the fair value of forest land, net of deferred taxes, are recognised in other comprehensive income (OCI) and accumulated in a revaluation reserve in equity. The revaluation reserve is not recycled to the income statement upon disposal. If the fair value of forest land were to be less than cost, the difference would be recognised in the income statement as an impairment loss.

Plantation forest assets

In plantation forest areas, biological assets are recognised at fair value in accordance with IAS 41 and based on the income approach in those areas where the Group has forest land. Fair value measurement is based on Level 3 of the fair value hierarchy. Forest land is measured initially and subsequently at cost, using the cost model as defined in IAS 16.

The valuation of biological assets is based on the discounted cash flow method. This method uses cash flows from continuous operations, incorporating sustainable forest management, and taking into account growth potential of one cycle. The fair value of biological assets is based on the productive forest land. The yearly harvest from the forecasted tree growth is multiplied by wood prices and the cost of silviculture and harvesting is deducted. The fair value of biological assets is measured as the present value of the harvest from one growth cycle, taking into consideration environmental restrictions and other reservations. The discount rate applied is determined using the weighted average cost of capital method.

Young standing timber less than two years old (less than three years in Montes del Plata) is considered to be an immature asset and accounted at cost. The fair value approximates the cost when little biological transformation has occurred or the impact of the transformation on the price is not expected to be significant. This varies according to the location and species of the assets.

Changes in the fair value of biological assets are recognised in the income statement. Forest land is measured at cost and not depreciated.

Critical accounting estimates and judgement

Biological assets

The fair value of biological assets is determined by using discounted cash flow method. These discounted cash flows require estimates of growth, harvesting, sales price, costs and discount rate. To determine the fair value of biological assets, management must estimate future price levels and trends for sales and costs and conduct regular surveys to establish the volumes of wood available for harvesting and their current growth rates.

Nordic forest assets

The fair value of forest assets in the Nordics is determined using a market approach, based on forest market transactions in the areas where Stora Enso’s forests are located. Market prices between areas vary significantly and judgement is applied to define relevant areas for market transactions used in valuation. The valuation of the forest assets is based on detailed transaction data and price statistics provided by market data suppliers. Judgement is applied when adjustments are made to reflect the specific characteristics and nature of Stora Enso’s forest assets and to exclude certain non-forest assets and outlier transactions. Stora Enso applies three-year (36 month) weighted average market transaction prices, which are considered to include a sufficient number of transactions and are estimated to represent market conditions at the reporting date.

The value of the forest assets is allocated to biological assets and forest land. The allocation of the combined fair value of forest assets is based on the income approach where the present values of expected net cash flows for both biological assets and forest land are calculated separately. The total net cash flows for each component include estimates for future cash flows.

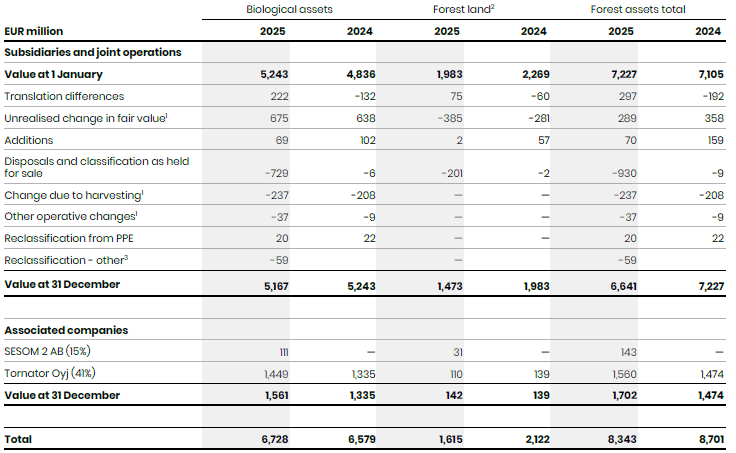

The value of forest assets disclosed in the consolidated statement of financial position from subsidiary companies and joint operations amounts to EUR 6,641 (7,227) million as shown below. The Group’s indirect share of forest assets held by associated companies amounts to EUR 1,702 (1,474) million. The total forest asset value, including leased forest land, amounts to EUR 8,478 (8,894) million.

Forest assets

1 For biological assets, changes are presented in the profit and loss. For forest land, changes in fair value are recognised directly in equity.

2 Not including leased forest land.

3 Related to Swedish forests.

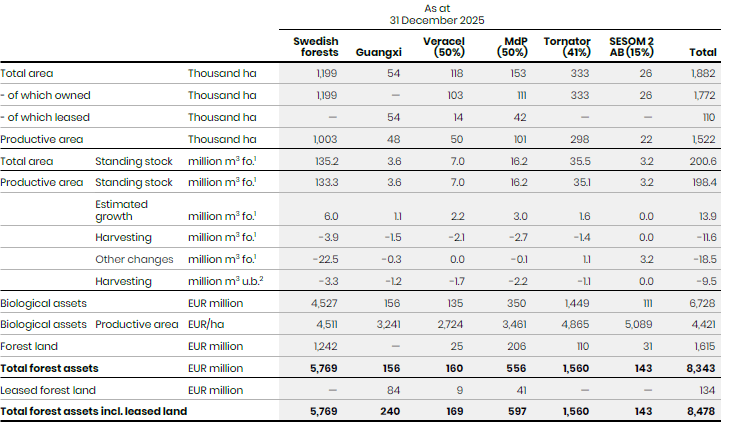

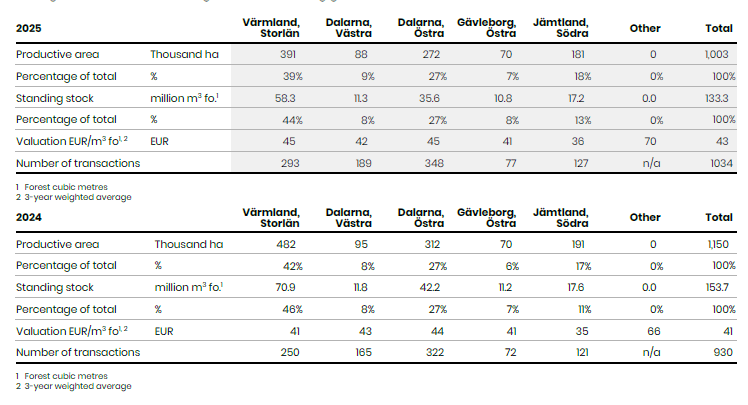

Valuation and standing stock of forest assets

1 Forest cubic meters

2 Solid under bark (sub) cubic meters

1 Forest cubic metres

2 Solid under bark (sub) cubic metres

Subsidiaries and joint operations

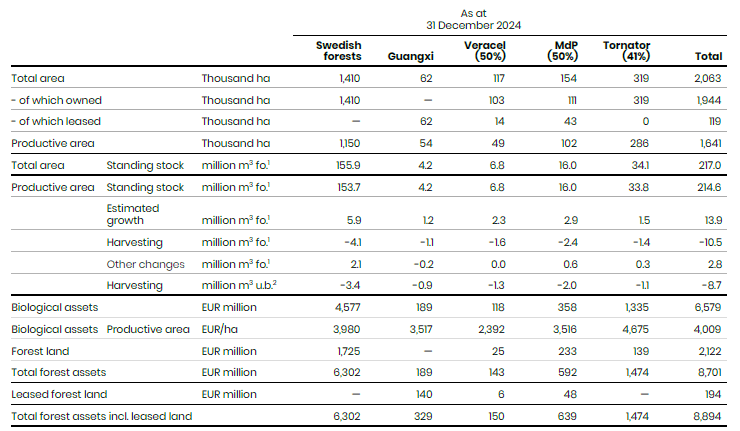

At the end of 2025, forest assets (excluding leases) were located by value, in Sweden 87% (87%), China 2% (3%), Brazil 2% (2%) and Uruguay 8% (8%). The total area amounts to 1,523 (1,744) thousand hectares of which 7% (7%) is leased and 0% (0%) is restricted. From Stora Enso’s total forest holdings 1,202 (1,355) thousand hectares constitutes productive forest area. The Montes del Plata and Veracel amounts reflect the ownership share.

Swedish forests

At the end of 2025, the value of biological assets in Swedish forests amounted to EUR 4,527 (4,577) million, related forest land amounted to EUR 1,242 (1,725) million and total forest assets amounted to EUR 5,769 (6,302) million. The decrease was mainly due to the divestment of forest assets in Sweden, while stronger foreign exchange rate and slight increase in standing stock had a positive impact on forest assets. Biological assets decreased due to the divestment, while foreign exchange rate impact and increase in long-term wood market prices had a positive impact on the value. The increased discount rate impacted the biological asset value negatively. A storm in the end of December had a negative impact on the biological assets in Sweden, due to which EUR 59 million of biological assets were moved to inventory and EUR 29 million was booked as damages to the operating result. The full extent of the damage and potential insurance compensation is still being assessed. Forest land value decreased mainly due to the divestment of forest land in Sweden and an increase in the discount rate, while foreign exchange rate had a positive impact on forest land value. Deferred tax liabilities related to forest assets amounted to EUR 1,191 (1,297) million. The discount rate of 4.5% (4.1%) was applied in the valuation.

The productive area in Swedish forests amounted to 1,003 (1,150) thousand hectares with a standing stock of 133.3 (153.7) million forest m³. The weighted three-year (36 month) average market transaction price applied in the valuation for Swedish forests assets in 2025 is EUR 43 (41) per forest m³. The forest asset value corresponds to an average of EUR 5,750 (5,480) per hectare of productive forest area.

As explained in the section Critical accounting estimates and judgement, the valuation of forest assets is based on detailed transaction data and price statistics as provided by different market data suppliers. Market transaction data is adjusted to consider the characteristics and nature of Stora Enso’s forest assets and to exclude certain non-forest assets and outliers. Main adjustments made to the transaction data in 2025 was related to outliers. The divestment of 12.4% of Stora Enso’s Swedish forest assets was not included in the market transaction data as it was not considered a pure unconditional sale of forest assets due to the related contractual agreements, further described in 6.1 Acquisitions, disposals and assets held for sale. The valuation takes into account the location of the forest land, price levels and volume of standing stock. Market prices vary significantly between areas. Future changes in the value of Swedish forest assets will be influenced by changes in market transaction prices and changes in volume of standing stock, considering growth and other factors.

Guangxi

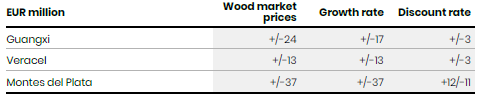

At the end of 2025, the value of the biological assets in Guangxi, China, amounted to EUR 156 (189) million. All the forest land in China is leased. The biological asset value decrease is mainly due to lower volumes as some of the lease contracts were ended in 2025, while sales prices and decrease in discount rate had a positive impact on the value. Biological assets included young standing timber with a value of EUR 21 (30) million. The discount rate of 8.8% (9.2%) used in the discounted cash flows (DCF) decreased in 2025.

Veracel

Veracel is a 50% joint operation in Brazil. Stora Enso’s share of biological assets was EUR 135 (118) million. The increase is mainly caused by favourable climate conditions effecting the growth and decreased discount rate. Biological assets included young standing timber with a value of EUR 36 (33) million. The discount rate of 8.2% (12.4%) is used in 2025. The related forest land is measured at cost.

Montes del Plata

Montes del Plata (MdP) is a 50% joint operation in Uruguay. Stora Enso’s share of biological assets was EUR 350 (358) million. The decrease is mainly driven by weaker foreign exchange rate, while increased growth and decrease in discount rate had a positive impact on the biological asset value. Biological assets included young standing timber with a value of EUR 54 (55) million. The discount rate of 8.0% (9.0%) is used in the DCF in 2025. The related forest land is measured at cost.

Associated companies

Tornator

Tornator Oyj is a 41% owned Finnish associate company. Stora Enso’s share of biological assets was EUR 1,449 (EUR 1,335) million, related forest land amounted to EUR 110 (139) million, and total forest assets equalled to EUR 1,560 (1,474) million. The increase in the value of forest assets is mainly driven by acquisitions and slightly higher market prices. Stora Enso’s share of the productive forest area totals 298 (286) thousand hectares with a standing stock of 35.1 (33.8) million forest m3. The weighted three-year (36 month) average market transaction price applied in the valuation for forest assets located in Finland in 2025 is EUR 44 (44) per forest m3. The forest asset value in Finland corresponds to an average of EUR 5,240 (5,160) per hectare of productive forest area.

SESOM 2 AB

SESOM 2 AB is a 15% owned Swedish associate company. Stora Enso’s share of biological assets was EUR 111 million, related forest land amounted to EUR 31 million and total forest assets equalled to EUR 143 million.

Stora Enso’s share of the productive forest area totals 22 thousand hectares with a standing stock of 3.2 million forest m3. The weighted three-year (36 month) average market transaction price applied in the valuation for forest assets located in Sweden in 2025 is EUR 45 per forest m3. The forest asset value in Sweden corresponds to an average of EUR 6,520 per hectare of productive forest area.

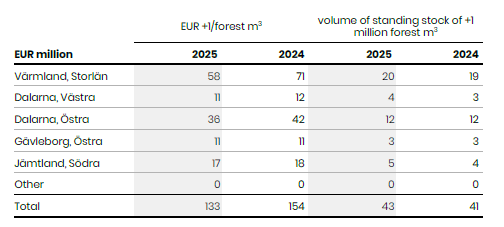

Valuation sensitivities of significant assumptions of a +/- 10% movement

Nordic forest asset valuation is sensitive to changes in market transaction prices and volume of standing stock. The table below shows the sensitivity to change in average market price and to change in the volume of standing stock of forest assets in Sweden.