InterContinental Hotels Group PLC – Annual report – 31 December 2019

Industry: leisure

Significant accounting policies (extract)

Revenue recognition

Revenue is recognised at an amount that reflects the consideration to which the Group expects to be entitled in exchange for transferring goods or services to a customer.

Fee business revenue

Under franchise agreements, the Group’s performance obligation is to provide a licence to use IHG’s trademarks and other intellectual property. Franchise royalty fees are typically charged as a percentage of hotel gross rooms revenues and are treated as variable consideration, recognised as the underlying hotel revenues occur.

Under management agreements, the Group’s performance obligation is to provide hotel management services and a licence to use IHG’s trademarks and other intellectual property. Base and incentive management fees are typically charged. Base management fees are typically a percentage of total hotel revenues and incentive management fees are generally based on the hotel’s profitability or cash flows. Both are treated as variable consideration. Like franchise fees, base management fees are recognised as the underlying hotel revenues occur. Incentive management fees are recognised over time when it is considered highly probable that the related performance criteria will be met, provided there is no expectation of a subsequent reversal of the revenue.

Application and re-licensing fees are not considered to be distinct from the franchise performance obligation and are recognised over the life of the related contract.

Franchise and management agreements also contain a promise to provide technology support and network services to hotels. A monthly technology fee, based on either gross rooms revenues or the number of rooms in the hotel, is charged and recognised over time as these services are delivered. Technology fee income is included in Central revenue.

IHG’s global insurance programme provides coverage to managed hotels for risks such as US workers’ compensation, employee and general liability. Premiums are payable by the hotels to the third-party insurance provider. As some of the risk is reinsured by the Group’s captive insurance company (‘the Captive’), SCH Insurance Company, premiums paid from the third-party insurance provider to the Captive are recognised as revenue as premiums are earned.

Contract assets

Amounts paid to hotel owners to secure management and franchise agreements (‘key money’) are treated as consideration payable to a customer. A contract asset is recorded which is recognised as a deduction to revenue over the initial term of the contract. Where loans are provided to an owner the difference, if any, between the face and market value of the loan is capitalised as a contract asset.

Performance guarantees

In limited cases, the Group may provide performance guarantees to third-party hotel owners to secure management agreements. The expected value of payments under performance guarantees reduces the overall transaction price and is treated as a reduction to revenue over the life of the contract.

Revenue from owned, leased and managed lease hotels

At its owned, leased and managed lease hotels, the Group’s performance obligation is to provide accommodation and other goods and services to guests. Revenue includes rooms revenue and food and beverage sales, which is recognised when the rooms are occupied and food and beverages are sold.

Cost reimbursements

In a managed property, the Group acts as employer of the general manager and other employees at the hotel and is entitled to reimbursement of these costs. The performance obligation is satisfied over time as the employees perform their duties, consistent with when reimbursement is received. Reimbursements for these services are shown as revenue with an equal matching employee cost, with no profit impact. Certain other costs relating to both managed and franchised hotels are also contractually reimbursable to IHG and, where IHG is deemed to be acting as principal in the provision of the related services, the revenue and cost are shown on a gross basis.

System Fund revenues

The Group operates a System Fund (the Fund) to collect and administer cash assessments from hotel owners for the specific purpose of use in marketing, the Guest Reservation System and hotel loyalty programme. The Fund also receives proceeds from the sale of loyalty points under third-party co-branding arrangements. The Fund is not managed to generate a profit or loss for IHG over the longer term, but is managed for the benefit of the IHG System with the objective of driving revenues for the hotels in the System.

Under both franchise and management agreements, the Group is required to provide marketing and reservations services, as well as other centrally managed programmes. These services are provided by the Fund and are funded by assessment fees. Costs are incurred and allocated to the Fund in accordance with the principles agreed with the IHG Owners Association. The Group acts as principal in the provision of the services as the related expenses primarily comprise payroll and marketing expenses under contracts entered into by the Group. The assessment fees from hotel owners are generally levied as a percentage of hotel revenues and are recognised as those hotel revenues occur.

Certain travel agency commission revenues within the Fund are recognised on a net basis, where it has been determined that IHG is acting as agent.

In respect of the loyalty programme (IHG Rewards Club), the related performance obligation is to arrange for the provision of future benefits to members on consumption of previously earned reward points. Members have a choice of benefits: reward nights at an IHG hotel or other goods or services provided by third parties. Under its franchise and management agreements, IHG receives assessment fees based on total qualifying hotel revenue from IHG Rewards Club members’ hotel stays.

The Group’s performance obligation is not satisfied in full until the member has consumed the points at a participating hotel or selected a reward from a third party. Accordingly, loyalty assessments are deferred in an amount that reflects the stand-alone selling price of the future benefit to the member. Revenue is impacted by a ‘breakage’ estimate of the number of points that will never be consumed. On an annual basis, the Group engages an external actuary who uses statistical formulae to assist in formulating this estimate, which is adjusted to reflect actual experience up to the reporting date.

As materially all of the points will be either consumed at IHG managed or franchised hotels owned by third parties, or exchanged for awards provided by third parties, IHG is deemed to be acting as agent on consumption and therefore recognises the related revenue net of the cost of reimbursing the hotel or third party that is providing the benefit.

Performance obligations under the Group’s co-branding arrangements comprise:

• arranging for the provision of future benefits to members who have earned points or free night certificates;

• marketing services; and

• providing the co-brand partner with the right to access the loyalty programme.

Fees from these agreements comprise fixed amounts normally payable at the beginning of the contract, and variable amounts paid on a monthly basis. Variable amounts are typically based on the number of points and free night certificates issued to members and the marketing services performed by the Group. Total fees are allocated to the performance obligations based on their estimated stand-alone selling prices. Revenue allocated to marketing and licensing obligations is recognised on a monthly basis as the obligation is satisfied. Revenue relating to points and free night certificates is recognised when the member has consumed the points or certificates at a participating hotel or has selected a reward from a third party, net of the cost of reimbursing the hotel or third party that is providing the benefit.

Judgement is required in estimating the stand-alone selling prices which are based upon generally accepted valuation methodologies regarding the value of the licence provided, and the number of points and certificates expected to be issued. However, the value of revenue recognised and the deferred revenue balance at the end of the year is not materially sensitive to changes in these assumptions.

Contract costs

Certain costs incurred to secure management and franchise agreements, typically developer commissions, are capitalised and amortised over the initial term of the related contract. These costs are presented as ‘Contract costs’ in the Group statement of financial position.

Contract assets and contract costs are reviewed for impairment when events or changes in circumstances indicate that the carrying value may not be recoverable.

Critical accounting policies and the use of judgements, estimates and assumptions (extract)

In determining and applying the Group’s accounting policies, management are required to make judgements, estimates and assumptions. An accounting policy is considered to be critical if its selection or application could materially affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the Consolidated Financial Statements, and the reported amounts of revenues and expenses during the reporting period.

Judgements

System Fund

The Group operates a System Fund (the Fund) to collect and administer cash assessments from hotel owners for the specific purpose of use in marketing, the Guest Reservation System and hotel loyalty programme. Assessments are generally levied as a percentage of hotel revenues.

The Fund is not managed to generate a profit or loss for IHG over the longer term, but is managed for the benefit of the IHG System with the objective of driving revenues for the hotels in the System. In relation to marketing and reservation services, the Group’s performance obligation under IFRS 15 ‘Revenue from Contracts with Customers’ is determined to be the continuous performance of the services rather than the spending of the assessments received. Accordingly, assessment fees are recognised as hotel revenues occur, Fund expenses are charged to the Group income statement as incurred and no constructive obligation is deemed to exist under IAS 37 ‘Provisions, Contingent Liabilities and Contingent Assets’. Accordingly, no liability is recognised relating to the balance of unspent funds.

No other critical judgements have been made in applying the Group’s accounting policies.

Estimates (extract)

Management consider that critical estimates and assumptions are used for measuring the deferred revenue relating to the loyalty programme and in impairment testing, as discussed in further detail below. Estimates and assumptions are evaluated by management using historical experience and other factors believed to be reasonable based on current circumstances, however actual results could differ.

Loyalty programme

The hotel loyalty programme, IHG Rewards Club, enables members to earn points, funded through hotel assessments, during each qualifying stay at an IHG branded hotel and consume points at a later date for free accommodation or other benefits. The Group recognises deferred revenue in an amount that reflects IHG’s unsatisfied performance obligations, valued at the stand-alone selling price of the future benefit to the member. The amount of revenue recognised and deferred is impacted by ‘breakage’. On an annual basis the Group engages an external actuary who uses statistical formulae to assist in the estimate of the number of points that will never be consumed (‘breakage’). Significant estimation uncertainty exists in projecting members’ future consumption activity.

Actuarial gains and losses would correspondingly adjust the amount of System Fund revenues recognised and deferred revenue in the Group statement of financial position.

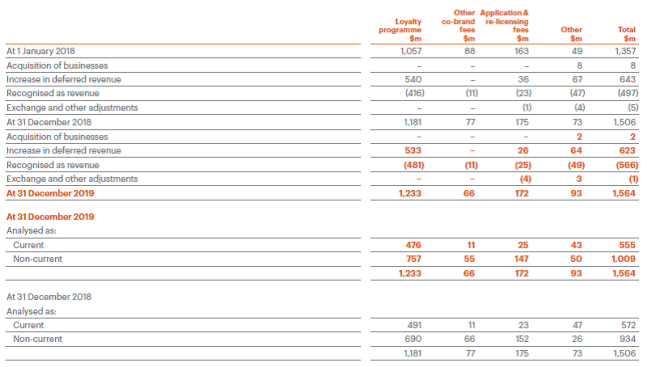

At 31 December 2019, deferred revenue relating to the loyalty programme was $1,233m (2018: $1,181m). Based on the conditions existing at the balance sheet date, a one percentage point decrease in the breakage estimate relating to outstanding points would increase this liability by approximately $16m.

3. Revenue

Disaggregation of revenue

The following table presents Group revenue disaggregated by type of revenue stream and by reportable segment:

Contract balances

A trade receivable is recorded when the Group has issued an invoice and has an unconditional right to receive payment. In respect of franchise fees, base and incentive management fees, Central revenue and revenues from owned, leased and managed lease hotels, the invoice is typically issued as the related performance obligations are satisfied, as described on page 144.

Contract assets (including performance guarantees)

Contract assets are recorded in respect of key money payments; the difference, if any, between the face and market value of loans made to owners; and the value of payments under performance guarantees.

At 31 December 2019, the amount of performance guarantees included within trade and other payables was $2m (2018: $3m) and the maximum payout remaining under such guarantees was $85m (2018: $42m).

Deferred revenue

Deferred revenue is recognised when payment is received before the related performance obligation is satisfied. The main categories of deferred revenue relate to the Loyalty programme, co-branding agreements, and franchise application and re-licensing fees.

The table on the previous page does not include amounts which were received and recognised as revenue in the same year. Amounts recognised as revenue were included in deferred revenue at the beginning of the year.

Loyalty programme revenues, shown gross in the table on the previous page, are presented net of the corresponding redemption cost in the Group income statement.

Other deferred revenue includes guest deposits received by owned, leased and managed lease hotels.

Transaction price allocated to remaining performance obligations

The Group has applied the practical expedient in IFRS 15 not to disclose the aggregate amount of the transaction price allocated to the performance obligations that are unsatisfied or partially unsatisfied as at the end of the reporting period for all amounts where the Group has a right to consideration in an amount that corresponds directly with the value to the customer of the Group’s performance completed to date (including franchise and management fees).

Amounts received and not yet recognised related to performance obligations that were unsatisfied at 31 December 2019 are as follows:

Contract costs

Movements in contract costs, typically developer commissions, are as follows:

33. System Fund

System Fund revenues comprise:

a Loyalty programme revenue is shown net of the cost of point redemptions.

System Fund expenses include: