China Yuchai International Limited – Annual report – 31 December 2024

Industry: manufacturing

2.5. Summary of material accounting policies (extract)

(d) Revenue from Contracts with Customers (extract)

Warranty obligations

The Group typically provides warranties for general repairs of defects as part of the sale of engines. These assurance-type warranties are accounted for as warranty provisions. Refer to the accounting policy on warranty provisions in Section (m) Provisions.

Certain contracts provide a customer with maintenance service, i.e. a distinct service to the customer in addition to the assurance that the product complies with agreed-upon specification. These service-type warranties are bundled together with the sale of engines. These contracts comprise two performance obligations, i.e. the promises to transfer the engines and to provide the service-type warranty. The transaction price is allocated to the service-type warranty and engines using a combination of residual and observable price approach. The portion of transaction price allocated to the service-type warranty is initially recorded as a contract liability and recognized as revenue at the point in time when the service is provided.

(m) Provisions (extract)

Product warranty

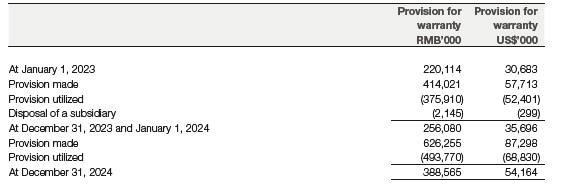

The Group recognizes a liability at the time the product is sold, for the estimated future costs relating to the assurance-type warranties, to be incurred under the lower of a warranty period or warranty mileage on various engine models, on which the Group provides free repair and replacement. Provisions for warranty are primarily determined based on historical warranty cost per unit of engines sold adjusted for specific conditions that may arise and the number of engines under warranty at each financial year. If the nature, frequency and average cost of warranty claims change, the accrued liability for product warranty will be adjusted accordingly.

6. REVENUE FROM CONTRACTS WITH CUSTOMERS (extract)

6.2. Contract balances

The contract liabilities comprise short-term advance received from customers and unfulfilled service-type maintenance service. The advance received from customers is recognized as revenue upon the delivery of goods, and the contract liability arising from unfulfilled service-type warranty is recognized upon the completion of the maintenance services. According to the business customary practice, the remaining performance obligations (unfulfilled service-type maintenance service) at the year-end is expected to be satisfied within 2 years.

(a) Set out below is the amount of revenue recognized from:

6.3. Performance obligations (extract)

The transaction price allocated to the remaining unsatisfied performance obligations as of 31 December are, as follows:

24. CONTRACT LIABILITIES

23. PROVISIONS