International Consolidated Airlines Group, S.A. – Annual report – 31 December 2025

Industry: airline

2 Significant accounting policies (extract)

Property, plant and equipment (extract)

e Leases

The Group leases various aircraft, properties, equipment and other assets. The lease terms of these assets are consistent with the determined useful economic life of similar assets within property, plant and equipment.

At inception of a contract, the Group assesses whether a contract is, or contains, a lease. A contract is, or contains, a lease if the contract conveys the right to control the use of an identified tangible asset for a period in exchange for consideration. The Group has elected not to apply such consideration where the contract relates to an intangible asset, such as for landing rights or IT software, in which case payments associated with the contract are expensed as incurred.

Leases are recognised as a lease liability and as a corresponding ROU asset at the date at which the leased asset is available for use by the Group.

Lease liabilities

Lease liabilities are initially measured at their present value, which includes the following lease payments: fixed payments (including in-substance fixed payments), less any lease incentives receivable; variable lease payments that are based on an index or a rate; amounts expected to be payable by the Group under residual value guarantees; the exercise price of a purchase option, if the Group is reasonably certain to exercise that option; payments of penalties for terminating the lease, if the lease term reflects the Group exercising that option; and payments to be made under reasonably certain extension options.

Aircraft lease payments are discounted using the interest rate implicit in the lease. The interest rate implicit in the lease is the discount rate that, at the inception of the lease, causes the aggregate present value of the minimum lease payments and the unguaranteed residual value to be equal to the fair value of the leased asset and any initial indirect costs of the lessor. For aircraft leases these inputs are either generally observable in the contract or readily available from external market data. The initial direct costs of the lessor are considered to be immaterial. If the interest rate implicit in the lease cannot be determined, the Group entity’s incremental borrowing rates are used.

Each lease payment is allocated between the principal and finance cost. The finance cost is charged to the Income statement over the lease period so as to produce a constant periodic rate of interest on the remaining balance of the lease liability for each period. After the commencement date, the amount of lease liabilities is increased to reflect the accretion of interest and reduced for the lease payments made.

The carrying amount of lease liabilities is remeasured if there is a modification of the lease contract, a reassessment of the lease term (specifically in regard to assumptions regarding extension and termination options) or changes in variable lease payments that are based on an index or a rate.

Right-of-use assets

At the lease commencement date, an ROU asset is measured at cost comprising the following: the amount of the initial measurement of the lease liability; any lease payments made at or before the commencement date less any lease incentives received; and any initial direct costs.

In addition, at the lease commencement date, the ROU asset will incorporate those restoration and handback costs that are considered unavoidable, such as the removal of airline-specific branding and configuration, to return the asset to its original condition, for which a corresponding amount is recognised within Provisions. The ROU asset is depreciated over the shorter of the asset’s useful life and the lease term on a straight-line basis. If ownership of the ROU asset transfers to the Group at the end of the lease term or the cost reflects the exercise of a purchase option, depreciation is calculated using the estimated useful life of the asset.

Amounts excluded from recognition as ROU assets and lease liabilities

The Group has elected not to recognise ROU assets and lease liabilities for short-term leases that have a lease term of 12 months or less (and where that short-term lease is not expected to be renewed) and leases of low-value assets. Short-term leases are leases with a lease term of 12 months or less that do not contain a purchase option. Low-value assets comprise specific IT equipment and office furniture. Payments associated with short-term leases and leases of low-value assets are recognised on a straight-line basis as an expense in the Income statement.

The Group is exposed to potential future increases in variable lease payments based on an index or rate which are not included in the lease liability until they take effect. When adjustments to lease payments based on an index or rate take effect, the lease liability is reassessed and adjusted against the ROU asset. Such variable lease payments are expensed to the Income statement as incurred.

Extension options are included in a number of aircraft, property and equipment leases across the Group and are reflected in the lease liability where the Group is reasonably certain that it will exercise the option.

Sale and leaseback transactions

The Group regularly uses sale and leaseback transactions to finance the acquisition of aircraft. Each transaction is assessed as to whether it meets the criteria within IFRS 15 ‘Revenue from contracts with customers’ for a sale to have occurred. The principal criterion for assessing whether a sale has occurred or not is whether the contract contains the option, at the discretion of the Group, to repurchase the aircraft during or at the end of the lease term. If such a repurchase option exists in the contract, irrespective of whether the Group intends to exercise the option or not, the sale is deemed not to have occurred. Where there is no repurchase option in such a transaction, then a sale is deemed to have occurred. The following defines the accounting for such transactions:

- If a sale is determined to have occurred, then the associated asset is de-recognised and an ROU asset and lease liability are recognised. The ROU asset recognised is based on the proportion of the previous carrying amount of the asset that is retained. Any gain or loss is restricted to the amount that relates to the rights that have been transferred to the counterparty to the transaction; and

- Where a sale is determined to have not occurred, the asset is retained on the Balance sheet within Property, plant and equipment and an Asset financed liability recognised equal to the financing proceeds.

Cash flow presentation – lease liabilities

Payments associated with lease liabilities are presented as follows in the Consolidated cash flow statement:

- Where the proceeds received from sale and leaseback transactions represent the fair value of the asset being transferred, the total proceeds are presented within cash flows from investing activities. Where the proceeds received from sale and leaseback transactions exceed the fair value of the asset being transferred, the element of the proceeds equivalent to the fair value of the asset being transferred is presented within investing activities and the amount of proceeds in excess of the fair value is presented within financing activities;

- The repayments of the principal element of lease liabilities are presented within cash flows from financing activities;

- The payments of the interest element of lease liabilities are included within cash flows from operating activities;

- The payments arising from variable elements of a lease, short-term leases and low-value assets are presented within cash flows from operating activities; and

- The non-cash gain or loss arising from sale and leaseback transactions is presented within cash flows from operating activities.

Cash flow presentation – asset financed liabilities

Payments associated with asset financed liabilities are presented as follows in the Consolidated cash flow statement:

- The proceeds received from asset financed liabilities are presented within cash flows from financing activities;

- The repayments of the principal element of asset financed liabilities are presented within cash flows from financing activities; and

- The payments of the interest element of asset financed liabilities are included within cash flows from operating activities.

Lessor accounting

From time to time the Group will lease, to third parties, specific assets, including certain property, plant and equipment. On inception of the lease, the Group determines whether each lease is a finance lease or an operating lease.

In order to make this determination, the Group assesses whether the lease transfers substantially all of the risks and rewards of ownership to the lessee. Factors in making this assessment include, but are not limited to, whether the lease term is for the major part of the economic life of the underlying asset and whether the underlying asset transfers to the lessee or the lessee has the option to purchase the underlying asset at the end of the lease. Where substantially all of the risks and rewards of ownership have been transferred, then the lease is recorded as a finance lease; otherwise it is recorded as an operating lease.

f Maintenance, repairs and overhaul

Owned aircraft

Major maintenance, repairs and overhaul expenditure, including replacement spares and labour costs for airframes and engines, is capitalised and amortised over the expected life between major maintenance, repair and overhaul events or to the end of the useful life of the asset. When each major event is performed, the associated cost is recognised in the carrying amount of the item of property, plant and equipment as a replacement asset and any remaining carrying amount of the cost of the previous maintenance event is de-recognised.

On initial recognition of an aircraft, a component of such costs is attributed to the embedded heavy maintenance component of the assets, such as the engines. The embedded heavy maintenance component is depreciated over the period to the next major maintenance event.

All other replacement spares and other costs relating to maintenance of owned fleet assets are charged to the Income statement on consumption or as incurred, respectively, recognised within Engineering and other aircraft costs.

Leased aircraft

Under each lease agreement, the Group is contractually committed to either return the airframe, engines and certain other assets in a specified condition or to compensate the lessor based on the conditionality of the aforementioned assets at the point of return to the lessor.

Accordingly, the Group records a provision for major maintenance, repair and overhaul events, including for airframes and engines, that occur through usage or through the passage of time, which is recognised as such activity occurs through to the next such maintenance event. A corresponding expense is recorded in the Income statement within Engineering and other aircraft costs over the relevant period as the provision is accumulated. Any subsequent changes in estimation are recognised in the Income statement. When the maintenance, repair or overhaul event occurs, the associated provision is de-recognised.

Restoration and handback obligations that arise on the inception of the lease, and that are not dependent on the usage of the asset or on the passage of time, are recognised as a provision for the full expected cost of discharging those obligations with a corresponding amount recognised as a separate component of the ROU asset. The associated ROU asset is depreciated over the lease term. Any subsequent change in estimation relating to such costs is reflected in both the provision and the ROU asset, with the adjustment to the ROU asset depreciated over the remaining lease term.

All other replacement spares and other costs relating to maintenance of leased fleet assets are charged to the Income statement on consumption or as incurred, respectively, within Engineering and other aircraft costs.

Power by the hour contracts

Certain of the Group’s maintenance contracts, for both owned and leased aircraft, transfer the risk and legal obligation for undertaking the maintenance activity to third-party service providers, with the Group paying the service providers based on usage of the asset. The associated usage of the asset gives rise to a charge, as flight hours are incurred and dependent on the number of take offs and landings, in the Income statement within Engineering and other aircraft costs.

Critical accounting estimates, assumptions and judgements (extract)

The preparation of financial statements requires management to make judgements, estimates and assumptions that affect the application of policies and reported amounts of assets and liabilities, income and expenses. These judgements, estimates and associated assumptions are based on historical experience and various other factors believed to be reasonable under the circumstances. Actual results in the future may differ from judgements and estimates upon which financial information has been prepared. These underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognised prospectively.

The estimates and assumptions that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are as follows:

- Revenue recognition (note 24): breakage assumptions applied to passenger revenue, customer loyalty programmes and unredeemed vouchers;

- Restoration and handback provisions (note 27): key assumptions underlying the carrying value of the provisions; and

- Employee benefit obligations (note 34): Airways Pension Scheme (APS) and New Airways Pension Scheme (NAPS) key actuarial assumptions.

The judgements that have a significant risk of causing a material adjustment to the carrying amounts of assets and liabilities within the next financial year are as follows:

- Income taxes (note 10): determining whether payments made to HMRC in relation to the IAG Loyalty VAT accounting are recoverable;

- Leases (note 14): determining the lease term of contracts with renewal and termination options; and

- Restoration and handback provisions (note 27): determination of accounting policy for leased aircraft.

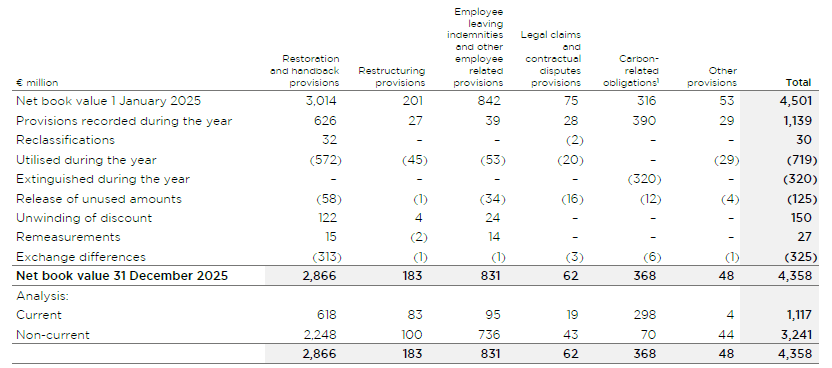

27 Provisions (extract)

Significant accounting estimate applied – Restoration and handback provisions: key assumptions underlying the carrying value of the provisions

At 31 December 2025, the Group recognised €2,866 million in respect of maintenance, restoration and handback provisions, principally in respect of leased aircraft (31 December 2024: €3,014 million).

The Group has a number of contracts with service providers to replace or repair engine parts and for other maintenance checks. These agreements are complex and generally cover a number of years. Provisions for maintenance, restoration and handback are made based on the best estimate of the likely committed cash outflow. In determining this best estimate, the Group applies significant judgement as to the level of forecast costs expected to be incurred when the major maintenance event occurs. Other assumptions not considered to be significant include aircraft utilisation, expected maintenance intervals and the aircraft’s condition. The associated forecast costs are discounted to their present value. While the Group considers that there are no reasonably possible changes to any of the individual assumptions that would have a material impact on the provisions, a combination of changes in several assumptions may. The Group considers that a reasonably possible change in the inflation rate and discount rate assumptions of a 100 basis point increase would give rise to an increase of €85 million (2024: €62 million) and a decrease of €77 million (2024: €70 million), respectively, in the provisions balance when applied in isolation to one another.

Significant accounting judgement applied – Restoration and handback provisions: determination of accounting policy for leased aircraft

IFRS 16 does not address the accounting for maintenance, restoration and handback provisions that arise through the usage of the underlying asset and, accordingly, the Group has applied judgement in applying an accounting policy with regard to the recognition and subsequent measurement of such provisions for leased aircraft. The Group’s accounting policy for provisions that arise through usage or through the passage of time is to recognise the associated estimated costs in the Income statement as the underlying asset is used or through the passage of time. The approach applied by the Group is consistent with the majority of major airlines that prepare their financial statements under IFRS. Were the Group to apply an alternative accounting policy, the financial impact would be materially different at the balance sheet date. An alternative accounting policy that the Group could have applied was the components approach, where the Group would capitalise the estimated costs of major maintenance events and depreciate them until the subsequent maintenance event (or to the end of lease term) and providing over the lease term for any expected cash compensation for maintenance obligations at the end of the lease. The Group considers that the current accounting policy for maintenance, restoration and handback activities reflects the obligations under its lease arrangements.

1 The disaggregation of Carbon-related obligations by underlying scheme is presented in note 4f.

Restoration and handback provisions

Provisions for restoration and handback costs are recognised to meet the contractual major maintenance and return conditions on aircraft held under lease. For those obligations arising on inception of an aircraft lease, the associated estimated cost is capitalised within the ROU asset. For those obligations that arise through usage or through the passage of time, the associated estimated costs are recognised in the Income statement as the associated asset is used or through the passage of time. The provision is long-term in nature.

The provisions also include an amount relating to leased land and buildings where restoration costs are contractually required at the end of the lease. Such costs are capitalised within ROU assets.

The provisions are determined by discounting the future cash flows using pre-tax risk-free rates specific to the tenor of the provision and the currency in which it arises. The unwinding of the discounting of the provisions is recorded as a Finance cost in the Income statement (see note 9a).

Remeasurements arising from changes in estimates relating to the effects of both discounting and inflation are recorded in the Income statement to the extent they relate to avoidable provisions or are recorded as an adjustment to the ROU asset (see note 14) for those unavoidable provisions.

Where amounts are finalised and the uncertainty relating to these provisions removed, the associated liability is reclassified to either current or non-current Other creditors, dependent on the expected timing of settlement.

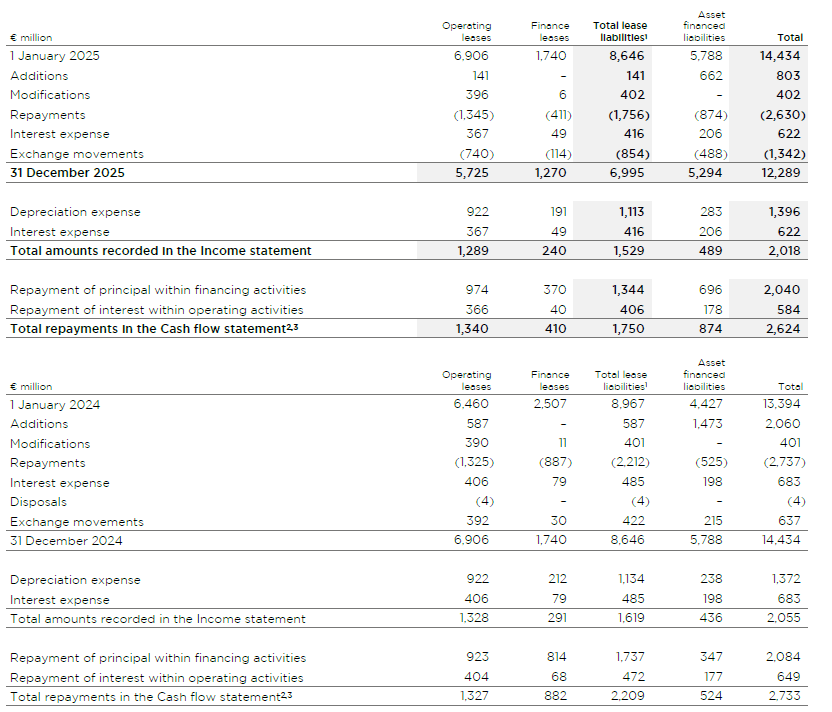

14 Leases (extract)

Significant accounting judgement applied – Determining the lease term of contracts with renewal and termination options

The Group determines the lease term as the non-cancellable term of the lease, together with any periods covered by an option to extend the lease if it is reasonably certain to be exercised, or any periods covered by an option to terminate the lease, if it is reasonably certain not to be exercised. The Group applies judgement in evaluating whether it is reasonably certain whether or not to exercise the option to renew or terminate the lease. Such judgement includes consideration of fleet plans, which underpin approved business plans and historical experience regarding the extension of leases. After the commencement date, the Group reassesses the lease term if there is a significant event or change in circumstances that affects the Group’s ability to exercise or not to exercise the option to renew or to terminate.

a Amounts recognised in the Balance sheet – right-of-use assets

Property, plant and equipment includes the following amounts relating to right-of-use assets:

1 Amounts with a net book value of €228 million (2024: €604 million) were reclassified from ROU assets to owned Property, plant and equipment at the cessation of the respective leases. The assets reclassified relate to leases with purchase options that were grandfathered as ROU assets upon transition to IFRS 16, for which the Group had been depreciating over the expected useful life of the aircraft, incorporating the purchase option.

b Amounts recognised in the Balance sheet – lease liabilities and asset financed liabilities

The following table provides supplemental information regarding the Group’s total contractual lease obligations, split between operating and finance leases that are reported within Lease liabilities and those contractual lease arrangements reported as Asset financed liabilities that do not meet the definition of a lease liability under IFRS. While the distinction between operating and finance leases is not applied for lessees under IFRS, the table below disaggregates operating and financing leases based on their contractual definitions and is consistent with the definitions applied for lessors under IFRS. The Group believes that this disaggregation of Lease liabilities is useful to the users of the financial statements in understanding the financing structure the Group has entered into.

1 Upon transition to IFRS 16 on 1 January 2019, all finance leases were grandfathered as lease liabilities.

2 Includes the repayment of both principal and interest.

3 Excludes cash flows associated with low-value leases and variable lease payments, which the Group does not recognise within lease liabilities.

Interest-bearing long-term borrowings include the following amount relating to lease liabilities:

c Amounts recognised in the Income statement

d Amounts recognised in the Cash flow statement

The following table details the amounts recognised in the Cash flow statement for the years to 31 December 2025 and 31 December 2024.

The Group is exposed to future cash outflows (on an undiscounted basis) at 31 December 2025, for which an amount of €nil (2024: €89 million) has been recognised in relation to leases not yet commenced to which the Group is committed.

e Maturity profile of lease liabilities and asset financed liabilities

The following table analyses the Group’s outflows in respect of operating leases, finance leases and asset financed liabilities into relevant maturity groupings based on the remaining period at 31 December to the contractual maturity date. The amounts disclosed in the table are the contractual undiscounted cash flows and include interest.

f Extension options

The Group has certain leases that contain extension options exercisable by the Group prior to the non-cancellable contract period. Where practicable, the Group seeks to include extension options in new leases to provide operational flexibility. The Group assesses at lease commencement whether it is reasonably certain to exercise the extension options.

The Group is exposed to future cash outflows (on an undiscounted basis) at 31 December 2025, for which no amount has been recognised, for potential extension options of €1,068 million (2024: €1,115 million) due to it not being reasonably certain that these leases will be extended.

29 Financial risk management objectives and policies (extract)

f Liquidity risk (extract)

The following table analyses the Group’s (outflows) and inflows in respect of financial liabilities and derivative financial instruments into relevant maturity groupings based on the remaining period at 31 December to the contractual maturity date. The amounts disclosed in the table are the contractual undiscounted cash flows and include interest.