British American Tobacco p.l.c. – Annual report – 31 December 2025

Industry: tobacco

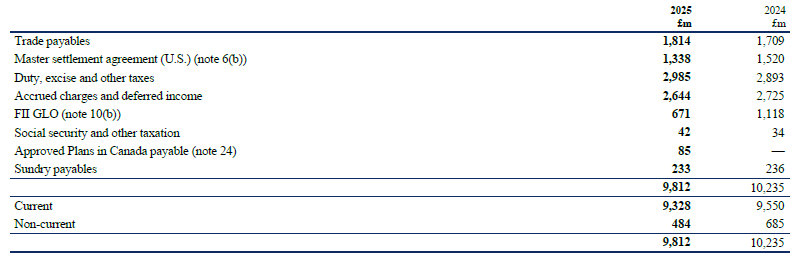

25 Trade and other payables

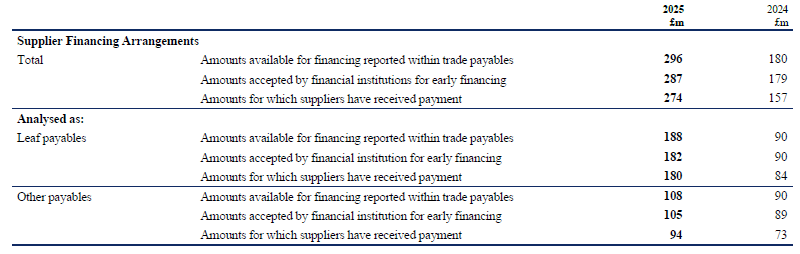

Supplier Financing Arrangements

The Group has certain supplier financing arrangements or ‘reverse factoring’ arrangements in place. The principal purpose of these arrangements is to provide the supplier with the option to access liquidity earlier through the sale of its receivables due from the Group to a bank or other financial institution prior to their due date. Management has determined that the Group’s payables to these suppliers have neither been extinguished nor have the liabilities been significantly modified by these arrangements. The value of amounts payable, invoice due dates and other terms and conditions applicable, from the Group’s perspective, remain unaltered, with only the ultimate payee being changed. Non-cash movements were immaterial. The cash outflows in respect of these arrangements have been recognised within operating cash flows.

Notes:

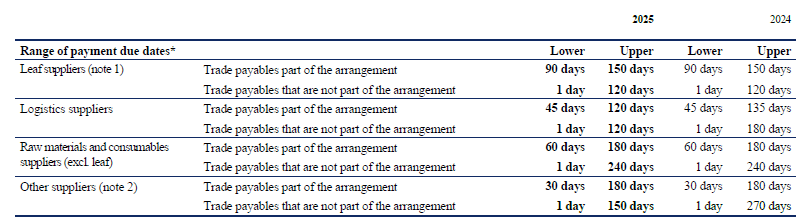

* Suppliers are subject to various payment due dates depending on the jurisdiction and standard practices. The Group’s payment terms commence from the invoice date. However, for certain categories of external suppliers, payment terms begin from the date a valid invoice is received.

1. Leaf suppliers are subject to various payment due dates depending on the jurisdiction and standard practices. In certain countries, the leaf suppliers who are not part of supplier financing arrangements are paid in advance or on the next working day.

2. The decrease in the upper limit for trade payables that are not part of the supplier financing arrangement (other suppliers) was due to a change in IT service provider.

Accrued charges and deferred income

Accrued charges and deferred income include £21 million of deferred income (2024: £20 million) relating to certain customer deposits in advance of shipments and £25 million (2024: £29 million) in respect of interest payable mainly related to tax matters.

26 Financial instruments and risk management (extract)

Liquidity risk (extract)

As part of its working capital management, in certain countries, the Group has entered into factoring arrangements and supply chain financing arrangements. These are explained in further detail in note 17 and note 25.