Co-operative Group Limited – Annual report – 4 January 2025

Industry: retail, financial

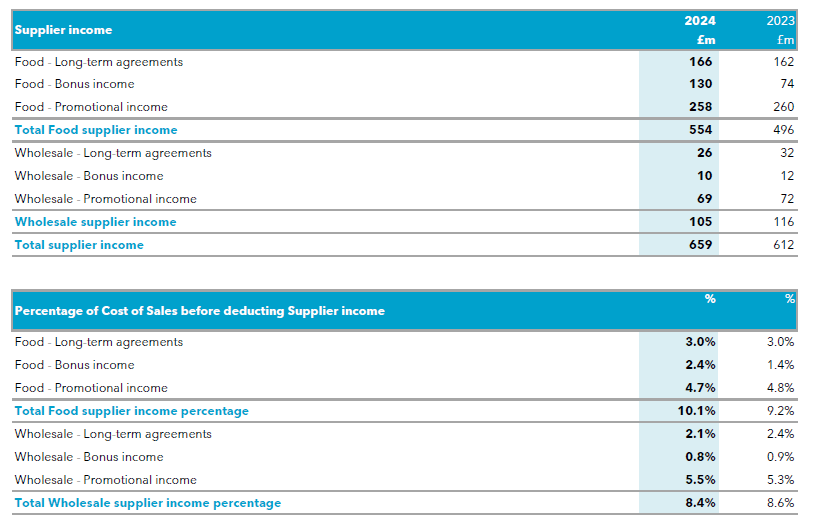

4 Supplier income

All figures exclude any income or purchases made as part of the Federal joint buying group (as supplier income is passed on to Federal (FRTS) members in the same proportion as the ratio to their cost of sales).

Accounting policies

Supplier income

Supplier income is recognised as a deduction from cost of sales on an accruals basis, based on the expected entitlement that has been earned up to the balance sheet date for each relevant supplier contract. Where amounts received are in the expectation of future business, these are recognised in the income statement in line with that future business.

The Group has a mixture of contractual terms with its suppliers. Where our trading terms state that the supplier income is netted against amounts owing to that supplier and it is our intention to settle the balances on a net basis then any outstanding invoiced supplier income at the reporting date is included within trade payables (Note 19). Any amounts received in advance of income being recognised are included in accruals and deferred income (Note 19). When we do not have the right of offset (or we do not intend to settle on a net basis) then the Group classifies outstanding supplier income within trade receivables (Note 15). Where the supplier income is earned but not yet invoiced to the supplier at the reporting date, this is classified within accrued income (Note 15).

There are three main types of income:

1. Long-term agreements: These refer to supplier income rebates based on the value of purchases Co-op places with its suppliers. Typically, these are annual % rebate agreements applied to the purchases Co-op makes from its suppliers. Income is only recognised once the rebate agreement is in place with the supplier.

2. Bonus income: These are typically unique payments made by the supplier and are not based on volume. They include payments for marketing support, range promotion and product development. These amounts are recognised when the income is earned and confirmed by suppliers. An element of the income is deferred if it relates to a future period.

3. Promotional income: Rebates based on sales volumes relating to agreed promotional activity. These are retrospective rebates based on sales volumes.

The inventory balance is stated net of any supplier income value on goods not sold at year-end.

16 Trade and other receivables (extract)

Within trade receivables is £48m (2023: £84m) of supplier income that is due from Food and Wholesale suppliers. Accrued income includes £131m (2023: £96m) in relation to supplier income that has been recognised but not yet billed. As at 1st March 2025 (reflecting the close of Period 2 for the Group), £44m (2023: £77m) of the trade receivables balance had been invoiced and settled and £108m (2023: £87m) of the accrued income balance has been invoiced and settled.

19 Trade and other payables (extract)

Where our trading terms state that the supplier income is netted against amounts owing to that supplier and it is our intention to settle the balances on a net basis then any outstanding invoiced supplier income at the reporting date is included within trade payables. Trade payables includes £33m (2023: £29m) of supplier income receivable that has been offset against amounts owed to those suppliers.