Impala Platinum Holdings Limited – Annual report – 30 June 2025

Industry: mining

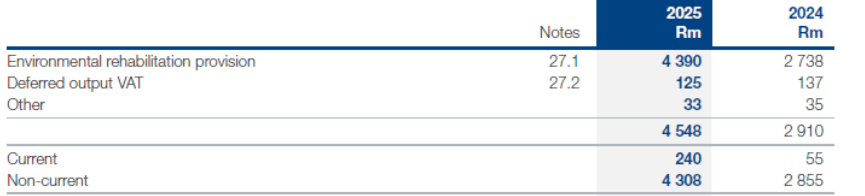

27. PROVISIONS

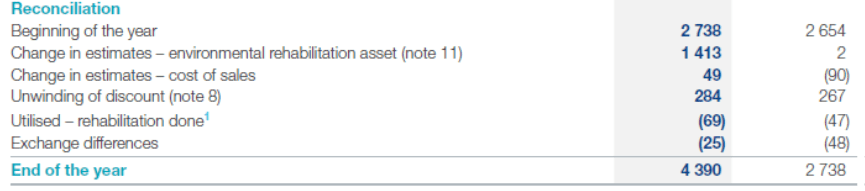

27.1 Environmental rehabilitation provision

1 Rehabilitation done mainly consists of concurrent rehabilitation at Zimplats open cast and rehabilitation at Impala Canada.

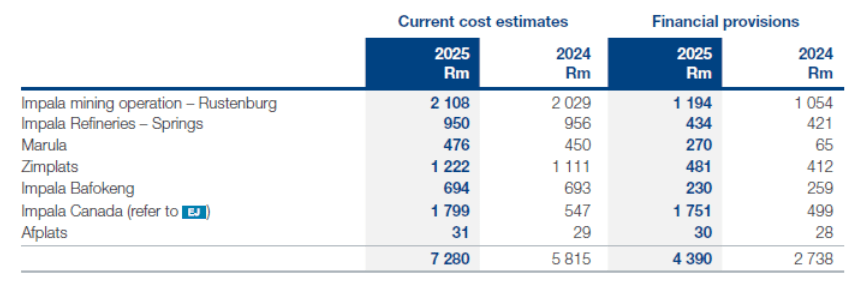

The current environmental rehabilitation cost estimates and financial provisions are made up as follows:

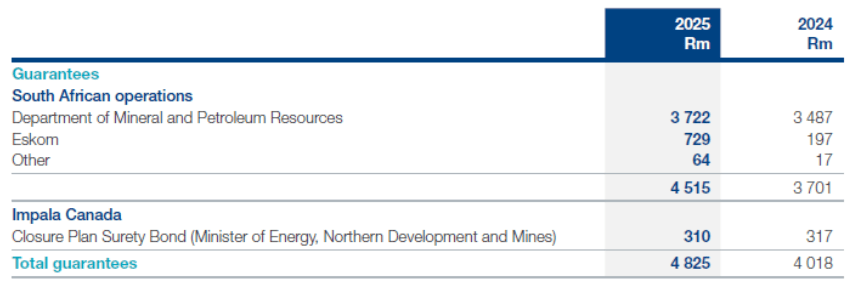

Guarantees and an insurance policy are available to the Department of Mineral and Petroleum Resources for South African mining operations to satisfy the requirements of the National Environmental Management Act with respect to environmental rehabilitation (note 34).

Estimates and judgements

Environmental rehabilitation

The Group’s mining and exploration activities are subject to various laws and regulations governing the protection of the environment. The Group recognises management’s best estimate for asset retirement obligations in the period in which they are incurred. Actual costs incurred in future periods can differ materially from the estimates. Additionally, future changes to environmental laws and regulations, LoM estimates and discount rates can affect the carrying amount of this provision. The LoM estimates are impacted by mineral reserve estimations (note 11).

In particular, from 20 November 2015, regulations governing financial provisions for asset retirement obligations in South Africa were transitioned from the Mineral and Petroleum Resources Development Act (MPRDA) to the National Environmental Management Act (NEMA). The current closure cost is closely aligned with existing regulations.

Estimated long-term environmental provisions, comprising pollution control, rehabilitation and mine closure, are based on the Group’s environmental policy taking into account current technological, environmental and regulatory requirements.

Provisions for future rehabilitation costs were determined based on calculations which require the use of estimates. The current rehabilitation cost estimate is R7 280 million (2024: R5 815 million). Cash flows relating to rehabilitation costs will occur at the end of the life of the individual mines to be rehabilitated.

South African operations

The discount rate is the long-term risk-free rate as indicated by the government bonds which ranged between 8.0% and 11.2% (2024: between 9.2% and 12.0%) at the time of calculation. The net present value of current rehabilitation estimates is based on the assumption of a long-term real discount rate of between 3.0% and 6.2% (2024: 4.2% and 7.0%).

Zimbabwean operations

The discount rate used was 7.3% (2024: 8.2%) at the time of calculation. The net present value of current rehabilitation estimates is based on the assumption of a long-term real discount rate of 5.1% (2024: 6.1%).

Canadian operations

Operating parameters at Impala Canada were adjusted in response to the deterioration in the palladium market fundamentals, as well as lower grades at Impala Canada, resulting in a further reduction of the life-of-mine of the operations from three years to one year. In response to this, management initiated a detailed review of the mine closure plan with an updated scope of closure activities and updated cost estimates. This resulted in an increase in their environmental rehabilitation provision of R1 245 million (C$96 million) which was capitalised to their environmental rehabilitation asset.

The discount rate used is the risk-free Bank of Canada bond yield (maturing in a comparable period to the mine life), plus a weighted average of inflation rates over the same period, and was 4.7% (2024: 6.0%) at the time of calculation. The net present value of current rehabilitation estimates is based on the assumption of a long-term real discount rate of 2.6% (2024: 3.9%).

27.2 Deferred output VAT

The deferred output VAT is in respect of the sale of Impala Bafokeng employee housing assets to employees which is only payable to the South African Revenue Service, in terms of section 16(4)(a)(ii) of the Value Added Tax Act No 89 of 1991, to the extent that the capital portion of the purchase price is being repaid by employees.

The deferred output VAT is initially recognised at the prevailing VAT rate of the selling price when a house is sold. When a sale is cancelled, the deferred output VAT is reversed.

Accounting policy

Provisions

Provisions are recognised when the Group has a present legal or constructive obligation as a result of past events where it is probable that an outflow of resources embodying economic benefits will be required to settle the obligation, and a reliable estimate of the amount of the obligation can be made. Provisions are not recognised for future operating losses.

Provisions are recognised as the best estimate of the expenditure required to settle the present obligation at reporting date taking into account the time value of money where relevant.

Environmental rehabilitation provision

These long-term obligations result from environmental disturbances associated with the Group’s mining operations. Estimates are determined by independent environmental specialists in accordance with environmental regulations.

Decommissioning costs

The costs arise from rectifying the damage caused before production commences. The net present value of future decommissioning cost estimates at year-end is recognised and fully provided for in the financial statements. The estimates are reviewed annually to take into account the effects of changes in the estimates. Estimated cash flows have been adjusted to reflect risks and timing specific to the rehabilitation liability. Discount rates that reflect the time value of money are used to calculate the present value.

Changes in the measurement of the liability, apart from unwinding of the discount, which is recognised in profit or loss as a finance cost, are capitalised to the environmental rehabilitation asset (note 11).

Restoration costs

These costs arise from rectifying the damage caused after production commences. The net present value of future restoration cost estimates at year-end is recognised and fully provided for in the financial statements. The estimates are reviewed annually to take into account the effects of changes in the estimates. Estimated cash flows have been adjusted to reflect risks and timing specific to the rehabilitation liability. Discount rates that reflect the time value of money are used to calculate the present value.

Changes in the measurement of the liability, apart from unwinding of the discount, which is recognised in profit or loss as a finance cost, are expensed to profit or loss.

Ongoing rehabilitation costs

The cost of the ongoing current programmes to prevent and control pollution is charged against income when they are incurred.

16. ENVIRONMENTAL REHABILITATION INVESTMENTS

16.1 Guarantee investments – Guardrisk

The investment in the insurance cell captive (Guardrisk) is intended to finance the long-term rehabilitation liabilities of the Group’s South African mining operations. These investments are measured at fair value through profit or loss. During the year, an additional R178 million, which was disinvested from Centriq Insurance Company Limited (refer to note 16.2), was invested and a R360 million (2024: R226 million) fair value gain was recognised in profit or loss.

16.2 Guarantee investments – Centriq Insurance Company Limited

In the current year, the guarantee investments were fair valued to R178 million, subsequently disposed of and reinvested in Guardrisk (refer to note 16.1). Prior to its disposal, an associated fair value gain of R8 million (2024: R5 million) was recognised in profit or loss.

The environmental guarantee investments were managed by Centriq Insurance Company Limited and were established to meet the insurance guarantees requirements of the Impala Bafokeng mining operations’ environmental liability, in which the investments served as security for the insurance guarantees issued. The investments, which primarily consisted of cash, were separately administered, and the Group’s access thereto was restricted. The environmental rehabilitation guarantee investments were measured at fair value through profit or loss.

16.3 Environmental trust deposits

The Bafokeng Rasimone Environmental Rehabilitation Trust was created in accordance with statutory requirements to fund the estimated cost of pollution control, rehabilitation and the end-of-life mine closure for the Impala Bafokeng operation. These obligations are funded by funding the trust and providing guarantees to the Department of Mineral and Petroleum Resources. The trust holds deposits in Nedbank and RMB that are carried at amortised cost. During the year, an R18 million (2024: R18 million) interest was earned and recognised in finance income.

Estimates and judgements

Financial assets measured at fair value through profit or loss

Fair value measurements reflect the view of market participants under current market conditions taking into account climate-related risks as well as geopolitical factors. Refer to note 35 for financial instrument risk disclosures.

Accounting policy

Financial assets measured at fair value through profit or loss

Financial assets that are not measured at amortised cost or at FVOCI are classified as measured at fair value through profit or loss.

11. PROPERTY, PLANT AND EQUIPMENT (extract)

The present value of decommissioning costs, which relate to dismantling and removing of the asset as a result of the environmental rehabilitation obligation, is included in the cost of the related pre- production assets. Changes in the valuation estimates of the environmental rehabilitation liability are accounted for as follows:

- Decreases in the liability reduces the cost of the related asset. The decrease in the asset is limited to its carrying amount and any excess is accounted for in profit or loss

- Increases in the liability increases the carrying amount of the related asset.

34. CONTINGENT LIABILITIES, GUARANTEES AND UNCERTAIN TAX MATTERS (extract)

The following guarantees have been issued by third parties and financial institutions on behalf of the Group to the following holders:

Guarantees to regulators (Department of Mineral and Petroleum Resources and the Minister of Energy, Northern Development and Mines) are in respect of future environmental rehabilitation liabilities for which a provision of R3 475 million (2024: R1 905 million) has been raised (note 27.1).