Mercedes-Benz Group AG – Annual report – 31 December 2023

Industry: automotive

32. Financial instruments (extract)

Net gains or losses

The following table shows the net gains/losses on financial instruments included in the Consolidated Statement of Income (excluding derivative financial instruments used in hedge accounting).

Net gains/losses on equity and debt instruments recognized at fair value through profit or loss primarily comprise gains and losses attributable to changes in the fair values of these instruments.

Net gains/losses on other financial assets and liabilities recognized at fair value through profit or loss comprise gains and losses attributable to changes in their fair values.

Net gains/losses on equity instruments recognized at fair value through other comprehensive income comprise dividend payments.

Net gains/losses on other financial assets recognized at fair value through other comprehensive income are primarily attributable to exchange-rate effects.

Net gains/losses on financial assets measured at (amortized) cost (excluding the interest income/expense shown below) primarily comprise impairment losses (including reversals of impairment losses) of minus €406 million (2022: minus €610 million) that are charged to cost of sales, selling expenses and other financial income/expense, net. Foreign currency gains and losses are also included.

Net gains/losses on financial liabilities measured at (amortized) cost (excluding the interest income/expense shown below) primarily comprise exchange-rate effects.

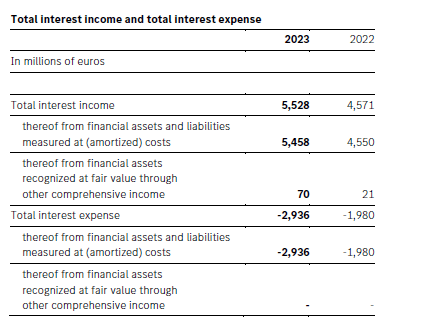

Total interest income and total interest expense

Total interest income and total interest expense for financial assets or financial liabilities that are not recognized at fair value through profit or loss are shown in the following table.

Information on derivative financial instruments

Use of derivatives

The Mercedes-Benz Group uses derivative financial instruments exclusively for hedging financial risks that arise from its operating or refinancing activities or from its liquidity management. These are mainly currency risks; interest rate risks and commodity price risks, which have been defined as risk categories. For these hedging purposes, the Group mainly uses currency forward transactions, cross-currency interest rate swaps, interest rate swaps, options and commodity forwards.

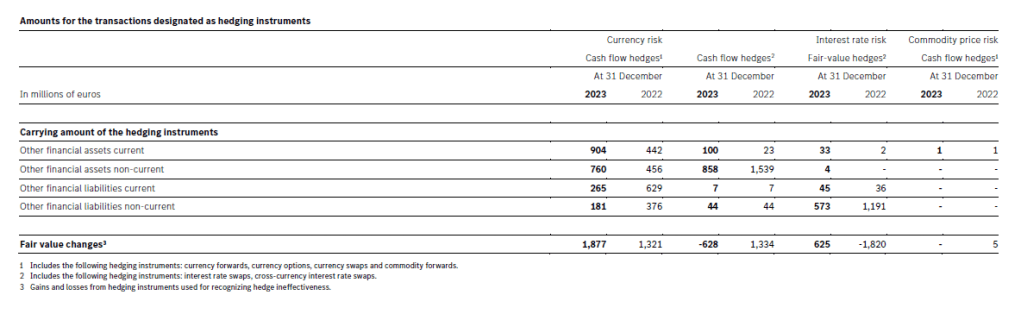

The following table shows the amounts for the transactions designated as hedging instruments.

Most of the transactions for which the effects from the measurement of the hedging instrument and the underlying transaction to a large extent offset each other in the Consolidated Statement of Income were mostly not included in the hedge accounting.

Even if derivative financial instruments do not or no longer qualify for hedge accounting, these instruments still serve to hedge financial risks from business operations. A hedging instrument is terminated when the hedged transaction no longer exists or is no longer expected to occur.

Explanations of the hedging of exchange-rate risks, interest rate risks and commodity price risks can be found in Note 33 in the sub-item Finance market risk.

Cash flow hedges and hedges of net investments in foreign operations

The Mercedes-Benz Group uses cash flow hedges for hedging currency risks, interest rate risks and commodity price risks. The amounts related to items designated as cash flow hedges are shown in the following table. The Group also partially hedges the currency risk of selected investments with the application of derivative or non-derivative financial instruments. Neither in the reporting year nor in the previous year were there any active hedges of net investments in foreign operations.

The gains and losses on items designated as cash flow hedges are shown in the following table.

Expenses of €2 million (2022: income of €2 million) were attributable to the hedge ineffective portion of the hedges.

During 2022, shifts in delivery dates and volumes occurred in various markets, making some planned vehicle sales in specific currencies unlikely, with the consequence that hedge accounting for these sales had to be terminated.

This particularly affected the currency CNY as a consequence of the Covid-19 pandemic. The reclassification from the reserves for derivative financial instruments to the Consolidated Statement of Income did not result in any material effects.

Fair-value hedges

The Group uses fair-value hedges primarily for hedging interest rate risks. The amounts of the items hedged with fair-value hedges are included in the following table.

Neither in the current year nor in the previous year were there any results attributable to the ineffective portion of the hedge with fair-value hedges.

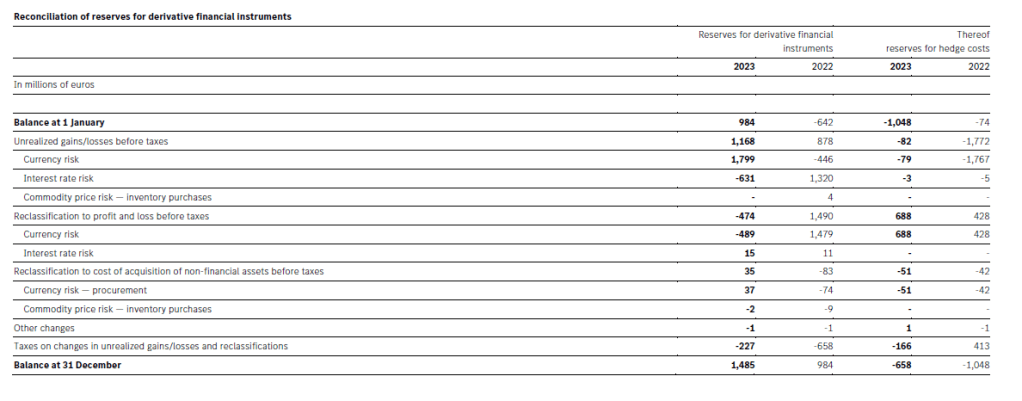

Reserves for derivative financial instruments

The following table shows the reconciliation of the reserves for derivative financial instruments (excluding reserves for hedges of net investments in foreign operations).

At 31 December 2023, the balance of reserves for hedges of net investments in foreign operations amounted to €189 million (2022: €189 million).

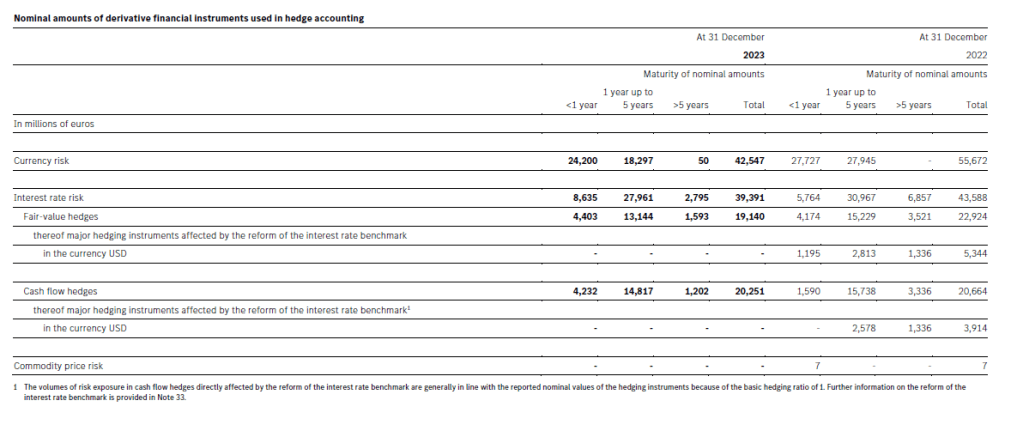

Nominal values of derivative financial instruments used in hedge accounting

At 31 December 2023, the Mercedes-Benz Group utilized derivative financial instruments with a maximum maturity of 71 and 115 months, respectively, (2022: 57 and 127 months) as hedges for currency risks and interest rate risks.

The following table shows the nominal values of derivative financial instruments used in hedge accounting entered into for the purpose of hedging currency risks, interest rate risks and commodity price risks that arise from the Group’s operating and/or financing activities.

The maturities of the derivative financial instruments generally correspond with those of the underlying transactions. The realization of the underlying transactions is expected to correspond with the maturities of the hedging transactions shown in the following table.

Average prices of hedging instruments

The following table shows the average prices of hedging instruments by risk category for the major risks.

33. Management of financial risks (extract)

Country risk

Country risk is the risk of economic loss arising from changes of political, economic, legal or social conditions in the respective country, e.g. resulting from sovereign measures such as expropriation or interdiction of foreign currency transfers.

The Mercedes-Benz Group is exposed to country risk mainly resulting from cross-border funding or collateralization of Group companies and customers, from investments in Group companies, associated companies, joint ventures and joint operations as well as from cross-border trade receivables. Country risks also arise from cross-border cash deposits at financial institutions.

The Mercedes-Benz Group manages these risks via country exposure limits (e.g. for hard currency portfolios of financial services entities). An internal rating system serves as a basis for the Mercedes-Benz Group’s risk-oriented country exposure management; it assigns all countries to risk classes, with consideration of both external ratings and capital market indications of country risks.

Finance-market risks

The global nature of its businesses exposes the Mercedes-Benz Group to significant market risks resulting from fluctuations in foreign currency exchange-rates and interest rates as well as commodity and energy prices. The Group is also exposed to equity price risk in connection with its investments in listed companies.

The Mercedes-Benz Group manages market risks to minimize the impact of fluctuations in foreign exchange-rates and interest rates on the earnings of the Group and its segments. The Group calculates its overall net-exposure to these market risks to provide the basis for hedging decisions, which include the selection of hedging instruments and the determination of hedging volumes and the corresponding periods. The hedging strategy is specified at Group level and uniformly implemented in the segments. Decisions regarding, for example, currencies and asset-liability management (interest rates) are made by a committee that meets regularly. Net-exposures are the basis for the hedging strategies and are updated regularly. The Mercedes-Benz Group usually counteracts the risk of short-term fluctuations in raw-material prices by means of price escalation clauses in the supply contracts. Power purchase agreements are also concluded to reduce electricity price risks. Power purchase agreements are purchase agreements for energy needs, including fixed purchase prices of the electricity generated by a specific plant for generating wind or solar power.

Certain existing benchmark interest rates including those of the London Interbank Offered Rate (for USD, GBP, CHF and JPY) were comprehensively and internationally reformed. As a result, those interest rates were gradually abolished and replaced with alternative risk-free reference rates. Alternative interest rates were developed on a national level in the context of the respective legal systems and currencies; they can therefore vary with regard to their structure, methodology and period of publication.

As the reform for EURIBOR and USD, GBP, CHF and JPY LIBOR has already been implemented, the contractual adjustment of financial instruments has already been made in line with a corresponding interest rate reference.

The conversion of the outstanding reference rates of hedging instruments and their underlying transactions was identical and without any material delay. The Mercedes-Benz Group considered the economic relationship and thus the continuation of hedge accounting to be still existing as of 31 December 2022.

The nominal values of those hedging instruments that were affected in the prior year and are included in a hedging relationship can be found in table Nominal amounts of derivative financial instruments used in hedge accounting in Note 32.

The effect of the application of the new interest rates on the Consolidated Financial Statements is being reviewed on an ongoing basis. In order to conduct financial transactions based on the new indices, the Mercedes-Benz Group is preparing its relevant IT-systems accordingly. Uncertainty still exists about future market standards with interest conventions for individual financial products (cash products and interest derivatives) that reference the new risk-free rates. Contracts not yet converted as part of the IBOR reform in the previous year (USD LIBOR) amounted to €4,790 million in financial liabilities and €9,258 million in derivatives as of 31 December 2022.

As part of its risk management system, the Mercedes-Benz Group employs value-at-risk analyses. In performing these analyses, the Mercedes-Benz Group quantifies its market risk due to changes in foreign currency exchange-rates and interest rates and certain commodity prices on a regular basis by predicting the potential loss over a target time horizon (holding period) and confidence level.

The value-at-risk calculations employed:

– Express potential losses in fair values, and

– assume a 99% confidence level and a holding period of five days.

At the Group level, the Mercedes-Benz Group calculates the value at risk for exchange-rate and interest rate risk according to the variance-covariance approach. The value-at-risk calculation method for commodity hedging instruments is based on a Monte Carlo simulation.

When calculating value at risk using the variance-covariance approach, the Mercedes-Benz Group first computes the current market value of the Group’s financial instruments portfolio. Then the sensitivity of the portfolio value to changes in the relevant market risk factors, such as particular foreign currency exchange-rates or interest rates of specific maturities, is quantified. Based on volatilities and correlations of these market risk factors, which are obtained from the RiskMetrics™ dataset, a statistical distribution of potential changes in the portfolio value at the end of the holding period is computed. The loss which is reached or exceeded with a probability of only 1% can be derived from this calculation and represents the value at risk.

The Monte Carlo simulation uses random numbers to generate possible changes in market risk factors consistent with current market volatilities. The changes in market risk factors allow the calculation of a possible change in the portfolio value over the holding period. Running multiple iterations of this simulation leads to a distribution of portfolio value changes. The value at risk can be determined based on this distribution as the portfolio value loss which is reached or exceeded with a probability of 1%.

Exchange-rate risk

Transaction risk and currency risk management

The global nature of the Mercedes-Benz Group’s businesses exposes cash flows to risks arising from fluctuations in exchange-rates. These risks primarily relate to fluctuations between the euro and the US dollar, the Chinese renminbi, the British pound and other currencies such as currencies of growth markets. In the operating vehicle business, the Group’s exchange-rate risk primarily arises when revenue is generated in a currency that is different from the currency in which the costs of revenue are incurred (transaction risk). It may be inadequate to cover the costs if the value of the currency in which the revenue is generated declined in the interim relative to the value of the currency in which the costs were incurred. The risk exposures serve as a basis for analysing exchange-rate risks at Group level.

In addition, the Group is indirectly exposed to a transaction risk from its equity-method investments.

The Group’s overall currency exposure is reduced by natural hedging, which consists of the currency exposures of the business operations of different entities and segments partially offsetting each other at Group level. These natural hedges eliminate the need for hedging to the extent of the matched exposures. To provide an additional natural hedge against any remaining transaction risk exposure, the Mercedes-Benz Group generally strives to increase cash outflows in the same currencies in which the Group has a net excess inflow.

In order to mitigate the impact of currency exchange-rate fluctuations for the business operations (future transactions), the Mercedes-Benz Group continually assesses its exposure to exchange-rate risks and hedges a portion of those risks by using derivative financial instruments. A committee manages the Group’s exchange-rate risk and its hedging transactions through currency derivatives. The committee consists of representatives of the relevant segments and corporate functions. The Corporate Treasury department aggregates foreign currency exposures from the companies of the Group and the operational units and implements the committee’s decisions concerning foreign currency hedging through transactions with international financial institutions. Suitable measures are generally taken without delay to eliminate any over-hedging regarding hedging transactions caused by changes in exposure. Moreover, designated hedging relationships are reviewed with respect to any requirements to discontinue hedge accounting.

The Group’s targeted hedge ratios for forecast operating cash flows in foreign currencies are generally determined using a step-by-step method. Depending on the nature of the underlying risks, the hedging rates decrease the further the expected cash flows are in the future. On the one hand, the hedging horizon is naturally limited by uncertainty related to cash flows that lie far in the future; on the other hand, it may also be limited by the fact that appropriate currency contracts are not available. This step-by-step method aims to limit risks for the Group from unfavourable movements in exchange-rates while preserving sufficient flexibility to participate in favourable developments. Based on this step-by-step method and depending on the market outlook, the committee determines the hedging horizon, which usually varies from one to five years, as well as the average hedge ratios. At the end of 2023, the currency management for calendar year 2024 showed an unhedged position in the automotive business of 35% of the underlying forecasted cash flows in US dollars and an unhedged position of 29% of the underlying forecast cash flows in British pounds, while the forecast cash flows in Chinese renminbi were almost fully hedged with an unhedged position of 4%.

To cover foreign currency exposure risks of the vehicle business operations forward foreign exchange contracts and currency options are primarily used. The Mercedes-Benz Group’s policies call for a mixture of these financial instruments depending on the assessment of market conditions. Value at risk is used to measure the exchange-rate risk inherent in these derivative financial instruments.

The following table shows the period-end, high, low and average value-at-risk figures of the exchange-rate risks for the 2023 and 2022 portfolios of derivative financial instruments, which were entered into primarily in connection with the vehicle business operations and the trade receivables and payables existing at the end of quarter. Average exposure has been computed on an end-of-quarter basis. The other transactions underlying the derivative financial instruments are not included in the following value-at-risk presentation, since they comprise forecast cash flows. See also table Nominal amounts of derivative financial instruments used in hedge accounting in Note 32.

Hedge accounting

When designating derivative financial instruments, a hedge ratio of 1 is applied. In addition, the respective volume and currency of the hedge and the underlying transaction as well as maturity dates are matched. The Group ensures an economic relationship between the underlying transaction and the hedging instrument by ensuring consistency of currency, volume and maturity. Option premiums and also forward components are not designated into the hedging relationship, but the hedging costs are deferred in other comprehensive income and recognized in profit or loss at the due date of the underlying transaction or recognized as adjustment of acquisition cost of non-financial assets. The effectiveness of the hedge is assessed at the start of and during the hedging relationship. Possible sources of ineffectiveness of the hedging relationship are:

– Changes in the credit risk on the measurement of the used hedging instrument which are not reflected in the change of the hedged currency risk.

– Changes in the timing of the hedged transactions. Please refer to table Cash Flow Hedges and hedges of a net investment in foreign operations in note 32. There were no material effects on earnings in the years 2022 and 2023.

Please refer to table Cash Flow Hedges and hedges of a net investment in foreign operations in note 32. There were no material effects on earnings in the years 2022 and 2023.

The development of the value at risk from foreign currency hedging in 2023 was primarily shaped by a decrease in the volume of hedging transactions and volatilities.

The Group’s investments in liquid assets or refinancing activities are generally selected so that possible currency risks are minimized. Transaction risks arising from liquid assets or payables in foreign currencies that result from the Group’s investment or refinancing on money and capital markets are generally hedged against currency risks at the time of investing or refinancing in accordance with the Mercedes-Benz Group’s internal policies. The Group uses appropriate derivative financial instruments (e.g. cross-currency interest rate swaps) to hedge against currency risk.

Because currency risks from liquidity investments or liabilities in foreign currencies are generally fully offset due to the Group’s investment or refinancing and the derivative financial instruments used in this regard, these financial instruments were not included in the value-at-risk calculation presented.

Effects of currency (translation risk)

For purposes of Mercedes-Benz Group’s Consolidated Financial Statements, the income and expenses and the assets and liabilities of subsidiaries located outside the euro zone are converted into euros. Therefore, period-to-period changes in exchange-rates may cause translation effects that have a significant impact on, for example, revenue, segment profit/loss (EBIT) and assets and liabilities of the Group. Unlike exchange-rate transaction risk, currency translation risk does not necessarily affect future cash flows. The Group’s equity position reflects changes in carrying amounts caused by exchange-rates. In general, the Mercedes-Benz Group does not hedge against currency translation risk.

Interest rate risk

The Mercedes-Benz Group uses a variety of interest rate sensitive financial instruments to manage the liquidity needs of the Group. However, the majority of interest rate sensitive assets and liabilities results from the financial services business operated by Mercedes-Benz Mobility. The Mercedes-Benz Mobility companies enter into transactions with customers that primarily result in fixed-rate receivables. The Mercedes-Benz Group’s general policy is to match the refinancing of interest-bearing assets in terms of maturities and interest rates wherever economically feasible. However, for a narrowly limited portion of the receivables portfolio in selected and developed markets, Mercedes-Benz Mobility does not match refinancing in terms of maturities in order to take advantage of market opportunities. This results in the Mercedes-Benz Group being exposed to interest rate risks.

A committee consisting of representatives of the relevant segments and the corporate functions manages the interest rate risk by setting targets for the interest rate risk position. The Corporate Treasury department and the local Mercedes-Benz Group companies are jointly responsible for achieving these targets. As separate functions, the Treasury Controlling and the Mercedes-Benz Mobility Controlling & Reporting department monitor target achievement on a monthly basis.

In order to achieve the targeted interest rate risk positions in terms of maturities and interest rate fixing periods, the Mercedes-Benz Group also uses derivative financial instruments such as interest rate swaps. The interest rate risk position is assessed by comparing assets and liabilities for corresponding maturities, including the impact of the relevant derivative financial instruments.

Derivative financial instruments are also used in conjunction with the refinancing related to the automotive segments and liquidity management. The Mercedes-Benz Group steers the funding activities of the automotive segments and the financial services business at Group level.

The table Value at risk for exchange risk, interest rate risk and commodity price risk shows the period-end, high, low and average value-at-risk figures of the interest rate risk for the 2023 and 2022 portfolios of interest rate sensitive primary financial instruments and derivative financial instruments of the Group, including the financial instruments of the financial services business. Liabilities from leasing contracts for which the Mercedes-Benz Group acts as a lessee are not included in the value-at-risk of the interest rate risk. Average exposure has been computed on an end-of-quarter basis.

In the course of 2023, changes in the value at risk of interest rate sensitive financial instruments were primarily determined by the development of interest rate volatilities.

Hedge accounting

When designating derivative hedging instruments, the Mercedes-Benz Group generally applies a hedge ratio of 1. The respective volumes, interest curves, currencies and maturity dates of the underlying transaction and the hedging instrument are generally matched. In the case of combined derivative financial instruments for interest currency hedges, the cross-currency basis spread is not designated into the hedge relationship, but deferred as a hedging cost in other comprehensive income and recognized in profit or loss over the hedge term. The Group ensures an economic relationship between the underlying transaction and the hedging instrument by ensuring consistency of interest rates, maturity terms and nominal amounts. In the case of hedging for ABS transactions of private placements, the risk of the market interest rate component is partly protected, which historically covers on average more than 70% of the change in value of the total interest rate. The effectiveness of the hedge is assessed at the beginning and during the hedging relationship using the hypothetical derivative method. Possible sources of ineffectiveness of the hedging relationship are:

– Effects of the credit risk on the fair value of the hedging instruments in use which are not reflected in the change in the hedged interest rate risk.

– No perfect match for individual parameters of the underlying hedged transactions and the hedging instruments used.

– Premiums on hedging instruments for hedging ABS transactions.

There were no material effects on earnings in the years 2022 and 2023.

Commodity-price risk

The Mercedes-Benz Group is exposed to the risk of changes in market prices (e.g. for raw materials and energy) in connection with procuring manufacturing supplies used in production. The Mercedes-Benz Group usually counteracts the risk of short-term fluctuations in market prices by means of short and medium-term price escalation clauses or fixing of purchase prices in the supply contracts. The Mercedes-Benz Group concludes e.g. power purchase agreements for wind and solar energy in order to protect itself from fluctuations in energy prices and ensure long-term, sustainable procurement of electricity.

A small portion of the raw-material price risk relating to the forecast procurement of precious metals was hedged with the use of derivative financial instruments. The Mercedes-Benz Group has decided to suspend these hedging strategies for precious metals until further notice. The previously existing hedges expired in 2023.

The table Value at risk for exchange-rate risk, interest rate risk and commodity price risk shows the period-end, high, low and average value-at-risk figures for the 2022 portfolio of derivative financial instruments used to hedge commodity price risk. Average exposure has been computed on an end-of-quarter basis. The transactions underlying the derivative financial instruments are not included in the value-at-risk presentation.

Derivative financial instruments without hedge accounting

In 2023, the nominal volumes of hedging instruments not designated in a hedging relationship, amounted to €9 billion (2022: €12 billion) for derivatives used to hedge interest rate risks and €13 billion (2022: €15 billion) for derivatives used to hedge exchange-rate risks, as well as €644 million (2022: €644 million) for derivatives used to hedge commodity price risks (energy and raw materials).

Equity-price risk

The Mercedes-Benz Group predominantly holds investments in shares of companies which are classified as long-term investments, some of which are accounted for in the Consolidated Financial Statements using the equity method, such as the share in Daimler Truck Holding AG and BBAC. These investments are not included in a market risk assessment by the Group.